Archive

HSBC protest tomorrow at noon with Alternative Banking (#OWS)

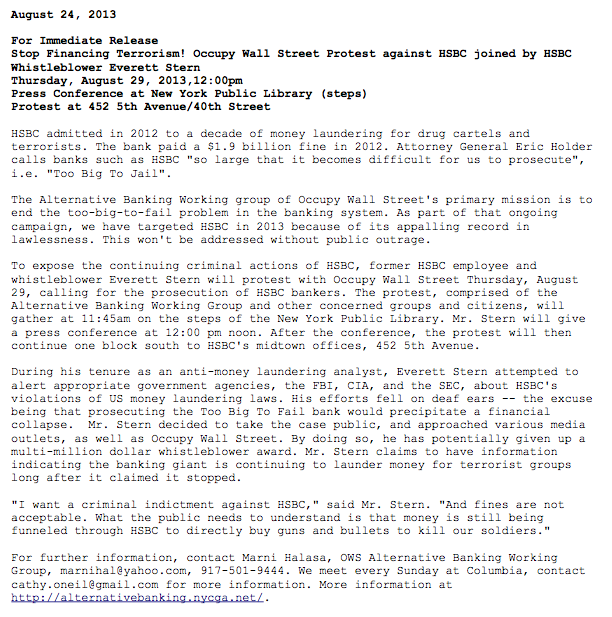

I’m helping organize a protest against HSBC with my Alternative Banking group. We’re going to be joined by Everett Stern, an HSBC whistleblower. You can learn more about that guy by reading Matt Taibbi’s Rolling Stones article on him.

Here’s the press release, I hope I see you there!

Occupy Finance, the book: announcement and fundraising (#OWS)

Members of the Alt Banking Occupy group have been hard at work recently writing a book which we call Occupy Finance. Our blog for the book is here. It’s a work in progress but we’re planning to give away 1,000 copies of the book on September 17th, the 2nd anniversary of the Occupation of Zuccotti Park.

We’re modeling it after another book which was put out last year by Strike Debt called the Debt Resistor’s Operations Manual, which I blogged about here when it came out.

Crappy Kickstarter

I want to tell you more about our book, which we’re writing by committee, but I did want to mention that in order to get the first 1,000 copies printed by September 17th, we’ll need altogether $2,500, and so far we’ve collected $2,150 from the various contributors, editors, and their friends. So we need to collect $350 at this point. If we get more then we’ll print more.

If you’d like to help us towards the last $350, we’d appreciate it – and I’ll even send you a copy of the book afterwards. But please don’t send anything you don’t want to give away, I can’t promise you some kind of formal proof of your contribution for tax purposes. This is Occupy after all, we suck at money. Consider this a crappy version of Kickstarter.

Anyway if you want to help out, send me a personal email to arrange it: cathy.oneil at gmail. I’ll basically just tell you to send me a personal check, since I’m the one fronting the money.

Audience and Mission

The mission of the book, like the mission of the Alt Banking group, is to explain the financial system and its dysfunction in plain English and to offer suggestions for how to think about it and what we can do to improve it.

The audience for this book is the 99% who are Occupy-friendly or at least Occupy-inquisitive. Specifically, we want people who know there’s something wrong, but don’t have the background to articulate what it is, to have a reference to help them define their issues. We want to give them ammunition at the water cooler.

What’s in the book?

After a stirring introduction, the book is divided into three basic parts: The Real Life Impact of Financialization, How We Got Here, and Things to do. I’ve got links below.

Keep in mind things are still in flux and will be changed, sometimes radically, before the final printing. In particular we’re actually using DropBox for most of our edits so the links below aren’t final versions (but will be eventually). Even so, the content below will give you a good idea of what we have in mind, and if you have comments or suggestions, please do tell us, thanks!

Our table of contents is as follows, and the available chapters have associated links:

Introduction: Fighting Our Way Out of the Financial Maze

The Real Life Impact of Financialization

- Heads They Win, Tails We Lose: Real Life Impact of Financialization on the 99%

- The bailout: it didn’t work, it’s still going on, and it’s making things worse

How We Got Here

- What Banks Do

- Impact of Deregulation

- The top ten financial outrages

- The muni bond industry and the 99%

Things to Do

Update: I’ve got $225 $301 pledged so far! You people rock!!

Larry Summers and the Lending Club

So here’s something potential Fed Chair Larry Summers is involved with, a company called Lending Club, which creates a money lending system that cuts out the middle man banks.

Specifically, people looking for money come to the site and tell their stories, and try to get loans. The investors invest in whichever loans look good to them, for however much money they want. For a perspective on the risks and rewards of this kind of peer-to-peer lending operation, look at this Wall Street Journal article which explains things strictly from the investor’s point of view.

A few red flags go up for me as I learn more about Lending Club.

First, from this NYTimes article, “The company [Lending Club] itself is not regulated as a bank. But it has teamed up with a bank in Utah, one of the states that allows banks to charge high interest rates, and that bank is overseen by state regulators and the Federal Deposit Insurance Corporation.”

I’m not sure how the FDIC is involved exactly, but the Utah connection is good for something, namely allowing high interest rates. According to the same article, 37% of loans are for APR’s of between 19% and 29%.

Next, Summers is referred to in that article as being super concerned about the ability for the consumers to pay back the loans. But I wonder how someone is supposed to be both desperate enough to go for a 25% APR loan and also able to pay back the money. This sounds like loan sharking to me.

Probably what bothers me most though is that Lending Club, in addition to offering credit scores and income when they have that information, also scores people asking for loans with a proprietary model which is, as you guessed it, unregulated. Specifically, if it’s anything like ZestFinance, could use signals more correlated to being uneducated and/or poor than to the willingness or ability to pay back loans.

By the way, I’m not saying this concept is bad for everyone- there are probably winners on the side of the loanees, and it might be possible that they get a loan they otherwise couldn’t get or they get better terms than otherwise or a more bespoke contract than otherwise. I’m more worried about the idea of this becoming the new normal of how money changes hands and how that would affect people already squeezed out of the system.

I’d love your thoughts.

Finance and open source

I want to bring up two quick topics this morning I’ve been mulling over lately which are both related to this recent post by Economist Rajiv Sethi from Barnard (h/t Suresh Naidu), who happened to be my assigned faculty mentor when I was an assistant prof there. I have mostly questions and few answers right now.

In his post, Sethi talks about former computer nerd for Goldman Sachs Sergey Aleynikov and his trial, which was chronicled by Michael Lewis recently. See also this related interview with Lewis, h/t Chris Wiggins.

I haven’t read Lewis’s piece yet, only his interview and Sethi’s reaction. But I can tell it’ll be juicy and fun, as Lewis usually is. He’s got a way with words and he’s bloodthirsty, always an entertaining combination.

So, the two topics.

First off, let’s talk a bit about high frequency trading, or HFT. My first two questions are, who does HFT benefit and what does HFT cost? For both of these, there’s the easy answer and then there’s the hard answer.

Easy answer for HFT benefitting someone: primarily the people who make loads of money off of it, including the hardware industry and the people who get paid to drill through mountains with cables to make connections between Chicago and New York faster.

Secondarily, market participants whose fees have been lowered because of the tight market-making brought about by HFT, although that savings may be partially undone by the way HFT’ers operate to pick off “dumb money” participants. After all, you say market making, I say arbing. Sorting out the winners, especially when you consider times of “extreme market conditions”, is where it gets hard.

Easy answer for the costs of HFT is for the companies that invest in IT and infrastructure and people to do the work, although to be sure they wouldn’t be willing to make that investment if they didn’t expect it to pay off.

A harder and more complete answer would involve how much risk we take on as a society when we build black boxes that we don’t understand and let them collide with each other with our money, as well as possibly a guess at what those people and resources now doing HFT might be doing otherwise.

And that brings me to my second topic, namely the interaction between the open source community and the finance community, but mostly the HFTers.

Sethi said it well (Cathy: see bottom of this for an update) this way in his post:

Aleynikov relied routinely on open-source code, which he modified and improved to meet the needs of the company. It is customary, if

not mandatory(Cathy: see bottom of this for an update) for these improvements to be released back into the public domain for use by others. But his attempts to do so were blocked:

Serge quickly discovered, to his surprise, that Goldman had a one-way relationship with open source. They took huge amounts of free software off the Web, but they did not return it after he had modified it, even when his modifications were very slight and of general rather than financial use. “Once I took some open-source components, repackaged them to come up with a component that was not even used at Goldman Sachs,” he says. “It was basically a way to make two computers look like one, so if one went down the other could jump in and perform the task.” He described the pleasure of his innovation this way: “It created something out of chaos. When you create something out of chaos, essentially, you reduce the entropy in the world.” He went to his boss, a fellow named Adam Schlesinger, and asked if he could release it back into open source, as was his inclination. “He said it was now Goldman’s property,” recalls Serge. “He was quite tense. When I mentioned it, it was very close to bonus time. And he didn’t want any disturbances.”

This resonates with my experience at D.E. Shaw. We used lots of python stuff, and as a community were working at the edges of its capabilities (not me, I didn’t do fancy HFT stuff, my models worked at a much longer time frame of at least a few hours between trades).

The urge to give back to the OS community was largely thwarted, when it came up at all, because there was a fear, or at least an argument, that somehow our competition would use it against us, to eliminate our edge, even if it was an invention or tool completely sanitized from the actual financial algorithm at hand.

A few caveats: First, I do think that stuff, i.e. python technology and the like eventually gets out to the open source domain even if people are consistently thwarting it. But it’s incredibly slow compared to what you might expect.

Second, It might be the case that python developers working outside of finance are actually much better at developing good tools for python, especially if they have some interaction with finance but don’t work inside. I’m guessing this because, as a modeler, you have a very selfish outlook and only want to develop tools for your particular situation. In other words, you might have some really weird looking tools if you did see a bunch coming from finance.

Finally, I think I should mention that quite a few people I knew at D.E. Shaw have now left and are actively contributing to the open source community now. So it’s a lagged contribution but a contribution nonetheless, which is nice to see.

Update: from my Facebook page, a discussion of the “mandatoriness” of giving back to the OS community from my brother Eugene O’Neil, super nerd, and friend William Stein, other super nerd:

Eugene O’Neil: the GPL says that if you give someone a binary executable compiled with GPL source code, you also have to provide them free access to all the source code used to generate that binary, under the terms of the GPL. This makes the commercial sale of GPL binaries without source code illegal. However, if you DON’T give anyone outside your organization a binary, you are not legally required to give them the modified source code for the binary you didn’t give them. That being said, any company policy that tries to explicitly PROHIBIT employees from redistributing modified GPL code is in a legal gray area: the loophole works best if you completely trust everyone who has the modified code to simply not want to distribute it.

William Stein: Eugene — You are absolutely right. The “mandatory” part of the quote: “It is customary, if not mandatory, for these improvements to be released back into the public domain for use by others.” from Cathy’s article is misleading. I frequently get asked about this sort of thing (because of people using Sage (http://sagemath.org) for web backends, trading, etc.). I’m not aware of any popular open source license that make it mandatory to give back changes if you use a project internally in an organization (let alone the GPL, which definitely doesn’t). The closest is AGPL, which involves external use for a website. Cathy — you might consider changing “Sethi said it well…”, since I think his quote is misleading at best. I’m personally aware of quite a few people that do use Sage right now who wouldn’t otherwise if Sethi’s statement were correct.

Should lawmakers use algorithms?

Here is an idea I’ve been hearing floating around the big data/ tech community: the idea of having algorithms embedded into law.

The argument for is pretty convincing on its face: Google has gotten its algorithms to work better and better over time by optimizing correctly and using tons of data. To some extent we can think of their business strategies and rules as a kind of “internal regulation”. So why don’t we take a page out of that book and improve our laws and specifically our regulations with constant feedback loops and big data?

No algos in law

There are some concerns I have right off the bat about this concept, putting aside the hugely self-serving dimension of it.

First of all, we would be adding opacity – of the mathematical modeling kind – to an already opaque system of law. It’s hard enough to read the legalese in a credit card contract without there also being a black box algorithm to make it impossible.

Second of all, whereas the incentives in Google are often aligned with the algorithm “working better”, whatever that means in any given case, the incentives of the people who write laws often aren’t.

So, for example, financial regulation is largely written by lobbyists. If you gave them a new tool, that of adding black box algorithms, then you could be sure they would use it to further obfuscate what is already a hopelessly complicated set of rules, and on top of it they’d be sure to measure the wrong thing and optimize to something random that would not interfere with their main goal of making big bets.

Right now lobbyists are used so heavily in part because they understand the complexity of their industries more than the lawmakers themselves. In other words, they actually add value in a certain way (besides in the monetary way). Adding black boxes would emphasize this asymmetric information problem, which is a terrible idea.

Third, I’m worried about the “black box” part of algorithms. There’s a strange assumption among modelers that you have to make algorithms secret or else people will game them. But as I’ve said before, if people can game your model, that just means your model sucks, and specifically that your proxies are not truly behavior-based.

So if it pertains to a law against shoplifting, say, you can’t have an embedded model which uses the proxy of “looking furtive and having bulges in your clothes.” You actually need to have proof that someone stole something.

If you think about that example for a moment, it’s absolutely not appropriate to use poor proxies in law, nor is it appropriate to have black boxes at all – we should all know what our laws are. This is true for regulation as well, since it’s after all still law which affects how people are expected to behave.

And by the way, what counts as a black box is to some extent in the eye of the beholder. It wouldn’t be enough to have the source code available, since that’s only accessible to a very small subset of the population.

Instead, anyone who is under the expectation of following a law should also be able to read and understand the law. That’s why the CFPB is trying to make credit card contracts be written in Plain English. Similarly, regulation law should be written in a way so that the employees of the regulator in question can understand it, and that means you shouldn’t have to have a Ph.D. in a quantitative field and know python.

Algos as tools

Here’s where algorithms may help, although it is still tricky: not in the law itself but in the implementation of the law. So it makes sense that the SEC has algorithms trying to catch insider trading – in fact it’s probably the only way for them to attempt to catch the bad guys. For that matter they should have many more algorithms to catch other kinds of bad guys, for example to catch people with suspicious accounting or consistently optimistic ratings.

In this case proxies are reasonable, but on the other hand it doesn’t translate into law but rather into a ranking of workflow for the people at the regulatory agency. In other words the SEC should use algorithms to decide which cases to pursue and on what timeframe.

Even so, there are plenty of reasons to worry. One could view the “Stop & Frisk” strategy in New York as following an algorithm as well, namely to stop young men in high-crime areas that have “furtive motions”. This algorithm happens to single out many innocent black and latino men.

Similarly, some of the highly touted New York City open data projects amount to figuring out that if you focus on looking for building code violations in high-crime areas, then you get a better hit rate. Again, the consequence of using the algorithm is that poor people are targeted at a higher rate for all sorts of crimes (key quote from the article: “causation is for other people”).

Think about this asymptotically: if you live in a nice neighborhood, the limited police force and inspection agencies never check you out since their algorithms have decided the probability of bad stuff happening is too low to bother. If, on the other hand, you are poor and live in a high-crime area, you get checked out daily by various inspectors, who bust you for whatever.

Said this way, it kind of makes sense that white kids smoke pot at the same rate as black kids but are almost never busted for it.

There are ways to partly combat this problem, as I’ve described before, by using randomization.

Conclusion

It seems to me that we can’t have algorithms directly embedded in laws, because of the highly opaque nature of them together with commonly misaligned incentives. They might be useful as tools for regulators, but the regulators who choose to use internal algorithms need to carefully check that their algorithms don’t have unreasonable and biased consequences, which is really hard.

Larry Summers being set up to fail?

I’m back from PyData, which was a lot of fun and filled with super nice nerdy people. My prezi slides are now available here.

I have time for one thought: a bunch of people have chatted me up recently with the theory that Larry Summers is being put in the running for the Fed Chair alongside Janet Yellen just so that, when Yellen gets the call, we can all breathe a sigh of relief it didn’t go to Summers.

In other words, it’s a wholly political ploy so the Obama can look like a hero for women everywhere when he chooses Yellen, and so that we can all conclude that at least Obama’s learned this one lesson with regards to dealing with the ongoing financial crisis: Summers isn’t the solution.

Depending on my mood I sometimes buy into this theory, but obviously I’m still worried.

Proprietary credit score model now embedded in law

I’ve blogged before about how I find it outrageous that the credit scoring models are proprietary, considering the impact they have on so many lives.

The argument given for keeping them secret is that otherwise people would game the models, but that really doesn’t make sense.

After all, the models that the big banks have to deal with through regulation aren’t secret, and they game those models all the time. It’s one of the main functions of the banks, in fact, to figure out how to game the models. So either we don’t mind gaming or we don’t hold up our banks to the same standards as our citizens.

Plus, let’s say the models were open and people started gaming the credit score models – what would that look like? A bunch of people paying their electricity bill on time?

Let’s face it: the real reason the models are secret is that the companies who set them up make more money that way, pretending to have some kind of secret sauce. What they really have, of course, is a pretty simple model and access to an amazing network of up-to-date personal financial data, as well as lots of clients.

Their fear is that, if their model gets out, anyone could start a credit scoring agency, but actually it wouldn’t be so easy – if I wanted to do it, I’d have to get all that personal data on everyone. In fact, if I could get all that personal data on everyone, including the historical data, I could easily build a credit scoring model.

So anyhoo, it’s all about money, that and the fact that we’re living under the assumption that it’s appropriate for credit scoring companies to wield all this power over people’s lives, including their love lives.

It’s like we have a secondary system of secret laws where we don’t actually get to see the rules, nor do we get to point out mistakes or reasonably refute them. And if you’re thinking “free credit report,” let’s be clear that that only tells you what data goes in to the model, it doesn’t tell you how it’s used.

As it turns out, though, it’s now more than like a secondary system of laws – it’s become embedded in our actual laws. Somehow the proprietary credit scoring company Equifax is now explicitly part of our healthcare laws. From this New York Times article (hat tip Matt Stoller):

Federal officials said they would rely on Equifax — a company widely used by mortgage lenders, social service agencies and others — to verify income and employment and could extend the initial 12-month contract, bringing its potential value to $329.4 million over five years.

Contract documents show that Equifax must provide income information “in real time,” usually within a second of receiving a query from the federal government. Equifax says much of its information comes from data that is provided by employers and updated each payroll period.

Under the contract, Equifax can use sources like credit card applications but must develop a plan to indicate the accuracy of data and to reduce the risk of fraud.

Thanks Equifax, I guess we’ll just trust you on all of this.

If we bailed out the banks, why not Detroit? (#OWS)

I wrote a post yesterday to discuss the fact that, as we’ve seen in Detroit and as we’ll soon see across the country, the math isn’t working out on pensions. One of my commenters responded, saying I was falling for a “very right wing attack on defined benefit pensions.”

I think it’s a mistake to think like that. If people on the left refuse to discuss reality, then who owns reality? And moreover, who will act and towards what end?

Here’s what I anticipate: just as “bankruptcy” in the realm of airlines has come to mean “a short period wherein we toss our promises to retired workers and then come back to life as a company”, I’m afraid that Detroit may signal the emergence of a new legal device for cities to do the same thing, especially the tossing out of promises to retired workers part. A kind of coordinated bankruptcy if you will.

It comes down to the following questions. For whom do laws work? Who can trust that, when they enter a legal obligation, it will be honored?

From Trayvon Martin to the people who have been illegally foreclosed on, we’ve seen the answer to that.

And then we might ask, for whom are laws written or exceptions made? And the answer to that might well be for banks, in times of crisis of their own doing, and so they can get their bonuses.

I’m not a huge fan of the original bailouts, because it ignored the social and legal contracts in the opposite way, that failures should fail and people who are criminals should go to jail. It didn’t seem fair then, and it still doesn’t now, as JP Morgan posts record $6.4 billion profits in the same quarter that it’s trying to settle a $500 million market manipulation charge.

It’s all very well to rest our arguments on the sanctity of the contract, but if you look around the edges you’ll see whose contracts get ripped up because of fraudulent accounting, and whose bonuses get bigger.

And it brings up the following question: if we bailed out the banks, why not the people of Detroit?

Math fraud in pensions

I wrote a post three months ago talking about how we don’t need better models but we need to stop lying with our models. My first example was municipal debt and how various towns and cities are in deep debt partly because their accounting for future pension obligations allows them to be overly optimistic about their investments and underfund their pension pots.

This has never been more true than it is right now, and as this New York Times Dealbook article explains, was a major factor in Detroit’s bankruptcy filing this past week. But don’t make any mistake: even in places where they don’t end up declaring bankruptcy, something is going to shake out because of these broken models, and it isn’t going to be extra money for retired civil servants.

It all comes down to wanting to avoid putting required money away and hiring quants (in this case actuaries) to make that seem like it’s mathematically acceptable. It’s a form of mathematical control fraud. From the article:

When a lender calculates the value of a mortgage, or a trader sets the price of a bond, each looks at the payments scheduled in the future and translates them into today’s dollars, using a commonplace calculation called discounting. By extension, it might seem that an actuary calculating a city’s pension obligations would look at the scheduled future payments to retirees and discount them to today’s dollars.

But that is not what happens. To calculate a city’s pension liabilities, an actuary instead projects all the contributions the city will probably have to make to the pension fund over time. Many assumptions go into this projection, including an assumption that returns on the investments made by the pension fund will cover most of the plan’s costs. The greater the average annual investment returns, the less the city will presumably have to contribute. Pension plan trustees set the rate of return, usually between 7 percent and 8 percent.

In addition, actuaries “smooth” the numbers, to keep big swings in the financial markets from making the pension contributions gyrate year to year. These methods, actuarial watchdogs say, build a strong bias into the numbers. Not only can they make unsustainable pension plans look fine, they say, but they distort the all-important instructions actuaries give their clients every year on how much money to set aside to pay all benefits in the future.

One caveat: if the pensions have actually been making between 7 percent and 8 percent on their investments every year then all is perhaps well. But considering that they typically invest in bonds, not stocks – which is a good thing – we’re likely seeing much smaller returns than that, which means their yearly contributions to the local pension plans are in dire straits.

What’s super interesting about this article is that it goes into the action on the ground inside the Actuary community, since their reputations are at stake in this battle:

A few years ago, with the debate still raging and cities staggering through the recession, one top professional body, the Society of Actuaries, gathered expert opinion and realized that public pension plans had come to pose the single largest reputational risk to the profession. A Public Plans Reputational Risk Task Force was convened. It held some meetings, but last year, the matter was shifted to a new body, something called the Blue Ribbon Panel, which was composed not of actuaries but public policy figures from a number of disciplines. Panelists include Richard Ravitch, a former lieutenant governor of New York; Bradley Belt, a former executive director of the Pension Benefit Guaranty Corporation; and Robert North, the actuary who shepherds New York City’s five big public pension plans.

I’m not sure what happened here, but it seems like a bunch of people in a profession, the actuaries, got worried that they were being used by politicians, and decided to investigate, but then that initiative got somehow replaced by a bunch of politicians. I’d love to talk to someone on the inside about this.

On being a data science skeptic: due out soon

A few months ago, at the end of January, I wrote a post about Bill Gates naive views on the objectivity of data. One of the commenters, “CitizensArrest,” asked me to take a look at a related essay written by Susan Webber entitled “Management’s Great Addiction: It’s time we recognized that we just can’t measure everything.”

Webber’s essay is really excellent, not to mention impressively prescient considering it was published in 2006, before the credit crisis. The format of the essay is simple: it brings up and explains various dangers in the context of measurement and modeling of business data, and calls for finding a space in business for skepticism. What an idea! Imagine if that had actually happened in finance when it should have back in 2006.

Please go read her essay, it’s short.

Recently, when O’Reilly asked me to write an essay, I thought back to this short piece and decided to use it as a template for explaining why I think there’s a just-as-desperate need for skepticism in 2013 here in the big data world as there was back then in finance.

Whereas most of Webber’s essay talks about people blindly accepting numbers as true, objective, precise, and important, and the related tragic consequences, I’ve added a small wrinkle to this discussion. Namely, I also devote concern over the people who underestimate the power of data.

Most of this disregard for unintended consequences is blithe and unintentional (and some of it isn’t), but even so it can be hugely damaging, especially to the individuals being modeled: think foreclosed homes due to crappy housing-related models in the past, and think creepy models and the death spiral of modeling for the present and future.

Anyhoo, I’m actively writing it now, and it’ll be coming out soon. Stay tuned!

You give me a capital requirement, I’ll give you a derivative to skirt it.

I’ve enjoyed reading Anat Admati and Martin Hellwig’s recent book, The Bankers’ New Clothes, which explains a ton of things extremely well, including:

- Differentiating between what’s “good for banks” (i.e. bankers) versus what’s good for the public, and how, through unnecessary complexity and shittons of lobbying money, the “good for bankers” case is made much more often and much more vehemently,

- that, when there’s a guaranteed backstop for a loan, the person taking out the loan has incentive to take on more risk, and

- that there are two different definitions of “big returns” depending on the context: one means big in absolute value (where -30% is bigger than -10%), the other mean big as in more positive (where -10% is bigger than -30%). Believe it or not, this ambiguity could be (at least metaphorically) taken as a cause of confusion when bankers talk to the public, in the following sense. Namely, when the expected return on an investment is, say, 3%, it makes sense for bankers to lever up their bets so they get “bigger returns” in the first sense, especially since there’s essentially no down side for them (a -30% return doesn’t affect them personally, a 30% return means a huge bonus). From the perspective of the public, they’d like to see the banks go for the “bigger return” in the second sense, so avoid the -30% scenario altogether, via restrained risk-taking.

Admati and Hellwig’s suggestion is to raise capital requirements to much higher levels than we currently have.

Here’s the thing though, and it’s really a question for you readers. How do derivatives show up on the balance sheet exactly, and what prevents me from building a derivative that avoids adding to my capital requirement but which adds risk to my portfolio?

I’ve been getting a lot of different information from people about whether this is possible, or will be possible once Basel III is implemented, but I haven’t reached anyone yet who is actually expert enough to make a definitive claim one way or the other.

It’s one thing if you’re talking about government interest rate swaps, but how do CDS’s, for example, get treated in terms of capital requirements? Is there an implicit probability of default used for accounting purposes? In that case, since such instruments are famously incredibly fat-tailed (i.e. the probability of default looks miniscule until it doesn’t), wouldn’t that encourage everyone to invest extremely heavily in instruments that don’t move their capital ratios much but take on outrageous risks? The devil’s in the detail here.

Payroll cards: “It costs too much to get my money” (#OWS)

If this article from yesterday’s New York Times doesn’t make you want to join Occupy, then nothing will.

It’s about how, if you work at a truly crappy job like Walmart or McDonalds, they’ll pay you with a pre-paid card that charges you for absolutely everything, including checking your balance or taking your money, and will even charge you for not using the card. Because we aren’t nickeling and diming these people enough.

The companies doing this stuff say they’re “making things convenient for the workers,” but of course they’re really paying off the employers, sometimes explicitly:

In the case of the New York City Housing Authority, it stands to receive a dollar for every employee it signs up to Citibank’s payroll cards, according to a contract reviewed by The New York Times.

Thanks for the convenience, payroll card banks!

One thing that makes me extra crazy about this article is how McDonalds uses its franchise system to keep its hands clean:

For Natalie Gunshannon, 27, another McDonald’s worker, the owners of the franchise that she worked for in Dallas, Pa., she says, refused to deposit her pay directly into her checking account at a local credit union, which lets its customers use its A.T.M.’s free. Instead, Ms. Gunshannon said, she was forced to use a payroll card issued by JPMorgan Chase. She has since quit her job at the drive-through window and is suing the franchise owners.

“I know I deserve to get fairly paid for my work,” she said.

The franchise owners, Albert and Carol Mueller, said in a statement that they comply with all employment, pay and work laws, and try to provide a positive experience for employees. McDonald’s itself, noting that it is not named in the suit, says it lets franchisees determine employment and pay policies.

I actually heard about this newish scheme against the poor when I attended the CFPB Town Hall more than a year ago and wrote about it here. Actually that’s where I heard people complain about Walmart doing this but also court-appointed child support as well.

Just to be clear, these fees are illegal in the context of credit cards, but financial regulation has not touched payroll cards yet. Yet another way that the poor are financialized, which is to say they’re physically and psychologically separated from their money. Get on this, CFPB!

Update: an excellent article about this issue was written by Sarah Jaffe a couple of weeks ago (hat tip Suresh Naidu). It ends with an awesome quote by Stephen Lerner: “No scam is too small or too big for the wizards of finance.”

How to understand the career trajectory of Larry Summers

I heard from a Wall Street Journal recently that Summers is on the short list for the Fed Chair. I’m wondering, how often and in how many ways does this guy need to fail before people stop thinking this guy is the silver bullet?

Then I remember this article which talks about a study that connects overconfidence with social status. From the article:

“Our studies found that overconfidence helped people attain social status. People who believed they were better than others, even when they weren’t, were given a higher place in the social ladder. And the motive to attain higher social status thus spurred overconfidence,” says Anderson, the Lorraine Tyson Mitchell Chair in Leadership and Communication II at the Haas School.

Social status is the respect, prominence, and influence individuals enjoy in the eyes of others. Within work groups, for example, higher status individuals tend to be more admired, listened to, and have more sway over the group’s discussions and decisions. These “alphas” of the group have more clout and prestige than other members. Anderson says these research findings are important because they help shed light on a longstanding puzzle: why overconfidence is so common, in spite of its risks. His findings suggest that falsely believing one is better than others has profound social benefits for the individual.

Of course, Larry Summers isn’t the only example of this I can think of, but he’s a pretty perfect one.

Technocrats and big data

Today I’m finally getting around to reporting on the congressional subcommittee I went to a few weeks ago on big data and analytics. Needless to say it wasn’t what I’d hoped.

My observations are somewhat disjointed, since there was no coherent discussion, so I guess I’ll just make a list:

- The Congressmen and women seem to know nothing more about the “Big Data Revolution” than what they’d read in the now-famous McKinsey report which talks about how we’ll need 180,000 data scientists in the next decade and how much money we’ll save and how competitive it will make our country.

- In other words, with one small exception I’ll discuss below, the Congresspeople were impressed, even awed, at the intelligence and power of the panelists. They were basically asking for advice on how to let big data happen on a bigger and better scale. Regulation never came up, it was all about, “how do we nurture this movement that is vital to our country’s health and future?”

- There were three useless panelists, all completely high on big data and making their money being like that. First there was a schmuck from the NSF who just said absolutely nothing, had been to a million panels before, and was simply angling to be invited to yet more.

- Next there was a guy who had started training data-ready graduates in some masters degree program. All he ever talked about is how programs like his should be funded, especially his, and how he was talking directly with employers in his area to figure out what to train his students to know.

- It was especially interesting to see how this second guy reacted when the single somewhat thoughtful and informed Congressman, whose name I didn’t catch because he came in and left quickly and his name tag was miniscule, asked him about whether or not he taught his students to be skeptical. The guy was like, I teach my students to be ready to deal with big data just like their employers want. The congressman was like, no that’s not what I asked, I asked whether they can be skeptical of perceived signals versus noise, whether they can avoid making huge costly mistakes with big data. The guy was like, I teach my students to deal with big data.

- Finally there was the head of IBM Research who kept coming up with juicy and misleading pro-data tidbits which made him sound like some kind of saint for doing his job. For example, he brought up the “premature infants are being saved” example I talked about in this post.

- The IBM guy was also the only person who ever mentioned privacy issues at all, and he summarized his, and presumably everyone else’s position on this subject, by saying “people are happy to give away their private information for the services they get in return.” Thanks, IBM guy!

- One more priceless moment was when one of the Congressmen asked the panel if industry has enough interaction with policy makers. The head of IBM Research said, “Why yes, we do!” Thanks, IBM guy!

I was reminded of this weird vibe and power dynamic, where an unchallenged mysterious power of big data rules over reason, when I read this New York Times column entitled Some Cracks in the Cult of Technocrats (hat tip Suresh Naidu). Here’s the leading paragraph:

We are living in the age of the technocrats. In business, Big Data, and the Big Brains who can parse it, rule. In government, the technocrats are on top, too. From Washington to Frankfurt to Rome, technocrats have stepped in where politicians feared to tread, rescuing economies, or at least propping them up, in the process.

The column was written by Chrystia Freeland and it discusses a recent paper entitled Economics versus Politics: Pitfalls of Policy Advice by Daron Acemoglu from M.I.T. and James Robinson from Harvard. A description of the paper from Freeland’s column:

Their critique is not the standard technocrat’s lament that wise policy is, alas, politically impossible to implement. Instead, their concern is that policy which is eminently sensible in theory can fail in practice because of its unintended political consequences.

In particular, they believe we need to be cautious about “good” economic policies that have the side effect of either reinforcing already dominant groups or weakening already frail ones.

“You should apply double caution when it comes to policies which will strengthen already powerful groups,” Dr. Acemoglu told me. “The central starting point is a certain suspicion of elites. You really cannot trust the elites when they are totally in charge of policy.”

Three examples they discuss in the paper: trade unions, financial deregulation in the U.S., privatization in Russia. Examples where something economists suggested would make the system better also acted to reinforce power of already powerful people.

If there’s one thing I might infer from my trip to Washington, it’s that the technocrats in charge nowadays, whose advice is being followed, may have subtly shifted away from deregulation economists and towards big data folks. Not that I’m holding my breath for Bob Rubin to be losing his grip any time soon.

Mr. Ratings Reformer Goes to Washington: Some Thoughts on Financial Industry Activism

This is a guest post by Marc Joffe, the principal consultant at Public Sector Credit Solutions, an organization that provides data and analysis related to sovereign and municipal securities. Previously, Joffe was a Senior Director at Moody’s Analytics for more than a decade.

Note to readers: for a bit of background on the SEC Credit Ratings Roundtable and the Franken Amendment see this recent mathbabe post.

I just returned from Washington after participating in the SEC’s Credit Ratings Roundtable. The experience was very educational, and I wanted to share what I’ve learned with readers interested in financial industry reform.

First and foremost, I learned that the Franken Amendment is dead. While I am not a proponent of this idea – under which the SEC would have set up a ratings agency assignment authority – I do welcome its intentions and mourn its passing. Thus, I want to take some time to explain why I think this idea is dead, and what financial reformers need to do differently if they want to see serious reforms enacted.

The Franken Amendment, as revised by the Dodd Frank conference committee, tasked the SEC with investigating the possibility of setting up a ratings assignment authority and then executing its decision. Within the SEC, the responsibility for Franken Amendment activities fell upon the Office of Credit Ratings (OCR), a relatively new creature of the 2006 Credit Rating Agency Reform Act.

OCR circulated a request for comments – posting the request on its web site and in the federal register – a typical SEC procedure. The majority of serious comments OCR received came from NRSROs and others with a vested interest in perpetuating the status quo or some close approximation thereof. Few comments came from proponents of the Franken Amendment, and some of those that did were inarticulate (e.g., a note from Joe Sixpack of Anywhere, USA saying that rating agencies are terrible and we just gotta do something about them).

OCR summarized the comments in its December 2012 study of the Franken Amendment. Progressives appear to have been shocked that OCR’s work product was not an originally-conceived comprehensive blueprint for a re-imagined credit rating business. Such an expectation is unreasonable. SEC regulators sit in Washington and New York; not Silicon Valley. There is little upside and plenty of political downside to taking major risks. Regulators are also heavily influenced by the folks they regulate, since these are the people they talk to on a day-to-day basis.

Political theorists Charles Lindblom and Aaron Wildavsky developed a theory that explains the SEC’s policymaking process quite well: it is called incrementalism. Rather than implement brand new ideas, policymakers prefer to make marginal changes by building upon and revising existing concepts.

While I can understand why Progressives think the SEC should “get off its ass” and really fix the financial industry, their critique is not based in the real world. The SEC is what it is. It will remain under budget pressure for the forseeable future because campaign donors want to restrict its activities. Staff will always be influenced by financial industry players, and out-of-the-box thinking will be limited by the prevailing incentives.

Proponents of the Franken Amendment and other Progressive reforms have to work within this system to get their reforms enacted. How? The answer is simple: when a request for comment arises they need to stuff the ballot box with varying and well informed letters supporting reform. The letters need to place proposed reforms within the context of the existing system, and respond to anticipated objections from status quo players. If 20 Progressive academics and Occupy-leaning financial industry veterans had submitted thoughtful, reality-based letters advocating the Franken Amendment, I believe the outcome would have been very different. (I should note that Occupy the SEC has produced a number of comment letters, but they did not comment on the Franken Amendment and I believe they generally send a single letter).

While the Franken Amendment may be dead, I am cautiously optimistic about the lifecycle of my own baby: open source credit rating models. I’ll start by explaining how I ended up on the panel and then conclude by discussing what I think my appearance achieved.

The concept of open source credit rating models is extremely obscure. I suspect that no more than a few hundred people worldwide understand this idea and less than a dozen have any serious investment in it. Your humble author and one person on his payroll, are probably the world’s only two people who actually dedicated more than 100 hours to this concept in 2012.

That said, I do want to acknowledge that the idea of open source credit rating models is not original to me – although I was not aware of other advocacy before I embraced it. Two Bay Area technologists started FreeRisk, a company devoted to open source risk models, in 2009. They folded the company without releasing a product and went on to more successful pursuits. FreeRisk left a “paper” trail for me to find including an article on the P2P Foundation’s wiki. FreeRisk’s founders also collaborated with Cate Long, a staunch advocate of financial markets transparency, to create riski.us – a financial regulation wiki.

In 2011, Cathy O’Neil (a.k.a. Mathbabe) an influential Progressive blogger who has a quantitative finance background ran a post about the idea of open source credit ratings, generating several positive comments. Cathy also runs the Alternative Banking group, an affiliate of Occupy Wall Street that attracts a number of financially literate activists.

I stumbled across Cathy’s blog while Googling “open source credit ratings”, sent her an email, had a positive phone conversation and got an invitation to address her group. Cathy then blogged about my open source credit rating work. This too was picked up on the P2P Foundation wiki, leading ultimately to a Skype call with the leader of the P2P Foundation, Michel Bauwens. Since then, Michel – a popularizer of progressive, collaborative concepts – has offered a number of suggestions about organizations to contact and made a number of introductions.

Most of my outreach attempts on behalf of this idea – either made directly or through an introduction – are ignored or greeted with terse rejections. I am not a proven thought leader, am not affiliated with a major research university and lack a resume that includes any position of high repute or authority. Consequently, I am only a half-step removed from the many “crackpots” that send around their unsolicited ideas to all and sundry.

Thus, it is surprising that I was given the chance to address the SEC Roundtable on May 14. The fact that I was able to get an invitation speaks well of the SEC’s process and is thus worth recounting. In October 2012, SEC Commissioner Dan Gallagher spoke at the Stanford Rock Center on Corporate Governance. He mentioned that the SEC was struggling with the task of implementing Dodd Frank Section 939A, which calls for the replacement of credit ratings in federal regulations, such as those that govern asset selection by money market funds.

After his talk, I pitched him the idea of open source credit ratings as an alternative creditworthiness standard that would satisfy the intentions of 939A. He suggested that I write to Tom Butler, head of the Office of Credit Ratings (OCR) and copy him. This led to a number of phone calls and ultimately a presentation to OCR staff in New York in January. Staff members that joined the meeting were engaged and asked good questions. I connected my proposal to an earlier SEC draft regulation which would have required structured finance issuers to publish cashflow waterall models in Python – a popular open source language.

I walked away from the meeting with the perception that, while they did not want to reinvent the industry, OCR staff were sincerely interested in new ideas that might create incremental improvements. That meeting led to my inclusion in the third panel of the Credit Ratings Roundtable.

For me, the panel discussion itself was mostly positive. Between the opening statement, questions and discussion, I probably had about 8 minutes to express my views. I put across all the points I hoped to make and even received a positive comment from one of the other panelists. On the downside, only one commissioner attended my panel – whereas all five had been present at the beginning of the day when Al Franken, Jules Kroll, Doug Peterson and other luminaries held the stage.

The roundtable generated less media attention than I expected, but I got an above average share of the limited coverage relative to the day’s other 25 panelists. The highlight was a mention in the Wall Street Journal in its pre-roundtable coverage.

Perhaps the fact that I addressed the SEC will make it easier for me to place op-eds and get speaking engagements to promote the open source ratings concept. Only time will tell. Ultimately, someone with a bigger reputation than mine will need to advocate this concept before it can progress to the next level.

Also, the idea is now part of the published record of SEC deliberations. The odds of it getting into a proposed regulation remain long in the near future, but these odds are much shorter than they were prior to the roundtable.

Political scientist John Kingdon coined the term “policy entrepreneurs” to describe people who look for and exploit opportunities to inject new ideas into the policy discussion. I like to think of myself as a policy entrepreneur, although I have a long way to go before I become a successful one. If you have read this far and also have strongly held beliefs about how the financial system should improve, I suggest you apply the concepts of incrementalism and policy entrepreneurship to your own activism.

Money, food, and the local

I take the Economist into the bath with me on the weekend when I have time. It’s relaxing for whatever reason, even when it’s describing horrible things or when I disagree with it. I appreciate the Economist for at least discussing many of the issues I care about.

Last night I came across this book review, about the book “Money: The Unauthorised Biography” written by Felix Martin. It tells the story of an ad hoc currency system in Ireland popping up during a financial crisis more than 40 years ago. The moral of that story is supposed to be something about how banking should operate, but I was struck by this line in the review:

It helped that a lot of Irish life is lived locally: builders, greengrocers, mechanics and barmen all turned out to be dab hands at personal credit profiling.

It occurs to me that “living locally” is exactly what most people, at least in New York, don’t do at all.

At this point I’ve lived in my neighborhood near Columbia University for 8 years, which is long enough to know Bob, the guy at the hardware store who sells me air conditioners and spatulas. If our currency system froze and we needed to use IOU notes, I’m pretty sure Bob and I would be good.

But, even though I shop at Morty’s (Morton Williams) regularly, the turnover there is high enough that I have never connected with anyone working there. I’m shit out of luck for food, in other words, in the case of a currency freeze.

Bear with me for one more minute. When I read articles like this one, which is called Pay People to Cook at Home – in which the author proposes a government program that will pay young parents to stay home and cook healthy food – it makes me think two things.

First, that people sometimes get confused between what could or should happen and what might actually happen, mostly because they don’t think about power and who has it and what their best interests are. I’m not holding my breath for this government program, in other words, even though I think there’s definitely a link between a hostile food environment and bad health among our nation’s youth.

Second, that in some sense we traditionally had pretty good solutions to child care and home cooking, namely we lived together with our families and not everyone had a job, so someone was usually on hand to cook and watch the kids. It’s a natural enough arrangement, which we’ve chucked in favor of a cosmopolitan existence.

And when I say “natural”, I don’t mean “appealing”: my mom has a full-time job as a CS professor in Boston and is not interested in staying home and cooking. Nor am I, for that matter.

In other words, we’ve traded away localness for something else, which I’m personally benefitting from, but there are other direct cultural effects which aren’t always so awesome. Our dependency on international banking and credit scores and having very little time to cook for our kids are a few examples.

Housing bubble or predictable consequence of income inequality?

It’s Sunday, which for me is a day of whimsical smoke-blowing. To mark the day, I think I’ll assume a position about something I know very little about, namely real estate. Feel free to educate me if I’m saying something inaccurate!

There has been a flurry of recent articles warning us that we might be entering a new housing bubble, for example this Bloomberg article. But if you look closely, the examples they describe seem cherry picked:

An open house for a five-bedroom brownstone in Brooklyn, New York, priced at $949,000 drew 300 visitors and brought in 50 offers. Three thousand miles away in Menlo Park, California, a one-story home listed for $2 million got six offers last month, including four from builders planning to tear it down to construct a bigger house. In south Florida, ground zero for the last building boom and bust, 3,300 new condominium units are under way, the most since 2007.

They mention later that Boston hasn’t risen so high as the others hot cities recently, but if you compare Boston to, say, Detroit on this useful Case-Schiller city graph, you’ll note that Boston never really went that far down in the first place.

When I read this kind of article, I can’t help but wonder how much of the signal they are seeing is explained by income inequality, combined with the increasing segregation of rich people in certain cities. New York City and Menlo Park are great examples of places where super rich people live, or want to live, and it’s well known that those buyers have totally recovered from the recession (see for example this article).

And it’s not even just American rich people investing in these cities. Judging from articles like this one in the New York Times, we’re now building luxury sky-scrapers just to attract rich Russians. The fatness of this real estate tail is extraordinary, and it makes me think that when we talk about real estate recoveries we should have different metrics than simply “average sell price”. We need to adjust our metrics to reflect the nature of the bifurcated market.

Now it’s also true that other cities, like Phoenix and Las Vegas are also gaining in the market. Many of the houses in these unsexier areas are being gobbled up by private equity firms investing in rental property. This is a huge part of the market right now in those places, and they buy whole swaths of houses at once. Note we’re not hearing about open houses with 300 buyers there.

Besides considering the scary consequences of a bunch of enormous profit-seeking management companies controlling our nation’s housing, and changing the terms of the rental agreements, I’ll just point out that these guys probably aren’t going to build too large a bubble, since their end-feeder is the renter, the average person who has a very limited income and ability to pay, unlike the Russians. On the other hand, they probably don’t know what they’re doing, so my error bars are large.

I’m not saying we don’t have a bubble, because I’d have to do a bunch of reckoning with actual numbers to understand stuff more. I’m just saying articles like the Bloomberg one don’t convince me of anything besides the fact that very rich people all want to live in the same place.

Dow at an all-time high, who cares?

The Dow is at an all-time high. Here’s the past 12 months:

Once upon a time it might have meant something good, in a kind of “rising tide lifts all boats” sort of way. Nowadays not so much.

Of course, if you have a 401K you’ll probably be a bit happier than you were 4 years ago. Or if you’re an investor with money in the game.

On the other hand, not many people have 401K plans, and not many who do don’t have a lot of money in them, partly because one in four people have needed to dip into their savings lately in spite of the huge fees they were slapped with for doing so. Go watch the recent Frontline episode about 401Ks to learn more about this scammy industry.

Let’s face it, the Dow is so high not because the economy is great, or even because it is projected to be great soon. It’s mostly inflated out of a combination of easy Fed money for banks, which translates to easy money for people who are already rich, and the fact that world-wide investors are afraid of Europe and are parking their money in the U.S. until the Euro problem gets solved.

In other words, that money is going to go away if people decide Europe looks stable, or if the Fed decides to raise interest rates. The latter might happen when the economy (or rather, if the economy) looks better, so putting that together we’re talking about a possible negative stock market response to a positive economic outlook.

The stock market has officially become decoupled from our nation’s future.

SEC Roundtable on credit rating agency models today

I’ve discussed the broken business model that is the credit rating agency system in this country on a few occasions. It directly contributed to the opacity and fraud in the MBS market and to the ensuing financial crisis, for example. And in this post and then this one, I suggest that someone should start an open source version of credit rating agencies. Here’s my explanation:

The system of credit ratings undermines the trust of even the most fervently pro-business entrepreneur out there. The models are knowingly games by both sides, and it’s clearly both corrupt and important. It’s also a bipartisan issue: Republicans and Democrats alike should want transparency when it comes to modeling downgrades- at the very least so they can argue against the results in a factual way. There’s no reason I can see why there shouldn’t be broad support for a rule to force the ratings agencies to make their models publicly available. In other words, this isn’t a political game that would score points for one side or the other.

Well, it wasn’t long before Marc Joffe, who had started an open source credit rating agency, contacted me and came to my Occupy group to explain his plan, which I blogged about here. That was almost a year ago.

Today the SEC is going to have something they’re calling a Credit Ratings Roundtable. This is in response to an amendment that Senator Al Franken put on Dodd-Frank which requires the SEC to examine the credit rating industry. From their webpage description of the event:

The roundtable will consist of three panels:

- The first panel will discuss the potential creation of a credit rating assignment system for asset-backed securities.

- The second panel will discuss the effectiveness of the SEC’s current system to encourage unsolicited ratings of asset-backed securities.

- The third panel will discuss other alternatives to the current issuer-pay business model in which the issuer selects and pays the firm it wants to provide credit ratings for its securities.

Marc is going to be one of something like 9 people in the third panel. He wrote this op-ed piece about his goal for the panel, a key excerpt being the following:

Section 939A of the Dodd-Frank Act requires regulatory agencies to replace references to NRSRO ratings in their regulations with alternative standards of credit-worthiness. I suggest that the output of a certified, open source credit model be included in regulations as a standard of credit-worthiness.

Just to be clear: the current problem is that not only is there wide-spread gaming, but there’s also a near monopoly by the “big three” credit rating agencies, and for whatever reason that monopoly status has been incredibly well protected by the SEC. They don’t grant “NRSRO” status to credit rating agencies unless the given agency can produce something like 10 letters from clients who will vouch for them providing credit ratings for at least 3 years. You can see why this is a hard business to break into.

The Roundtable was covered yesterday in the Wall Street Journal as well: Ratings Firms Steer Clear of an Overhaul – an unfortunate title if you are trying to be optimistic about the event today. From the WSJ article:

Mr. Franken’s amendment requires the SEC to create a board that would assign a rating firm to evaluate structured-finance deals or come up with another option to eliminate conflicts.

While lawsuits filed against S&P in February by the U.S. government and more than a dozen states refocused unflattering attention on the bond-rating industry, efforts to upend its reliance on issuers have languished, partly because of a lack of consensus on what to do.

I’m just kind of amazed that, given how dirty and obviously broken this industry is, we can’t do better than this. SEC, please start doing your job. How could allowing an open-source credit rating agency hurt our country? How could it make things worse?

Why we should break up the megabanks (#OWS)

Today is May Day, and my Occupy group and I are planning to join in the actions all over the city this afternoon. At 2:00 I’m going to be at Cooper Square, where Free University is holding a bunch of teach-ins, and I’m giving one entitled “Why we should break up the megabanks.” I wanted to get my notes for the talk down in writing beforehand here.

The basic reasons to break up the megabanks are these:

- They hold too much power.

- They cost too much.

- They get away with too much.

- They make things worse.

Each requires explanation.

Megabanks hold too much power

When Paulson went to Congress to argue for the bailout in 2008, he told them that the consequences of not acting would be a total collapse of the financial system and the economy. He scared Congress and the American people to such an extent that the banks managed to receive $700 billion with no strings attached. Even though half of that enormous pile of money was supposed to go to help homeowners threatened with foreclosures, almost none of it did, because the banks found other things to do with it.

The power of megabanks doesn’t only exert itself through the threat of annihilation, though. It also flows through lobbyists who water down Dodd-Frank (or really any policy that banks don’t like) and through “the revolving door,” the men and women who work for Treasury, the White House, and regulators about half the time and sit in positions of power in the megabanks the other half of their time, gaining influence and money and retiring super rich.

It is unreasonable to expect to compete with this kind of insularity and influence of the megabanks.

They cost too much

The bailout didn’t work and it’s still going on. And we certainly didn’t “make money” on it, compared to what the government could have expected if we had invested differently.

But honestly it’s too narrow to think about money alone, because what we really need to consider is risk. And there we’ve lost a lot: when we bailed them out, we took on the risk of the megabanks, and we have simply done nothing to return it. Ultimately the only way to get rid of that costly risk is to break them up once and for all to a size that they can reasonably and obviously be expected to fail.

Make no mistake about it: risk is valuable. It may not be quantifiable at a moment of time, but over time it becomes quite valuable and quantifiable indeed, in various ways.

One way is to think about borrowing costs and long-term default probabilities, and there the estimates have varied but we’ve seen numbers such as $83 billion per year modeled. Few people dispute that it’s the right order of magnitude.

They get away with too much

There doesn’t seem to be a limit to what the megabanks can get away with, which we’ve seen with HSBC’s money laundering from terrorists and drug cartels, we’ve seen with Jamie Dimon and Ina Drew lying to Congress about fucking with their risk models, we’ve seen with countless fraudulent and racist practices with mortgages and foreclosures and foreclosure reviews, not to mention setting up customers to fail in deals made to go bad, screwing municipalities and people with outrageous fees, shaving money off of retirement savings, and manipulating any and all markets and rates that they can to increase their bonuses.

The idea of a financial sector is to grease the wheels of commerce, to create a machine that allows the economy to work. But in our case we have a machine that’s taken over the economy instead.

They make things worse

Ultimately the best reason to break them up right now, the sooner the better, is that the incentives are bad and getting worse. Now that they live in a officially protected zone, there is even less reason for them then there used to be to rein in risky practices. There is less reason for them to worry about punishments, since the SEC’s habit of letting people off without jailtime, meaningful penalties, or even admitting wrongdoing has codified the lack of repercussions for bad behavior.

If we use recent history as a guide, the best job in finance you can have right now is inside a big bank, protected from the law, rather than working at a hedge fund where you can be nabbed for insider trading and publicly displayed as an example of the SEC’s new “toughness.”

What we need to worry about now is how bad the next crash is going to be. Let’s break up the megabanks now to mitigate that coming disaster.