Archive

HSBC Action today at noon

Here’s what I’m doing today at lunch time.

——

FOR IMMEDIATE RELEASE Monday, March 4, 2013

Occupy Wall Street Pickets At HSBC in New York

The action

HSBC To Issue Annual Earnings Report on Monday, March 4, 2013. These are the same unindicted criminals that admitted to money-laundering for drug cartels.

We Demand Justice for Executive Criminals & An End to “Too Big to Jail”!

Picket at HSBC New York Headquarters – Noon to 1:30pm

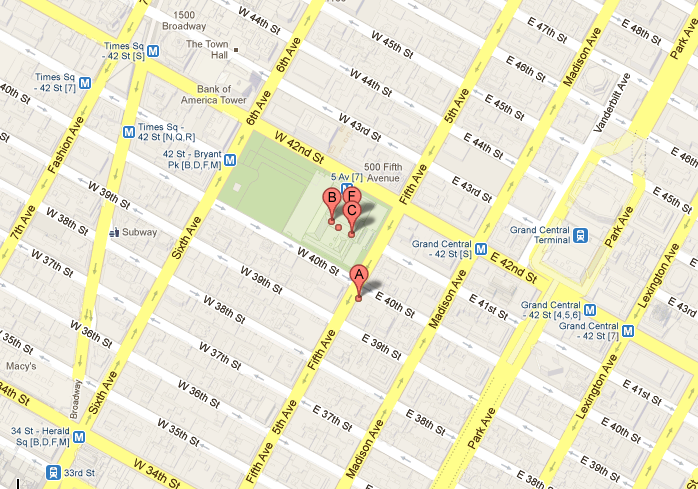

Gather on the steps of the New York Public Library Main Branch, 41st St. & Fifth Ave. See more at #OWSaltbanking and at our Facebook page for the event.

NEW YORK CITY – The “Occupy Wall Street – Alternative Banking” working group today continues its campaign to call on local, state and federal criminal and financial authorities to pursue prosecutions of executives at HSBC responsible for the bank’s admitted record of laundering money for drug cartels and alleged terrorists.

On Monday, March 4, as HSBC announces its annual earnings for 2012, OWS Alt Banking will rally at noon on the steps of the New York Public Library, Main Branch, across the street from HSBC’s New York headquarters.

The Story In Brief

In a recent settlement with the US Department of Justice, HSBC admitted to laundering billions of dollars for Mexican and Colombian drug cartels over many years. HSBC also admitted violating US sanctions regimes on Iran and on entities that the US government designates as “terrorist.”

Under the deal with DOJ, HSBC was forced to pay a $1.9 billion institutional penalty, which represents only six weeks worth of HSBC’s 2011 profits. The Justice Department agreed not to prosecute bank officials and other persons responsible for the admitted severe criminal conduct. All executive salaries and bonuses will be paid in full – some on deferred schedules. US financial authorities also declined to pull the criminal bank’s license to operate in the US.

Reportedly, authorities feared that jailing any of the megabank’s executives or shutting down its operations would cause its collapse and set off other bank collapses. This highlights the continuing systemic danger of “Too Big To Fail,” which also means “Too Big To Jail.” Thus OWS Alternative Banking is also calling on regulatory and legislative authorities finally to break up the big banks that dominate financial markets and can act with such impunity thanks to their sheer size.

Additional Context

OWS Alternative Banking Group points out that not to prosecute the HSBC executives responsible for money laundering to the full extent of the law diminishes the law and sends the wrong message. It creates an incentive for other banks to engage in the same criminal conduct.

Banks are being told that if they are big enough, they can commit any institutional crime without fear that personal punishments will follow, and in the confidence that institutional penalties will be minor in comparison to the profits made by breaking the law.

What message does this send to the American people, and to the world? “The war on drugs” and “the war on terror” rage on as centerpieces of US global policy.

In the United States, hundreds of thousands of people, predominantly people of color, have been imprisoned for often minor drug offenses. This has destroyed the futures of many young people and contributed to the biggest prison-industrial complex in the world.

In Mexico and Colombia, the US government supports a “drug war” in which literally thousands of people are murdered, often by the military personnel of those nations acting as death squads. In Pakistan, Yemen and other nations, US military drones bomb targeted persons – often killing their families or neighbors – on suspicion of “terrorism,” without trial or appeal.

In the US, executives at Islamic charities accused of funneling money to organizations designated as terrorist have received multiple life sentences. How is this different from HSBC’s conduct in helping to maintain the finances of drug cartels and alleged terrorists? Money laundering is absolutely essential to the business of the illegal drug trade. Furthermore, money launderers make the fattest profits out of all participants in the illegal drug trade.

Why are the banker-criminals getting a free pass? Why do we allow a two-tier justice system, with harsh punishments for minor drug offenders and rewards and impunity for the biggest offenders of all?

Therefore OWS Alternative Banking is asking for fair prosecution of the HSBC criminals and for ethical practices and staffing to replace the blatant abuse of customer money and good will. HSBC’s license to operate in the United States must be pulled.

The further message is to break up the big banks. They can no longer be considered too big too fail and allowed to commit blatant crimes of fraud and money laundering at US taxpayers’ expense.

Given the United Nations estimate of $400 billion in drug money laundered annually, it is nearly impossible that this enormous volume of dirty cash does not in large part go through the other big Wall Street and City of London banks.

“IT IS A DARK DAY FOR THE RULE OF LAW.” – New York Times, 12/11/2012

“Apparently non-violent demonstration against corrupt banking is subject to more criminal scrutiny than actual corrupt banking.” – Village Voice, 12/26/2012

Is mathematics a vehicle for control fraud?

Bill Black

A couple of nights I ago I attended this event at Columbia on the topic of “Rent-Seeking, Instability and Fraud: Challenges for Financial Reform”.

The event was great, albeit depressing – I particularly loved Bill Black‘s concept of control fraud, which I’ll talk more about in a moment, as well as Lynn Turner‘s polite description of the devastation caused by the financial crisis.

To be honest, our conclusion wasn’t a surprise: there is a lack of political will in Congress or elsewhere to fix the problems, even the low-hanging obvious criminal frauds. There aren’t enough actual police to take on the job of dealing with the number of criminals that currently hide in the system (I believe the statistic was that there are about 1,000,000 people in law enforcement in this country, and 2,500 are devoted to white-collar crime), and the people at the top of the regulatory agencies have been carefully chosen to not actually do anything (or let their underlings do anything).

Even so, it was interesting to hear about this stuff through the eyes of a criminologist who has been around the block (Black was the guy who put away a bunch of fraudulent bankers after the S&L crisis) and knows a thing or two about prosecuting crimes. He talked about the concept of control fraud, and how pervasive control fraud is in the current financial system.

Control Fraud

Control fraud, as I understood him to describe it, is the process by which a seemingly legitimate institution or process is corrupted by a fraudulent institution to maintain the patina of legitimacy.

Once you say it that way, you recognize it everywhere, and you realize how dirty it is, since outsiders to the system can’t tell what’s going on – hey, didn’t you have overseers? Didn’t they say everything was checking out ok? What the hell happened?

So for example, financial firms like Bank of America used control fraud in the heart of the housing bubble via their ridiculous accounting methods. As one of the speakers mentioned, the accounting firm in charge of vetting BofA’s books issued the same exact accounting description for many years in the row (literally copy and paste) even as BofA was accumulating massive quantities of risky mortgage-backed securities (update: I’ve been told it’s called an “Auditors Report” and it has required language. But surely not all the words are required? Otherwise how could it be called a report?). In other words, the accounting firm had been corrupted in order to aid and abet the fraud.

“Financial Innovation”

To get an idea of the repetitive nature and near-inevitability of control fraud, read this essay by Black, which is very much along the lines of his presentation on Tuesday. My favorite passage is this, when he addresses how our regulatory system “forgot about” control fraud during the deregulation boom of the 1990’s:

On January 17, 1996, OTS’ Notice of Proposed Rulemaking proposed to eliminate its rule requiring effective underwriting on the grounds that such rules were peripheral to bank safety.

“The OTS believes that regulations should be reserved for core safety and soundness requirements. Details on prudent operating practices should be relegated to guidance.

Otherwise, regulated entities can find themselves unable to respond to market innovations because they are trapped in a rigid regulatory framework developed in accordance with conditions prevailing at an earlier time.”

This passage is delusional. Underwriting is the core function of a mortgage lender. Not underwriting mortgage loans is not an “innovation” – it is a “marker” of accounting control fraud. The OTS press release dismissed the agency’s most important and useful rule as an archaic relic of a failed philosophy.

Here’s where I bring mathematics into the mix. My experience in finance, first as a quant at D.E. Shaw, and then as a quantitative risk modeler at Riskmetrics, convinced me that mathematics itself is a vehicle for control fraud, albeit in two totally different ways.

Complexity

In the context of hedge funds and/or hard-core trading algorithms, here’s how it works. New-fangled complex derivatives, starting with credit default swaps and moving on to CDO’s, MBS’s, and CDO+’s, got fronted as “innovation” by a bunch of economists who didn’t really know how markets work but worked at fancy places and claimed to have mathematical models which proved their point. They pushed for deregulation based on the theory that the derivatives represented “a better way to spread risk.”

Then the Ph.D.’s who were clever enough to understand how to actually price these instruments swooped in and made asstons of money. Those are the hedge funds, which I see as kind of amoral scavengers on the financial system.

At the same time, wanting a piece of the action, academics invented associated useless but impressive mathematical theories which culminated in mathematics classes throughout the country that teach “theory of finance”. These classes, which seemed scientific, and the associated economists described above, formed the “legitimacy” of this particular control fraud: it’s math, you wouldn’t understand it. But don’t you trust math? You do? Then allow us to move on with rocking our particular corner of the financial world, thanks.

Risk

I also worked in quantitative risk, which as I see it is a major conduit of mathematical control fraud.

First, we have people putting forward “risk estimates” that have larger errorbars then the underlying values. In other words, if we were honest about how much we can actually anticipate price changes in mortgage backed securities in times of panic, then we’d say something like, “search me! I got nothing.” However, as we know, it’s hard to say “I don’t know” and it’s even harder to accept that answer when there’s money on the line. And I don’t apologize for caring about “times of panic” because, after all, that’s why we care about risk in the first place. It’s easy to predict risk in quiet times, I don’t give anyone credit for that.

Never mind errorbars, though- the truth is, I saw worse than ignorance in my time in risk. What I actually saw was a rubberstamping of “third part risk assessment” reports. I saw the risk industry for what it is, namely a poor beggar at the feet of their macho big-boys-of-finance clients. It wasn’t just my firm either. I’ve recently heard of clients bullying their third party risk companies into allowing them to replace whatever their risk numbers were by their own. And that’s even assuming that they care what the risk reports say.

Conclusion

Overall, I’m thinking this time is a bit different, but only in the details, not in the process. We’ve had control fraud for a long long time, but now we have an added tool in the arsenal in the form of mathematics (and complexity). And I realize it’s not a standard example, because I’m claiming that the institution that perpetuated this particular control fraud wasn’t a specific institution like Bank of America, but rather then entire financial system. So far it’s just an idea I’m playing with, what do you think?

Break up the megabanks already (#OWS)

For the past few months at Occupy we’ve been focusing more and more on having a single message and goal. That has been to break up the big banks.

What’s great about this goal is that it’s a non-partisan issue; there is growing consensus (among non-bankers) from the left and the right that the current situation is outrageous and untenable. What’s not great, of course, is that the situation is so easy to spot because it’s so heinous.

Yesterday another voice joined the Break-Up-The-Big-Banks chorus in the form of an editorial at Bloomberg (hat tip Hannah Appel). They wrote a persuasive piece on breaking up the big banks based on simple arithmetic involving bank profits and taxpayer subsidy. Even the title fits that description: “Why Should Taxpayers Give Big Banks $83 Billion a Year?”. Here’s an excerpt from the editorial (emphasis mine):

…Banks have a powerful incentive to get big and unwieldy. The larger they are, the more disastrous their failure would be and the more certain they can be of a government bailout in an emergency. The result is an implicit subsidy: The banks that are potentially the most dangerous can borrow at lower rates, because creditors perceive them as too big to fail.

Lately, economists have tried to pin down exactly how much the subsidy lowers big banks’ borrowing costs. In one relatively thorough effort, two researchers — Kenichi Ueda of the International Monetary Fund and Beatrice Weder di Mauro of the University of Mainz — put the number at about 0.8 percentage point. The discount applies to all their liabilities, including bonds and customer deposits.

Big Difference

Small as it might sound, 0.8 percentage point makes a big difference. Multiplied by the total liabilities of the 10 largest U.S. banks by assets, it amounts to a taxpayer subsidy of $83 billion a year. To put the figure in perspective, it’s tantamount to the government giving the banks about 3 cents of every tax dollar collected.

The top five banks — JPMorgan, Bank of America Corp., Citigroup Inc., Wells Fargo & Co. and Goldman Sachs Group Inc. – – account for $64 billion of the total subsidy, an amount roughly equal to their typical annual profits (see tables for data on individual banks). In other words, the banks occupying the commanding heights of the U.S. financial industry — with almost $9 trillion in assets, more than half the size of the U.S. economy — would just about break even in the absence of corporate welfare. In large part, the profits they report are essentially transfers from taxpayers to their shareholders.

Next time someone tells me I want to take money out of rich people’s pockets (and that makes me a free market hater), I’m going to remind them that every time I pay taxes, 3 cents out of every dollar (that I know of) goes directly to the banks for no good reason whatsoever except the fact that they have the lobbyists to support this system. They’re bullies, and I hate bullies.

So no, I’m not suggesting we take honestly earned money out of the pockets of those who deserve it, I’m suggesting we stop stuffing insiders’ pockets with our money. Big difference.

But it’s not just money I object to – it’s future liability. There’s now an established track record of discovered criminal acts that don’t get anyone at the big banks in trouble. We are setting ourselves up for an even bigger bailout of some form soon, one that we taxpayers really may not be able to afford.

I think of the too-big-to-fail problem as like having an alcoholic brother-in-law who not only sleeps on your couch every night but also knows the PIN code on your ATM card. The money is irksome, no doubt, but what if that guy fell asleep smoking a cigarette and me and my kids die in the resulting fiery inferno? And it’s not that I think all addicts could be magically cured, but I don’t want them to have access to my personal stuff. Get them out of my house.

So can we break up the megabanks already? I’d really like to stop worrying about them because I have better things to do.

NYC data hackathons, past and future: Politics, Occupy, and Climate change (#OWS)

The past: Money in politics

First thing’s first, I went to the Bicoastal Datafest a few weekends ago and haven’t reported back. Mostly that’s because I got sick and didn’t go on the second day, but luckily other people did, like Kathy Kiely from the Sunlight Foundation, who wrote up this description of the event and the winning teams’ projects.

And hey, it turns out that my new company shares an office with Harmony Institute, whose data scientist Burton DeWilde was on the team that won “Best in Show” for their orchestral version of the federal government’s budget.

Another writeup of the event comes by way of Michael Lawson, who worked on the team that set up an accounting fraud detection system through Benford’s Law. I might be getting a guest blog post about this project through another one of its team members soon.

And we got some good progress on our DataKind/ Sunlight Foundation money-in-politics project as well, thanks to DataKind intern Pete Darche and math nerds Kevin Wilson and Johan de Jong.

The future one week from now: Occupy

Next up, on March 1st and 2nd at CUNY Graduate Center is this data hackathon called OccupyData (note this is a Friday and Saturday, which is unusual). You can register for the event here.

It’s a combination of an Occupy event and a datafest, so obviously I am going to try to go. The theme is general – data for the 99% – but there’s a discussion on this listserv as to the various topics people might want to focus on (Aaron Swartz and Occupy Sandy are coming up for example). I’m looking forward to reporting back (or reporting other people’s report-backs if my kids don’t let me go).

The future two weeks from now: Climate change

Finally, there’s this datathon, which doesn’t look open to registration, but which I’ll be participating in through my work. It’s stated goal is “to explore how social and meteorological data can be combined to enhance social science research on climate change and cities.” The datathon will run Saturday March 9th – Sunday March 10th, 2013, starting noon Saturday, with final presentations at noon Sunday. I’ll try to report back on that as well.

Five false myths that make liberals feel good

1. The U.S. has a progressive tax code

Actually, no. Not when you include all kinds of taxes. From this Economist column, which states “The fact of the matter is that the American tax code as a whole is almost perfectly flat.”

2. The U.S. is a land of opportunity

Actually, the mobility of the U.S. is worse than Canada’s or anywhere in Western Europe. From the NY Times article:

Despite frequent references to the United States as a classless society, about 62 percent of Americans (male and female) raised in the top fifth of incomes stay in the top two-fifths, according to research by the Economic Mobility Project of the Pew Charitable Trusts. Similarly, 65 percent born in the bottom fifth stay in the bottom two-fifths.

3. The bailout worked

Actually, the bailout is still happening, as we see from monthly discoveries such as this recent back-door bailout, and it hasn’t worked for the majority of the people it was intended for, namely people stuck with unreasonable mortgages (people forget this sometimes, but the first half of TARP was for the banks, the second half was for mortgage holders). From a NY Times Op-ed by Elizabeth Lynch (emphasis mine):

So a lender can forgive a second mortgage — which in the event of foreclosure would be worthless anyway — and under the settlement claim credits for “modifying” the mortgage, while at the same time it or another bank forecloses on the first loan. The upshot, of course, is that the people the settlement was designed to protect keep losing their homes.

4. Our private data is protected by our government

Although on the one hand the CIA recently admitted to full monitoring of Facebook using fake personas (h/t Chris Wiggins), the U.S. government does not in fact take great pains to protect the data they collect about its citizens. Moreover, government workers who complain about the porous data protection are punished instead of protected, as is explained in this Times piece. My favorite quote is this bit of common sense:

Susan Landau, a Guggenheim fellow in cyber security, privacy and public policy, says companies and agencies are unlikely to improve data security without the threat of penalty.

“What are the personal consequences for employees who allow data breaches to happen?” Ms. Landau asks. “Until people lose their jobs, nothing is going to change.”

5. We are recovering from the great recession

From 2009-2011, the top 1% captured 121% of all income gains (h/t Matt Stoller).

Who says you can’t perform at 121%? Turns out you can if other people are actually losing income while you’re getting increasingly rich.

Don’t get me wrong, corporate profits have done even better – a 171% gains since we’ve had Obama. But I’d go by things that matter to the 99%, so payrolls and jobs. Payrolls are flat and we still have 5 million fewer jobs, so I’d say it’s not much of a recovery.

HSBC protest yesterday (#OWS)

Here’s a picture from yesterday (thanks Pam!):

This was near the end when some people had already left. We met on the steps of the NYPL as above but in between we went across the street and marched in front of HSBC, which was barricaded by the police. Indeed there were as many police, or more, as protesters. We chanted things like, “Stop and Frisk HSBC!” or “The banks got bailed out, we got sold out” but my favorite chant was a song Nick and Manny made up during the event:

Bankers and drug lords sittin’ in a tree

K-I-S-S-I-N-G

First comes love, then comes prrofit,

Then comes a settlement from the Justice De-partment!

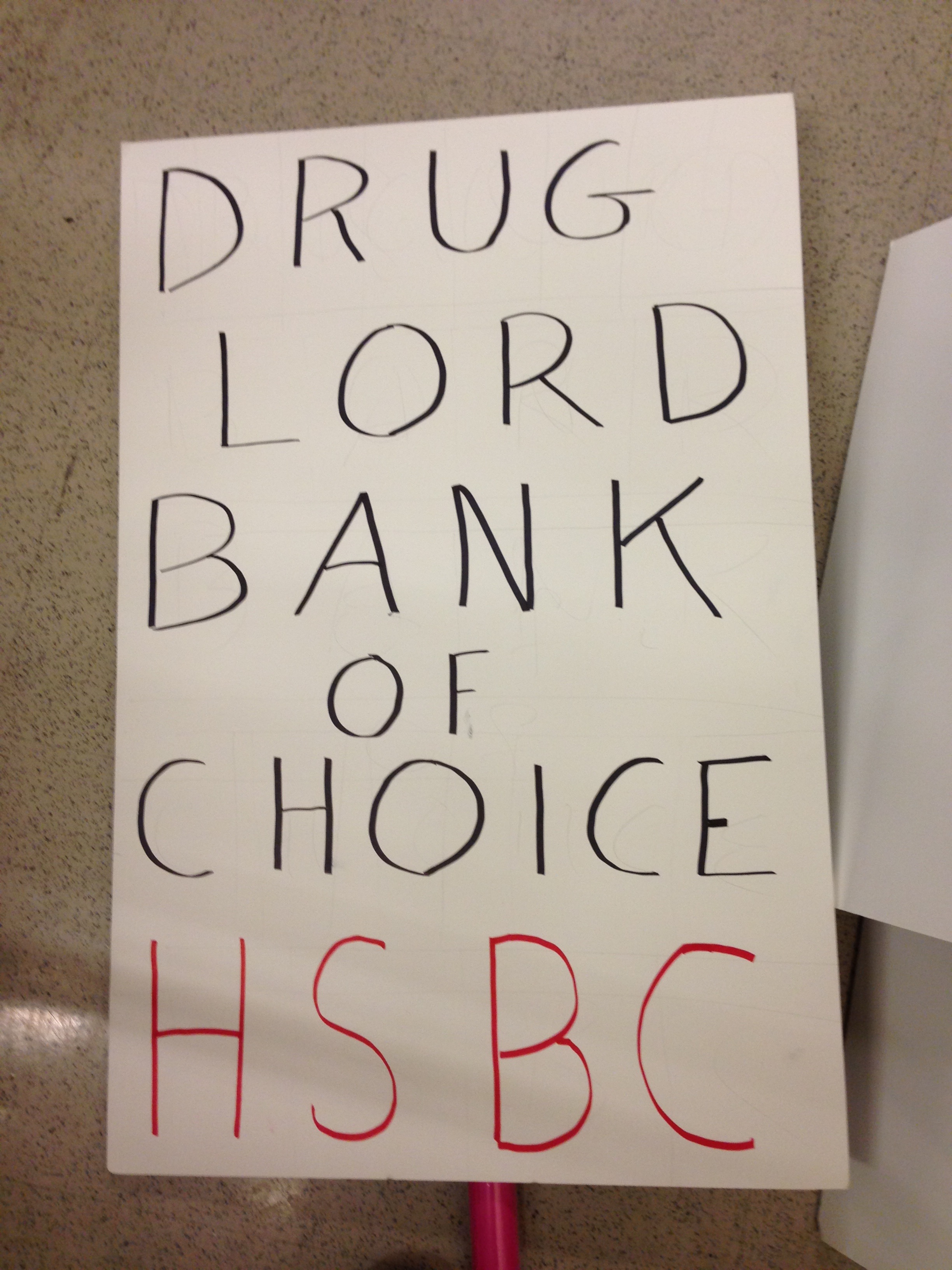

Here’s a pic from the marching part with an appropriate Valentine’s Day theme (note the barricades behind the protesters):

And here’s me with my sandwich board. The front (note the long line of police motorcycles behind me):

And the back:

Also check out Taibbi’s HSBC article from yesterday.

Occupy HSBC: Valentine’s Day protest at noon #OWS

Protest with #OWS Alternative Banking Group

I’m writing to invite you to a protest against mega-bank HSBC at noon on Valentine’s Day (Thursday) starting on the steps of the New York Public Library at 42nd and 5th. Details are here but it’s the big green box on the map on the Fifth Avenue side:

Why are we protesting?

Like you, I’m sure, I’d like nothing more than to stop worrying about shit that goes on in our country’s banks.

We have better things to do with out time than to get annoyed over enormous bonuses being given to idiots for their repeated failures. We’re frankly exhausted from the outrage.

I mean, the average person doesn’t have a job where they get an $11 million bonus instead of a $22 million dollar bonus when they royally screw up. Outside the surreal realm of international banking, the normal response to screw-ups on that level is to get fired.

You might expect a company that has been caught criminally screwing minorities out of fair contracts might be at risk of being closed down, but in this day and age you’d know that big banks, or TIBACO (too interconnected, big, and complex to oversee) institutions, as we in Alt Banking like to call them, are immune to such action.

There’s a clear evolving standard of treatment in the banking sector when it comes to criminal activity:

- the powers that be (SEC, DOJ, etc.) make a huge production over the severity of the fine,

- which is large in dollar amounts but

- usually represents about 10% of the overall profit the given banks made during their exploit.

- Nobody ever goes to jail, and

- the shareholders pay the fine, not the perpetrators.

- The perps get somewhat diminished bonuses. At worst.

The bottomline: we have an entire class of citizens that are immune to the laws because they are considered too important to our financial stability.

But why HSBC?

HSBC is a perfect example of this. An outrageous example.

HSBC didn’t get a bailout in 2008 like many other banks, even though they were ranked #2 in subprime mortgage lending. But that’s not because they didn’t lose money – in fact they lost $6 billion but somehow kept afloat.

And now we know why.

Namely, they were money-laundering, earning asstons by facilitating drugs and terrorism. This was blood money, make no mistake, and it went directly into the pockets of HSBC bankers in the form of bonuses.

When this years-long criminal mafia activity was discovered, nothing much happened beyond a fine, as per usual. Well, to be honest, they were fined $1.9 billion dollars, which is a lot of money, but is only 5 weeks of earnings for the mammoth institution – depending on the way you look at it, HSBC is the 2nd largest bank in the world.

Too big to jail

And that’s when “Too big to fail” became “Too big to jail.” Even the New York Times was outraged. From their editorial page:

Federal and state authorities have chosen not to indict HSBC, the London-based bank, on charges of vast and prolonged money laundering, for fear that criminal prosecution would topple the bank and, in the process, endanger the financial system. They also have not charged any top HSBC banker in the case, though it boggles the mind that a bank could launder money as HSBC did without anyone in a position of authority making culpable decisions.

Clearly, the government has bought into the notion that too big to fail is too big to jail. When prosecutors choose not to prosecute to the full extent of the law in a case as egregious as this, the law itself is diminished. The deterrence that comes from the threat of criminal prosecution is weakened, if not lost.

National Threat

You may recall that there was an extensive FBI investigation of OWS before Zuccotti Park was even occupied.

Ironic? As the Village Voice said, “apparently non-violent demonstration against corrupt banking is subject to more criminal scrutiny than actual corrupt banking.”

Question for you: which is the bigger national security threat, OWS or HSBC?

We demand

HSBC needs its license revoked, and there need to be prosecutions. Those who are guilty need to be punished or else we have an official invitation to criminal acts by bankers. We simply can’t live in a country which rewards this kind of behavior.

Mind you, this isn’t just about HSBC. This is about all the megabanks. Citi or BoA are exempt from prosecution, too. Our message needs to be “break up the megabanks”.

I’ll end with what Matt Taibbi had to say about the HSBC settlement:

On the other hand, if you are an important person, and you work for a big international bank, you won’t be prosecuted even if you launder nine billion dollars. Even if you actively collude with the people at the very top of the international narcotics trade, your punishment will be far smaller than that of the person at the very bottom of the world drug pyramid. You will be treated with more deference and sympathy than a junkie passing out on a subway car in Manhattan (using two seats of a subway car is a common prosecutable offense in this city). An international drug trafficker is a criminal and usually a murderer; the drug addict walking the street is one of his victims. But thanks to Breuer, we’re now in the business, officially, of jailing the victims and enabling the criminals.

Join us on Valentine’s Day at noon on the steps of the New York Public Library and help us Occupy HSBC. Please redistribute widely!

HSBC Valentine’s Day action (#OWS)

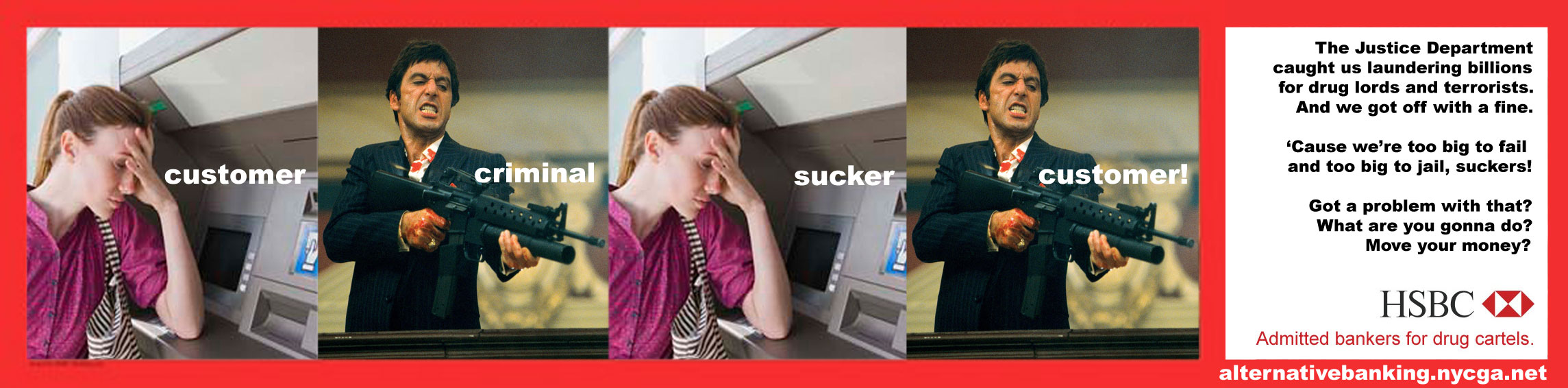

We in the Alt Banking group are planning a protest against “too big to jail” bank HSBC for Valentine’s Day. As soon as we started the planning we realized they are utterly ripe for satire with their ridiculous airport posters like this one:

Here’s a new poster for them, courtesy of Nick from our group (and crossposted from the Alt Banking blog):

Readers, can you help us come up with posters and slogans for the event? Bonus if it has to do with a Valentine’s Day theme, along the lines of “You broke my heart, HSBC!” or if it riffs on their slogan, “The World’s Local Bank”. We will be making posters and flyers with this stuff next Sunday afternoon, if you’re going to be up near Columbia you should join us.

Thanks for your help! If you tweet this, don’t forget to use the hashtag #HSBC as a gift to those guys.

update: Public Citizen in Maryland is attempting to revoke HSBC’s bank charter.

Alt-Banking calls on Senate to defend Main Street against Wall Street (#OWS)

This is crossposted from the blog of the Alternative Banking Working group of #OWS.

Dear Senators,

It is now up to you to restore the integrity of the Department of the Treasury.

As the Department’s web site states, Treasury’s job is to:

“Maintain a strong economy and create economic and job opportunities by promoting the conditions that enable growth and stability…protecting the integrity of the financial system, and manage the U.S. Government’s finances and resources effectively.”

President Obama’s nominee, Jacob Lew, does not measure up to the task.

Since the days of the Clinton Administration, the office of the Treasury Secretary has morphed into the custodian of Wall Street interests, allowing fraudulent banking practices to lead us into a recession, paying little or no heed to the concerns of Main Street about economic growth or jobs. Moreover, unlike the George W. Bush presidency where Enron executives were jailed — little has been done since the latest crisis to prosecute the people responsible for the widespread criminality and total disregard of ethics and values in finance.

The new Treasury Secretary should be an individual who looks out for the 99%, not a Timothy Geithner clone who would rather save financial players than enforce the law. We need someone who will focus on the productive economy and jobs. We need someone who will push back against Wall Street, not someone who will do their bidding.

Jacob Lew’s tenure at the original too-big-to-fail bank, Citigroup, has disqualified him. He received a $900,000 bonus from Citi in 2008, essentially paid out of the taxpayer bailout, just before he returned to government. At best this has the “appearance of impropriety”.

As HSBC’s “too big to jail’ settlement shows, the too-big-to-fail problem persists. We need a Treasury Secretary who will work to address this. Despite being near the heart of the storm, or perhaps because he was at Citigroup, Jack Lew shows no recognition that the current structure of the banking system is the heart of the problem. We must block his appointment.

Criminality and greed are embedded in the culture of the financial system and only major reform will get rid of it. Please join us in our efforts to reject Jacob Lew and ask President Obama to nominate someone who can truly live up to the mandate of the U.S. Treasury.

Sincerely,

Members of the OWS Alternative Banking Group

Marni Halasa

Josh Snodgrass

Hannah Appel

Linda Brown

Nicholas Levis

Cathy O’Neil

Anchard Scott

Yves Smith

Akshat Tewary

Is mathbabe a terrorist or a lazy hippy? (#OWS)

The Occupy narrative, put forth by mainstream media such as the New York Times and led by friends of Wall Street such as Andrew Ross Sorkin, is sad and pathetic. A bunch of lazy hippies, with nothing much in the way of organized demands, and, by the way, nothing much in the way of reasonable grievances either. And moreover, according to Sorkin, Occupy had fizzled as of its first anniversary.

To an earnest reader of the New York Times, in other words, there’s no there there, and we can move on. Nothing to see.

From my perspective as an active occupier, this approach of casual indifference has seemed oddly inconsistent with the interest in the #OWS Alternative Banking group from other nations. I’ve been interviewed by mainstream reporters from the UK, Belgium, Canada, France, Germany, and Japan, and none of them seemed as willing to dismiss the movement or our group quite as actively as the New York Times has.

And then there was the country-wide clearing of the parks, which seemed mysteriously coordinated, and the press (yes, the New York Times again) knowing when and where it would happen somehow, and taking pictures of the police gathering beforehand.

Police preparing to clear Zuccotti Park

Really it was enough to make one consider a conspiracy theory between the authorities and mainstream media.

I’m not one for conspiracy theories, though, so I let it pass. But other people were more vigilant than myself after the coordinated clearings, and, as I learned from this Naked Capitalism post, first Truthout attempted a FOIA request to the FBI, and was told that “no documents related to its infiltration of Occupy Wall Street existed at all”, and then the Partnership for Civil Justice filed a FOIA request which was served.

Turns out there was quite a bit of worry about Occupy among the FBI, and Homeland Security, even before Zuccotti was occupied. Occupy was dubbed a terrorist organization, for example. See the heavily redacted details here.

I guess to some extent this makes sense, as the roots of Occupy are outwardly anarchist, and there is a history of anarchist bombings of the New York Stock Exchange. I guess this could also explain the meetings the FBI and Homeland Security had with the banks and the stock exchange. They wanted to cover their asses in case the anarchists were violent.

On the other hand, by the time they cleared the park the movement was openly peaceful. You don’t get called lazy dirty hippies because you’re throwing bombs into buildings, after all. And the coordination of the clearing of the parks is no longer a conspiracy, it’s verified. They were clearly afraid of us.

So which is it, lazy hippy or scary terrorist? There’s a baffling disconnect.

The truth, in this case, is not in between. Instead, Occupy lives in a different plane altogether, as I’ll explain, and this in turn explains both the “lazy” and the “scary” narrative.

The “lazy” can be put to rest here and now, it’s just wrong. The response and relief efforts of Occupy Sandy has convincingly shown that laziness is not an underlying principle of Occupy.

Occupy Sandy volunteers

But Occupy Sandy did expose some principles that we occupiers have known to be true since the beginning:

- that we must overcome or even ignore structured and rigid rules to help one another at a human level,

- that we must connect directly with suffering and organically respond to it as we each know how to, depending on circumstances, and

- that moral and ethical responsibilities are just plain more important than rules.

Such a nuanced concept might seem, from the outside, to be a bunch of meditating hippies, although you’d have to kind of want to see that to think that’s all it is. So that explains the “lazy” narrative to me: if you don’t understand it, and if you don’t want to bother to look carefully, then just describe the surface characteristics.

Second, the “scary” part is right, but it’s not scary in the sense of guns and bombs – but since the cops, the FBI, and Homeland Security speak in that language, the actual threat of Occupy is again lost in translation.

It’s our ideas that threaten, not our violence. We ignore the rules, when they oppress and when they make no sense and when they serve to entrench an already entrenched elite. And ignoring rules is sometimes more threatening than breaking them.

Is mathbabe a terrorist? Is the Alternative Banking group a threat to national security because we discuss breaking up the big banks without worrying about pissing off major campaign contributors?

I hope we are a threat, but not to national security, and not by bombs or guns, but by making logical and moral sense and consistently challenging a rigged system.

I’m planning to file a FOIA request on myself and on the Alt Banking group to see what’s up.

If Barofsky heads the SEC I’ll work for it

Neil Barofsky visited my Occupy group, Alternative Banking, this past Sunday. He was awesome.

We discussed the credit crisis, the recent outrageous HSBC ruling which quantified the cost banks near for money laundering for terrorists and drug lords at below cost, and the hopelessness, or on a good day the hope, of having a financial and regulatory system that will eventually work.

We discussed the incentives in the HAMP set-up, which explain why very few homeowners have actually received lasting relief from unaffordable mortgages. We discussed the incentives for fraud and other criminal behavior in the absence of real punishment, that too much money is being spent pursuing insider training because that’s what people understand how to do, and we discussed the reluctance of the regulators to litigate tough cases. We talked about how change has to come from the top, because all of these organizations are super hierarchical and require political will to get things done.

In the past year I was offered a job at the SEC, working as a quant in the enforcement division. Although I want to help sort out this mess, I haven’t felt that this job, which is relatively junior, would allow me to do that meaningfully.

But I came away from the meeting with Barofsky with this feeling: if we had someone in charge at the SEC like him who could speak truth to power and who is smart enough to see through economic jargon and bullshit well enough to understand incentives for fraud and lying, then I’d work there in a heartbeat.

Let’s just hope it doesn’t take another world-wide financial crisis before we get someone like that.

On Reuters talking about Occupy

I was interviewed a couple of weeks ago and it just got posted here:

Anti-black Friday ideas? (#OWS)

I’m trying to put together a post with good suggestions for what to do on Black Friday that would not include standing in line waiting for stores to open.

Speaking as a mother of 3 smallish kids, I don’t get the present-buying frenzy thing, and it honestly seems as bad as any other addiction this country has gotten itself into. In my opinion, we’d all be better off if pot were legalized country-wide but certain categories of plastic purchases were legal only through doctor’s orders.

One idea I had: instead of buying things your family and loved ones don’t need, help people get out of debt by donating to the Rolling Jubilee. I discussed this yesterday in the #OWS Alternative Banking meeting, it’s an awesome project.

Unfortunately you can’t choose whose debt you’re buying (yet) or even what kind of debt (medical or credit card etc.) but it still is an act of kindness and generosity (towards a stranger).

It begs the question, though, why can’t we buy the debt of people we know and love and who are in deep debt problems? Why is it that debt collectors can buy this stuff but consumers can’t?

In a certain sense we can buy our own debt, actually, by negotiating directly with debt-collectors when they call us. But if a debt-collector offers to let you pay 70 cents on the dollar, it probably means he or she bought it at 20 cents on the dollar; they pay themselves and their expenses (the daily harassing phone calls) with the margin, plus they buy a bunch of peoples’ debts and only actually successfully scare some of them into paying anything.

Question for readers:

- Is there a way to get a reasonable price on someone’s debt, i.e. closer to the 20 cents figure? This may require understanding the consumer debt market really well, which I don’t.

- Are there other good alternatives to participating in Black Friday?

Free people from their debt: Rolling Jubilee (#OWS)

Do you remember the group Strike Debt? It’s an offshoot of Occupy Wall Street which came out with the Debt Resistors Operation Manual on the one-year anniversary of Occupy; I blogged about this here, very cool and inspiring.

Well, Strike Debt has come up with another awesome idea; they are fundraising $50,000 (to start with) by holding a concert called the People’s Bailout this coming Thursday, featuring Jeff Mangum of Neutral Milk Hotel, possibly my favorite band besides Bright Eyes.

Actually that’s just the beginning, a kick-off to the larger fundraising campaign called the Rolling Jubilee.

The main idea is this: once they have money, they buy people’s debts with it, much like debt collectors buy debt. It’s mostly pennies-on-the-dollar debt, because it’s late and there is only a smallish chance that, through harassment legal and illegal, they will coax the debtor or their family members to pay.

But instead of harassing people over the phone, the Strike Debt group is simply going to throw away the debt. They might even call people up to tell them they are officially absolved from their debt, but my guess is nobody will answer the phone, from previous negative conditioning.

Get tickets to the concert here, and if you can’t make it, send donations to free someone from their debt here.

In the meantime enjoy some NMH:

Money market regulation: a letter to Geithner and Schapiro from #OWS Occupy the SEC and Alternative Banking

#OWS working groups Occupy the SEC and Alternative Banking have released an open letter to Timothy Geithner, Secretary of the U.S. Treasury, and Mary Schapiro, Chairman of the SEC, calling on them to put into place reasonable regulation of money market funds (MMF’s).

Here’s the letter, I’m super proud of it. If you don’t have enough context, I give a more background below.

What are MMFs?

Money market funds make up the overall money market, which is a way for banks and businesses to finance themselves with short-term debt. It sounds really boring, but as it turns out it’s a vital issue for the functioning of the financial system.

Really simply put, money market funds invest in things like short-term corporate debt (like 30-day GM debt) or bank debt (Goldman or Chase short-term debt) and stuff like that. Their investments also include deposits and U.S. bonds.

People like you and me can put our money into money market funds via our normal big banks like Bank of America. In face I was told by my BofA banker to do this around 2007. He said it’s like a savings account, only better. If you do invest in a MMF, you’re told how much over a dollar your investments are worth. The implicit assumption then is that you never actually lose money.

What happened in the crisis?

MMF’s were involved in some of the early warning signs of the financial crisis. In August and September 2007, there was a run on subprime-related asset backed commercial paper.

In 2008, some of the funds which had invested in short-term Lehman Brother’s debt had huge problems when Lehman went down, and they “broke the buck”. This caused wide-spread panic and a bunch of money market funds had people pulling money from them.

In order to avoid a run on the MMF’s, the U.S. stepped in and guaranteed that nobody would actually lose money. It was a perfect example of something we had to do at the time, because we would literally not have had a functioning financial system given how central the money markets were at the time, in financing the shadow banking system, but something we should have figured out how to improve on by now.

This is a huge issue and needs to be dealt with before the next crisis.

What happened in 2010?

In 2010, regulators put into place rules that tightened restrictions within a fund. Things like how much cash they had to have on hand (liquidity requirements) and how long the average duration of their investments could be. This helped address the problem of what happens within a given fund when investors take their money out of that fund.

What they didn’t do in 2010 was to control systemic issues, and in particular how to make the MMF’s robust to large-scale panic.

What about Schapiro’s two MMF proposals?

More recently, Mary Schapiro, Chairman of the SEC, made two proposals to address the systemic issues. In the first proposal, instead of having the NAV’s set at one dollar, everything is allowed to float, just like every other kind of mutual fund. The industry didn’t like it, claiming it would make MMF’s less attractive.

In the second proposal, Schapiro suggesting that MMF managers keep a buffer of capital and that a new, weird lagged way for people to remove their money from their MMF’s, namely if you want to withdraw your funds you’ll only get 97%, and later (after 30 days) you’ll get 3% if the market doesn’t take a loss. If it does take a loss, will get only part of that last 3%.

The goal of this was to distribute losses more evenly, and to give people pause in times of crisis from withdrawing too quickly and causing a bank-like run.

Unfortunately, both of Schapiro’s proposals didn’t get passed by the 5 SEC Commissioners in August 2012 – it needed a majority vote, but they only got 2.

What happened when Geithner and Blackrock entered the picture?

The third, most recent proposal, comes out of the FSOC, a new meta-regulator, whose chair is Timothy Geithner. The guys proposed to the SEC in a letter dated September 27th that they should do something about money market regulation. Specifically, the FSOC letter suggests that either the SEC should go with one of Schapiro’s two ideas or a new third one.

The third one is again proposing a weird way for people to take their money out of a MMF, but this time it definitely benefits people who are “first movers”, in other words people who see a problem first and get the hell out. It depends on a parameter, called a trigger, which right now is set at 25 basis points (so 25 cents if you have $100 invested).

Specifically, if the value of the fund falls below 99.75, any withdrawal from that point on will be subject to a “withdrawal fee,” defined to be the distance between the fund’s level and 100. So if the fund is at 99.75, you have to pay a 25 cent fee and you only get out 99.50, whereas if the fund is at 99.76, you actually get out 100. So in other words, there’s an almost 50 cents difference at this critical value.

Is this third proposal really any better than either of Schapiro’s first two?

The industry and Timmy: bff’s?

Here’s something weird: on the same day the FSOC letter was published, BlackRock, which is a firm that does an enormous amount of money market managing and so stands to win or lose big on money market regulation, published an article in which they trashed Schapiro’s proposals and embellished this third one.

In other words, it looks like Geithner has been talking directly to Blackrock about how the money market regulation should be written.

In fact Geithner has seemingly invited industry insiders to talk to him at the Treasury. And now we have his proposal, which benefits insiders and also seems to have all of the unattractiveness that the other proposals had in terms of risks for normal people, i.e. non-insiders. That’s weird.

Update: in this Bloomberg article from yesterday (hat tip Matt Stoller), it looks like Geithner may be getting a fancy schmancy job at BlackRock after the election. Oh!

What’s wrong with simple?

Personally, and I say this as myself and not representing anyone else, I don’t see what’s wrong with Schapiro’s first proposal to keep the NAV floating. If there’s risk, investors should know about it, period, end of story. I don’t want the taxpayers on the hook for this kind of crap.

Occupy in the Financial Times

Lisa Pollack just wrote about Occupy yesterday in this article entitled “Occupy is Increasingly Well-informed”.

It was mostly about Alternative Banking‘s sister working group in London, Occupy Economics, and their recent event this past Monday at which Andy Haldane, Executive Director of Financial Stability at the Bank of England spoke and at which Lisa Pollack chaired the discussion. For more on that event see Lisa’s article here.

Lisa interviewed me yesterday for the article, and asked me (over the screaming of my three sons who haven’t had school in what feels like months), if I had a genie and one try, what would I wish for with respect to Occupy and Alt Banking. I decided that my wish would be that there’s no reason to meet anymore, that the regulators, politicians, economists, lobbyists and bank CEO’s, so the stewards or our financial system and the economy, all got together and decided to do their jobs (and the lobbyists just found other jobs).

Does that count as one wish?

I’m digging these events where Occupiers get to talk one-on-one with those rare regulators and insiders who know how the system works, understand that the system is rigged, and are courageous enough to be honest about it. Alternative Banking met with Sheila Bar a couple of months ago and we’ve got more very exciting meetings coming up as well.

Are healthcare costs really skyrocketing?

Yesterday we had a one-year anniversary meeting of the Alternative Banking group of Occupy Wall Street. Along with it we had excellent discussions of social security, Medicare, and ISDA, including details descriptions of how ISDA changes the rules to suit themselves and the CDS market, acting as a kind of independent system of law, which in particular means it’s not accountable to other rules of law.

Going back to our discussion on Medicare, I have a few comments and a questions for my dear readers:

I’ve been told by someone who should know that the projected “skyrocketing medical costs” which we hear so much about from politicians are based on a “cost per day in the hospital” number, i.e. as that index goes up, we assume medical costs will go up in tandem.

There’s a very good reason to consider this a biased proxy for medical costs, however. Namely, lots of things that used to be in-patient procedures (think gallbladder operations, which used to require a huge operation and many days of ICU care) are now out-patient procedures, so they don’t require a full day in the hospital.

This is increasingly true for various procedures – what used to take many days in the hospital recovering now takes fewer (or they kick you out sooner anyway). The result is that, on average, you only get to stay a whole day in the hospital if something’s majorly wrong with you, so yes the costs there are much higher. Thus the biased proxy.

A better index of cost would be: the cost of the average person’s medical expenses per year.

First question: Is this indeed how people calculate projected medical costs? It’s surprisingly hard to find a reference. That’s a bad sign. I’d really love a reference.

Next, I have a separate pet theory on why we are so willing to believe whatever we’re told about medical costs.

I’ve been planning for months to write a venty post about medical bills and HMO insurance paper mix-ups (update: wait, I did in fact write this post already). Specifically, it’s my opinion that the system is intentionally complicated so that people will end up paying stuff they shouldn’t just because they can’t figure out who to appeal to.

Note that even the idea of appealing to authority for a medical bill presumes that you’ve had a good education and experience dealing with formality. As a former customer service representative at a financial risk software company, I’m definitely qualified, but I can’t believe that the average person in this country isn’t overwhelmed by the prospect. It’s outrageous.

Part of this fear and anxiety stems from the fact that the numbers on the insurance claims are so inflated – $1200 to be seen for a dislocated finger being put into a splint, things like that. Why does that happen? I’m not sure, but I believe those are fake numbers that nobody actually pays, or at least nobody with insurance.

Second question: Why are the numbers on insurance claims so inflated? Who pays those actual numbers?

On to my theory: by extension of the above byzantine system of insurance claims and inflated prices for everything, we’re essentially primed for the line coming from politicians, who themselves (of course) lean on experts who “have studied this,” that health care costs are skyrocketing and that we can’t possibly allow “entitlements” to continue to grow the way they have been. A couple of comments:

- As was pointed out here (hat tip Deb), the fact that the numbers are already inflated so much, especially in comparison to other countries, should mean that they will tend to go down in the future, not up, as people travel away from our country to pay less. This is of course already happening.

- Even so, psychologically, we are ready for those numbers to say anything at all. $120,000 for a splint? Ok, sounds good, I hope I’m covered.

- Next, it’s certainly true that with technological advances come expensive techniques, especially for end-of-life and neonatal procedures. But on the other hand technology is also making normal, mid-life procedures (gallbladders removal) much cheaper.

- I would love to see a few histograms on this data, based on age of patient or prevalence of problem.

- I’d guess such histograms would show us the following: the overall costs structure is becoming much more fat-tailed, as the uncommon but expensive procedures are being used, but the mean costs could easily be going down, or could be projected to go down once more doctors and hospitals have invested in these technologies. Of course I have no idea if this is true.

Third question: Anyone know where such data can be found so I can draw me some histograms?

Final notes:

- The baby boomers are a large group, and they’re retiring and getting sick. But they’re not 10 times bigger than other generations, and the “exponential growth” we’ve been hearing about doesn’t get explained by this alone.

- Assume for a moment that medical costs are rising but not skyrocketing, which is my guess. Why would people (read: politicians) be so eager to exaggerate this?

Bad news wish list

You know that feeling you get when, a few years after you went to a wedding of your friends, you find out they’re getting a divorce?

It’s not a nice feeling. It’s work for you, and nasty work at that: you have to go back over your memories of those two in the past years, where you’d been projecting happiness and contentment all this time, and replace it with argument and bitterness. Not to mention the sorrow and sympathy you naturally bestow on your friends.

If it happens enough times, which it has to me, then going to weddings at all is kind of a funereal affair. I no longer project happy thoughts towards the newly married couple. If anything I worry for them and cross my fingers, hoping for the best. You may even say I’ve lost my faith in the institution.

Considering this, I can kind of understand why some religions don’t allow divorce. If you don’t allow it, then the bad news will never come out, and you won’t have to retroactively fit your internal model of other people’s lives to reality. You can go on blithely assuming everyone’s doing great. While we’re at it, no kids are getting neglected or abused because we don’t talk about that kind of thing.

By way of unreasonable analogy, I’d like to discuss the lack of conversation we’ve seen by the presidential campaigns on both sides about the state of the financial system. I’m starting to think it’s part of the religion of politicians that they never talk about this stuff, because they treat it as an embarrassing failure along the lines of a catholic divorce.

Or maybe I don’t have to be so philosophical about it- is it religion, or is it just money?

I had trouble following much about the two national conventions, because it made me so incensed that nothing was really being discussed, and that it was all so full of shit. But one thing I managed to glean from the coverage of the “events” being sponsored by the various lobbyist groups at the two conventions is that, whereas most lobbyists sponsor events at one of the conventions, like the NRA sponsors something at the Republican convention and the unions sponsor stuff at the Democratic convention, the financial lobbyists sponsor huge swanky events at both.

I interpret this to mean that they are paying to not be discussed as a platform issue. They seem to have paid enough, because I don’t hear anything from the Romney camp about shit Obama has or hasn’t done, or shit Geithner has or hasn’t done.

In fact, there’s a “Stories I’d like to See” column in Reuters column entitled “Tales of a TARP built to benefit bankers, and waiting for CEOs to pay the price”, and written by Stephen Brill, which discusses this exact issue in the context of Neil Barofsky’s book Bailout, which I blogged about here. From the column:

A presidential campaign that wanted to call out the Obama administration for being too friendly to Wall Street and the banks at the expense of Main Street would be using Bailout as the cheat sheet that keeps on giving. But with the Romney campaign’s attack coming from the opposite direction – that the president and his team have killed the economy by shackling Wall Street – and with Romney on record in favor of allowing the mortgage crisis to “bottom out” with no government intervention, the former Massachusetts governor and his team have no use for Bailout.

The second half of the article is really good, asking very commonsensical question about the recent settlement BofA got from the SEC for blatantly lying to shareholders around the time they acquired Merrill Lynch. Specifically the author notes that the (current) shareholders are left paying the (2008) shareholders, which is dumb, but the asshole Ken Lewis, who actually lied doesn’t seem to be getting into any trouble at all. From the column:

And, as long as we’re talking about harm done to shareholders, why wouldn’t we now see a new, post-settlement shareholders’ suit not against the company but targeted only at Lewis and some of his former colleagues who got Bank of America into this jam in the first place and just caused it to pay out $2.4 billion? (The plaintiffs here could be any current shareholders, because they are the ones who are writing the $2.4 billion check.) Again, did the company indemnify Lewis and other executives against shareholder suits, meaning that if a shareholder now sues Lewis over this $2.4 billion settlement, the shareholder is once again only suing himself?

Can someone please sort this out?

I really like this idea, that we have a list of topics for people to sort out, even though it’s going to be bad news. What other topics should we ask for on our bad news wish list?

Student loans are a regressive tax

I don’t think this approach of looking at student loans is new, but it’s new to me. A friend of mine mentioned this to me over the weekend.

For simplicity, assume everyone goes to college. Next, assume they all go to similar colleges – similar in cost and in quality. We will revisit these assumptions later. Finally, assume that costs of college keep going up the way they’re going and that student loan interest rates stay high.

What this means when you put it all together is that sufficiently rich people, or more likely their parents, will pay a one-time very large fee to attend college, but then they’ll be done with it. The rest of the people will be stuck paying monthly fees that will never go away. Moreover, because the interest rates are pretty high, the total amount non-rich people pay over their lifetime is substantially more than what rich people pay.

This is essentially a regressive tax, whereby poor people pay more than rich people.

Other points:

- The government student loans don’t have interest rates that are extremely high, but there’s a limit of how much you can borrow with that program, which leads many people even now to borrow privately at much higher rates.

- In the case of government-backed student loans this “tax” is essentially going to the government. In the case of private student loans, the private creditors are receiving the tax.

- Since you can’t discharge student debt via bankruptcy, even private student debt, it really is a life-long tax. It’s even true that if you haven’t paid off your student debt by the time you retire, your social security payments get cut.

- What about our assumptions that all schools have the same quality? Not true. Rich people tend to go to better schools. This means the poor are paying a tax for an inferior service. Of course, it’s also true that truly elite schools like Harvard have excellent financial support for their poorer students. This means there’s a two-tier school system if you’re poor: you can go to a normal school and pay tax, or you can excel and get into an elite school and it will be free.

- What about our assumption that all schools have the same cost? Of course not true; we can look for better quality education for a reasonable price.

- What about our assumption that everyone goes to college? Not true, but it’s still true that going to college and finishing sets you up for far better wage earning than if you only have a high school diploma. And although going to college and not finishing may not, nobody think they’re the ones who won’t finish.

Conclusion: Either we have to keep costs down or we have to make college government-subsidized or we have to make student loan interest rates really low or we have to offset this regressive tax with a highly progressive income tax.

High frequency trading: how it happened, what’s wrong with it, and what we should do

High frequency trading (HFT) is in the news. Politicians and regulators are thinking of doing something to slow stuff down. The problem is, it’s really complicated to understand it in depth and to add rules in a nuanced way. Instead we have to do something pretty simple and stupid if we want to do anything.

How it happened

In some ways HFT is the inevitable consequence of market forces – one has an advantage when one makes a good decision more quickly, so there was always going to be some pressure to speed up trading, to get that technological edge on the competition.

But there was something more at work here too. The NYSE exchange used to be a non-profit mutual, co-owned by every broker who worked there. When it transformed to a profit-seeking enterprise, and when other exchanges popped up in competition with it was the beginning of the age of HFT.

All of a sudden, to make an extra buck, it made sense to allow someone to be closer and have better access, for a hefty fee. And there was competition among the various exchanges for that excellent access. Eventually this market for exchange access culminated in the concept of co-location, whereby trading firms were allowed to put their trading algorithms on servers in the same room as the servers that executed the trades. This avoids those pesky speed-of-light issues when sitting across the street from the executing servers.

Not surprisingly, this has allowed the execution of trades to get into the mind-splittingly small timeframe of double-digit microseconds. That’s microseconds, where from wikipedia: “One microsecond is to one second as one second is to 11.54 days.”

What’s wrong with it

Turns out, when things get this fast, sometimes mistakes happen. Sometimes errors occur. I’m writing in the third-person passive voice because we are no longer talking directly about human involvement, or even, typically, a single algorithm, but rather the combination of a sea of algorithms which together can do unexpected things.

People know about the so-called “flash crash” and more recently Knight Capital’s trading debacle where an algorithm at opening bell went crazy with orders. But people on the inside, if you point out these events, might counter that “normal people didn’t lose money” at these events. The weirdness was mostly fixed after the fact, and anyway pension funds, which is where most normal people’s money lives, don’t ever trade in the thin opening bell market.

But there’s another, less well known example from September 30th, 2008, when the House rejected the bailout, shorting stocks were illegal, and the Dow dropped 778 points. The prices as such common big-ticket stocks such as Google plummeted and, in this case, pension funds lost big money. It’s true that some transactions were later nulled, but not all of them.

This happened because the market makers of the time had largely pulled their models out of the market after shorting became illegal – there was no “do this algorithm except make sure you’re never short” button on the algorithm, so once the rule was called, the traders could only turn it all of completely. As a result, the liquidity wasn’t there and the pension funds, thinking they were being smart to do their big trades at close, instead got completely walloped.

Keep this in mind, before you go blaming the politicians on this one because the immediate cause was the short-sighted short-selling ban: the HFT firms regularly pull out of the market in times of stress, or when they’re updating their algorithms, or just whenever they want. In other words, it’s liquidity when you need it least.

Moreover, just because two out of three times were relatively benign for the 99%, we should not conclude that there’s nothing potentially disastrous going on. The flash crash and Knight Capital have had impact, namely they serve as events which erode our trust in the system as a whole. The 2008 episode on top of that proved that yes, we can be the victims of the out-of-control machines fighting against each other.

Quite aside from the instability of the system, and how regular people get screwed by insiders (because after all, that’s not a new story at all, it’s just a new technology for an old story), let’s talk about resources. How much money and resources are being put into the HFT arena and how could those resources otherwise be used?

Putting aside the actual energy consumed by the industry, which is certainly non-trivial, let’s focus for a moment on money. It has been estimated that overall, HFT firms post about $80 billion in profits yearly, and that they make on the order of 10% profit on their technology investments. That would mean that there’s in the order of $800 billion being invested in HFT each year. Even if we highball the return at 25%, we still have more than $300 billion invested in this stuff.

And to what end?

Is that how much it’s really worth the small investor to have decreased bid-ask spreads when they go long Apple because they think the new iPhone will sell? What else could we be doing with $800 billion dollars? A couple of years of this could sell off all of the student debt in this country.

What should be done

Germany has recently announced a half-second minimum for posting an share order. This is eons in current time frames, and would drastically change how trading is done. They also want HFT algorithms to be registered with them. You know, so people can keep tabs on the algorithms and understand what they’re doing and how they might interact with each other.

Um, what? As a former quant, let me just say: this will not work. Not a chance in hell. If I want to obfuscate the actual goals of a model I’ve written, that’s easier than actually explaining it. Moreover, the half-second rule may sound good but it just means it’s a harder system to game, not that it won’t be gameable.

Other ideas have been brought forth as to how to slow down trading, but in the end it’s really hard to do: if you put in delays, there’s always going to be an algorithm employed which decides whose trade actually happens first, and so there will always be some advantage to speed, or to gaming the algorithm. It would be interesting but academically challenging to come up with a simple enough rule that would actually discourage people from engaging in technological warfare.

The only sure-fire way to make people think harder about trading so quickly and so often is a simple tax on transactions, often referred to as a Tobin Tax. This would make people have sufficient amount of faith in their trade to pay the tax on top of the expected value of the trade.

And we can’t just implement such a tax on one market, like they do for equities in London. It has to be on all exhange-traded markets, and moreover all reasonable markets should be exchange-traded.

Oh, and while I’m smoking crack, let me also say that when exchanges are found to have given certain of their customers better access to prices, the punishments for such illegal insider information should be more than $5 million dollars.

{kind=link}