Archive

SEC Roundtable on credit rating agency models today

I’ve discussed the broken business model that is the credit rating agency system in this country on a few occasions. It directly contributed to the opacity and fraud in the MBS market and to the ensuing financial crisis, for example. And in this post and then this one, I suggest that someone should start an open source version of credit rating agencies. Here’s my explanation:

The system of credit ratings undermines the trust of even the most fervently pro-business entrepreneur out there. The models are knowingly games by both sides, and it’s clearly both corrupt and important. It’s also a bipartisan issue: Republicans and Democrats alike should want transparency when it comes to modeling downgrades- at the very least so they can argue against the results in a factual way. There’s no reason I can see why there shouldn’t be broad support for a rule to force the ratings agencies to make their models publicly available. In other words, this isn’t a political game that would score points for one side or the other.

Well, it wasn’t long before Marc Joffe, who had started an open source credit rating agency, contacted me and came to my Occupy group to explain his plan, which I blogged about here. That was almost a year ago.

Today the SEC is going to have something they’re calling a Credit Ratings Roundtable. This is in response to an amendment that Senator Al Franken put on Dodd-Frank which requires the SEC to examine the credit rating industry. From their webpage description of the event:

The roundtable will consist of three panels:

- The first panel will discuss the potential creation of a credit rating assignment system for asset-backed securities.

- The second panel will discuss the effectiveness of the SEC’s current system to encourage unsolicited ratings of asset-backed securities.

- The third panel will discuss other alternatives to the current issuer-pay business model in which the issuer selects and pays the firm it wants to provide credit ratings for its securities.

Marc is going to be one of something like 9 people in the third panel. He wrote this op-ed piece about his goal for the panel, a key excerpt being the following:

Section 939A of the Dodd-Frank Act requires regulatory agencies to replace references to NRSRO ratings in their regulations with alternative standards of credit-worthiness. I suggest that the output of a certified, open source credit model be included in regulations as a standard of credit-worthiness.

Just to be clear: the current problem is that not only is there wide-spread gaming, but there’s also a near monopoly by the “big three” credit rating agencies, and for whatever reason that monopoly status has been incredibly well protected by the SEC. They don’t grant “NRSRO” status to credit rating agencies unless the given agency can produce something like 10 letters from clients who will vouch for them providing credit ratings for at least 3 years. You can see why this is a hard business to break into.

The Roundtable was covered yesterday in the Wall Street Journal as well: Ratings Firms Steer Clear of an Overhaul – an unfortunate title if you are trying to be optimistic about the event today. From the WSJ article:

Mr. Franken’s amendment requires the SEC to create a board that would assign a rating firm to evaluate structured-finance deals or come up with another option to eliminate conflicts.

While lawsuits filed against S&P in February by the U.S. government and more than a dozen states refocused unflattering attention on the bond-rating industry, efforts to upend its reliance on issuers have languished, partly because of a lack of consensus on what to do.

I’m just kind of amazed that, given how dirty and obviously broken this industry is, we can’t do better than this. SEC, please start doing your job. How could allowing an open-source credit rating agency hurt our country? How could it make things worse?

How much math do scientists need to know?

I’m catching up with reading the “big data news” this morning (via Gil Press) and I came across this essay by E. O. Wilson called “Great Scientist ≠ Good at Math”. In it, he argues that most of the successful scientists he knows aren’t good at math, and he doesn’t see why people get discouraged from being scientists just because they suck at math.

Here’s an important excerpt from the essay:

Over the years, I have co-written many papers with mathematicians and statisticians, so I can offer the following principle with confidence. Call it Wilson’s Principle No. 1: It is far easier for scientists to acquire needed collaboration from mathematicians and statisticians than it is for mathematicians and statisticians to find scientists able to make use of their equations.

Given that he’s written many papers with mathematicians and statisticians, then, he is not claiming that math itself is not part of great science, just that he hasn’t been the one that supplied the mathy bits. I think this is really key.

And it resonates with me: I’ve often said that the cool thing about working on a data science team in industry, for example, is that different people bring different skills to the table. I might be an expert on some machine learning algorithms, while someone else will be a domain expert. The problem requires both skill sets, and perhaps no one person has all that knowledge. Teamwork kinda rocks.

Another thing he exposes with Wilson’s Principle No. 1, though, which doesn’t resonate with me, is a general lack of understanding of what mathematicians are actually trying to accomplish with “their equations”.

It is a common enough misconception to think of the quant as a guy with a bunch of tools but no understanding or creativity. I’ve complained about that before on this blog. But when it comes to professional mathematicians, presumably including his co-authors, a prominent scientist such as Wilson should realize that they are doing creative things inside the realm of mathematics simply for the sake of understanding mathematics.

Mathematicians, as a group, are not sitting around wishing someone could “make use of their equations.” For one thing, they often don’t even think about equations. And for another, they often think about abstract structures with no goal whatsoever of connecting it back to, say, how ants live in colonies. And that’s cool and beautiful too, and it’s not a failure of the system. That’s just math.

I’m not saying it wouldn’t be fun for mathematicians to spend more time thinking about applied science. I think it would be fun for them, actually. Moreover, as the next few years and decades unfold, we might very well see a large-scale shrinkage in math departments and basic research money, which could force the issue.

And, to be fair, there are probably some actual examples of mathy-statsy people who are thinking about equations that are supposed to relate to the real world but don’t. Those guys should learn to be better communicators and pair up with colleagues who have great data. In my experience, this is not a typical situation.

One last thing. The danger in ignoring the math yourself, if you’re a scientist, is that you probably aren’t that great at knowing the difference between someone who really knows math and someone who can throw around terminology. You can’t catch charlatans, in other words. And, given that scientists do need real math and statistics to do their research, this can be a huge problem if your work ends up being meaningless because your team got the math wrong.

Global move to austerity based on mistake in Excel

As Rortybomb reported yesterday on the Roosevelt Institute blog (hat tip Adam Obeng), a recent paper written by Thomas Herndon, Michael Ash, and Robert Pollin looked into replicating the results of a economics paper originally written by Carmen Reinhart and Kenneth Rogoff entitled Growth in a Time of Debt.

The original Reinhart and Rogoff paper had concluded that public debt loads greater than 90 percent of GDP consistently reduce GDP growth, a “fact” which has been widely used. However, the more recent paper finds problems. Here’s the abstract:

Herndon, Ash and Pollin replicate Reinhart and Rogoff and find that coding errors, selective exclusion of available data, and unconventional weighting of summary statistics lead to serious errors that inaccurately represent the relationship between public debt and GDP growth among 20 advanced economies in the post-war period. They find that when properly calculated, the average real GDP growth rate for countries carrying a public-debt-to-GDP ratio of over 90 percent is actually 2.2 percent, not -0:1 percent as published in Reinhart and Rogo ff. That is, contrary to RR, average GDP growth at public debt/GDP ratios over 90 percent is not dramatically different than when debt/GDP ratios are lower.

The authors also show how the relationship between public debt and GDP growth varies significantly by time period and country. Overall, the evidence we review contradicts Reinhart and Rogoff ’s claim to have identified an important stylized fact, that public debt loads greater than 90 percent of GDP consistently reduce GDP growth.

A few comments.

1) We should always have the data and code for published results.

The way the authors Herndon, Ash and Pollin managed to replicate the results was that they personally requested the excel spreadsheets from Reinhart and Rogoff. Given how politically useful and important this result has been (see Rortybomb’s explanation of this), it’s kind of a miracle that they released the spreadsheet. Indeed that’s the best part of this story from a scientific viewpoint.

2) The data and code should be open source.

One cool thing is that now you can actually download the data – there’s a link at the bottom of this page. I did this and was happy to have a bunch of csv files and some (open source) R code which presumably recovers the excel spreadsheet mistakes. I also found some .dta files, which seems like Stata proprietary file types, which is annoying, but then I googled and it seems like you can use R to turn .dta files into csv files. It’s still weird that they wrote code in R but saved files in Stata.

3) These mistakes are easy to make and they’re mostly not considered mistakes.

Let’s talk about the “mistakes” the authors found. First, they’re excluding certain time periods for certain countries, specifically right after World War II. Second, they chose certain “non-standard” weightings for the various countries they considered. Finally, they accidentally excluded certain rows from their calculation.

Only that last one is considered a mistake by modelers. The others are modeling choices, and they happen all the time. Indeed it’s impossible not to make such choices. Who’s to say that you have to use standard country weightings? Why? How much data do you actually need to consider? Why?

[Aside: I’m sure there are proprietary trading models running right now in hedge funds that anticipate how other people weight countries in standard ways and betting accordingly. In that sense, using standard weightings might be a stupid thing to do. But in any case validating a weighting scheme is extremely difficult. In the end you’re trying to decide how much various countries matter in a certain light, and the answer is often that your country matters the most to you.]

4) We need to actually consider other modeling possibilities.

It’s not a surprise, to economists anyway, that after you include more post-WWII years of data, which we all know to be high debt and high growth years worldwide, you get a substantively different answer. Excluding these data points is just as much a political decision as a modeling decision.

In the end the only reasonable way to proceed is to describe your choices, and your reasoning, and the result, but also consider other “reasonable” choices and report the results there too. And if you don’t like the answer, or don’t want to do the work, at the very least you need to provide your code and data and let other people check how your result changes with different “reasonable” choices.

Once the community of economists (and other data-centric fields) starts doing this, we will all realize that our so-called “objective results” utterly depend on such modeling decisions, and are about as variable as our own opinions.

5) And this is an easy model.

Think about how many modeling decisions and errors are in more complicated models!

Interview with Chris Wiggins: don’t send me another $^%& shortcut alias!

When I first met Chris Wiggins of Columbia and hackNY back in 2011, he immediately introduced me to about a hundred other people, which made it obvious that his introductions were highly stereotyped. I thought he was some kind of robot, especially when I started getting emails from his phone which all had the same (long) phrases in them, like “I’m away from my keyboard right now, but when I get back to my desk I’ll calendar prune and send you some free times.”

Finally I was like “what the hell, are you sending me whole auto-generated emails”? To which he replied “of course.”

Chris posted the code to his introduction script last week so now I have proof that some of my favorite emails I thought were from him back in 2011 were actually from tcsh.

Feeling cheated, I called him to tell him he has an addiction to shell scripting. Here’s a brief interview, rewritten to make me sound smarter and cooler than I am.

——

CO: Ok, let’s start with these iphone shortcuts. Sometimes the whole email from you reads like a bunch of shortcuts.

CW: Yup, lots of times.

CO: What the hell? Don’t you want to personalize things for me at least a little?

CW: I do! But I also want to catch the subway.

CO: Ugh. How many shortcuts do you have on that thing?

CW: Well.. (pause)..38.

CO: Ok now I’m officially worried about you. What’s the longest one?

CW: Probably this one I wrote for Sandy: If I write “sandy” it unpacks to

“Sorry for delay and brevity in reply. Sandy knocked out my phone, power, water, and internet so I won’t be replying as quickly as usual. Please do not hesitate to email me again if I don’t reply soon.”

CO: You officially have a problem. What’s the shortest one?

CW: Well, when I type “plu” it becomes “+1”

CO: Ok, let me apply the math for you: your shortcut is longer than your longcut.

CW: I know but not if you include switching from letters to numbers on the iphone, which is annoying.

CO: How did you first become addicted to shortcuts?

CW: I got introduced to UNIX in the 80s and, in my frame of reference at the time, the closest I had come to meeting a wizard was the university’s sysadmin. I was constantly breaking things by chomping cpu with undead processes or removing my $HOME or something, and he had to come in and fix things. I learned a lot over his shoulder. In the summer before I started college, my dream was to be a university sysadmin. He had to explain to me patiently that I shouldn’t spend college in a computercave.

CO: Good advice, but now that you’re a grownup you can do that.

CW: Exactly. Anyway, everytime he would fix whatever incredible mess I had made he would sign off with some different flair and walk out, like he was dropping the mic and walking off stage. He never signed out “logout” it was always “die” or “leave” or “ciao” (I didn’t know that word at the time). So of course by the time he got back to his desk one day there was an email from me asking how to do this and he replied:

“RTFM. alias”

CO: That seems like kind of a mean thing to do to you at such a young age.

CW: It’s true. UNIX alias was clearly the gateway drug that led me to writing shell scripts for everything.

CO: How many aliases do you have now?

CW: According to “alias | wc -l “, I have 1137. So far.

CO: So you’ve spent countless hours making aliases to save time.

CW: Yes! And shell scripts!

CO: Ok let’s talk about this script for introducing me to people. As you know I don’t like getting treated like a small cog. I’m kind of a big deal.

CW: Yes, you’ve mentioned that.

CO: So how does it work?

CW: I have separate biography files for everyone, and a file called nfile.asc that has first name, lastname@tag, and email address. Then I can introduce people via

% ii oneil@mathbabe schutt

It strips out the @mathbabe part (so I can keep track of multiple people named oneil) from the actual email, reads in and reformats the biographies, grepping out the commented lines, and writes an email I can pipe to mutt. The whole thing can be done in a few seconds.

CO: Ok that does sound pretty good. How many shell scripts do you have?

CW: Hundreds. A few of them are in my public mise-en-place repository, which I should update more. I’m not sure which of them I really use all the time, but it’s pretty rare I type an actual legal UNIX command at the command line. That said I try never to leave the command line. Students are always teaching me fancypants tricks for their browsers or some new app, but I spend a lot of time at the command line getting and munging data, and for that, sed, awk, and grep are here to stay.

CO: That’s kinda sad and yet… so true. Ok here’s the only question I really wanted to ask though: will you promise me you’ll never send me any more auto-generated emails?

CW: no.

War of the machines, college edition

A couple of people have sent me this recent essay (hat tip Leon Kautsky) written by Elijah Mayfield on the education technology blog e-Literate, described on their About page as “a hobby weblog about educational technology and related topics that is maintained by Michael Feldstein and written by Michael and some of his trusted colleagues in the field of educational technology.”

Mayfield’s essay is entitled “Six Ways the edX Announcement Gets Automated Essay Grading Wrong”. He’s referring to the recent announcement, which was written about in the New York Times last week, about how professors will soon be replaced by computers in grading essays. He claims they got it all wrong and there’s nothing to worry about.

I wrote about this idea too, in this post, and he hasn’t addressed my complaints at all.

First, Mayfield’s points:

- Journalists sensationalize things.

- The machine is identifying things in the essays that are associated with good writing vs. bad writing, much like it might learn to distinguish pictures of ducks from pictures of houses.

- It’s actually not that hard to find the duck and has nothing to do with “creativity” (look for webbed feet).

- If the machine isn’t sure it can spit back the essay to the professor to read (if the professor is still employed).

- The machine doesn’t necessarily reward big vocabulary words, except when it does.

- You’d need thousands of training examples (essays on a given subject) to make this actually work.

- What’s so really wonderful is that a student can get all his or her many drafts graded instantaneously, which no professor would be willing to do.

Here’s where I’ll start, with this excerpt from near the end:

“Can machine learning grade essays?” is a bad question. We know, statistically, that the algorithms we’ve trained work just as well as teachers for churning out a score on a 5-point scale. We know that occasionally it’ll make mistakes; however, more often than not, what the algorithms learn to do are reproduce the already questionable behavior of humans. If we’re relying on machine learning solely to automate the process of grading, to make it faster and cheaper and enable access, then sure. We can do that.

OK, so we know that the machine can grade essays written for human consumption pretty accurately. But it hasn’t had to deal with essays written for machine consumption yet. There’s major room for gaming here, and only a matter of time before there’s a competing algorithm to build a great essay. I even know how to train that algorithm. Email me privately and we can make a deal on profit-sharing.

And considering that students will be able to get their drafts graded as many times as they want, as Mayfield advertised, this will only be easier. If I build an essay that I think should game the machine, by putting in lots of (relevant) long vocabulary words and erudite phrases, then I can always double check by having the system give me a grade. If it doesn’t work, I’ll try again.

And the essays built this way won’t get caught via the fraud detection software that finds plagiarism, because any good essay-builder will only steal smallish phrases.

One final point. The fact that the machine-learning grading algorithm only works when it’s been trained on thousands of essays points to yet another depressing trend: large-scale classes with the same exact assignments every semester so last year’s algorithm can be used, in the name of efficiency.

But that means last year’s essay-building algorithm can be used as well. Pretty soon it will just be a war of the machines.

Hey WSJ, don’t blame unemployed disabled people for the crap economy

This morning I’m being driven crazy by this article in yesterday’s Wall Street Journal entitled “Workers Stuck in Disability Stunt Economic Recovery.”

Even the title makes the underlying goal of the article crystal clear: the lazy disabled workers are to blame for the crap economy. Lest you are unconvinced that anyone could make such an unreasonable claim of causation, here’s a tasty excerpt from the article that spells it out:

Economic growth is driven by the number of workers in an economy and by their productivity. Put simply, fewer workers usually means less growth.

Since the recession, more people have gone on disability, on net, than new workers have joined the labor force. Mr. Feroli estimated the exodus to disability costs 0.6% of national output, equal to about $95 billion a year.

“The greater cost is their long-term dependency on transfers from the federal government,” Mr. Autor said, “placing strain on the soon-to-be exhausted Social Security Disability trust fund.”

The underlying model here, then, is that there’s a bunch of people who have the choice between going on disability or “joining the labor force” and they’ve all chosen to go on disability. I wonder where their evidence is that people really have that choice, considering the unemployment numbers and participation rate numbers we see nowadays.

For example, the unemployment rate for youths is now 22.9%, and the participation rate for them has gone from 59.2% in December 2007, to 54.5% today. This is probably not because so many kids under the age of 25 are disabled, I suspect. If you look at the overall labor participation rate, it’s dropped from 66.0 in December 2007 to 63.3 in March 2013. Most of the people who have left the work force are also not disabled. They’ve been discouraged for some other mysterious reason. I’m gonna go ahead and guess it’s because they can’t find a job.

This leads me to ask the following question from the journalists LESLIE SCISM and JON HILSENRATH who wrote the article: Where is your evidence of causation??

Here’s another example from the article of a seriously fucked-up understanding of cause and effect:

With overall participation down, the labor force—a measure of people working and people looking for work—is barely growing.

They consistently paint the picture whereby people decide to stop working, and then yucky things happen, in this case the labor force stops growing. Damn those lazy people.

They even bring in a fancy word from physics to describe the problem, namely hysteresis. Now, they didn’t understand or correctly define the term, but it doesn’t really matter, because the point of using a fancy term from physics was not to add to the clarity of the argument but rather to impress.

The goal here is, in fact, that if enough economists use sophisticated language to describe the various effects, we will all be able to blame people with bad backs, making $13.6K per year, on why our economy sucks, rather than the rich assholes in finance who got us into this mess and are currently buying $2 million dollar personal offices instead of going to jail.

Just to be clear, that’s $1,130 a month, which I guess represents so enticing a lifestyle that the people currently enjoying it ‘are “pretty unlikely to want to forfeit economic security for a precarious job market”‘ according to M.I.T. economist David Autor. I’d love to have David Autor spell out, for us, exactly what’s economically secure about that kind of monthly check.

The rest of the article is in large part a description of how people get onto SSDI, insinuating that the people currently on it are not really all that disabled or worthy of living high on the hog, and are in any case never ever leaving.

How’s this for a slightly different take on the situation: there are of course some people who are faking something, that’s always the case. But in general, the people on SSDI need to be there, and before the recession might have had the kind of employers who kept them on even though they often called in sick, out of loyalty and kindness, because they didn’t want to fire them. But when the recession struck those employers had to cut them off, or they went out of business completely. Now those people can’t find work and don’t have many options. In other words, the recession caused the SSDI program to grow. That doesn’t mean it caused a bunch of people to get sick, but it does mean that sick people are more dependent on SSDI because there are fewer options.

By the way, read the comments of this article, there are some really good ones (“What were people with injuries and no high-value job skills to do? Is the number of people in the social security disability program the problem or the symptom?”) as well as some really outrageous ones (‘The current situation makes the picture of the “Welfare Queen” of the 1980s look like an honest citizen’).

We don’t need more complicated models, we need to stop lying with our models

The financial crisis has given rise to a series of catastrophes related to mathematical modeling.

Time after time you hear people speaking in baffled terms about mathematical models that somehow didn’t warn us in time, that were too complicated to understand, and so on. If you have somehow missed such public displays of throwing the model (and quants) under the bus, stay tuned below for examples.

A common response to these problems is to call for those models to be revamped, to add features that will cover previously unforeseen issues, and generally speaking, to make them more complex.

For a person like myself, who gets paid to “fix the model,” it’s tempting to do just that, to assume the role of the hero who is going to set everything right with a few brilliant ideas and some excellent training data.

Unfortunately, reality is staring me in the face, and it’s telling me that we don’t need more complicated models.

If I go to the trouble of fixing up a model, say by adding counterparty risk considerations, then I’m implicitly assuming the problem with the existing models is that they’re being used honestly but aren’t mathematically up to the task.

But this is far from the case – most of the really enormous failures of models are explained by people lying. Before I give three examples of “big models failing because someone is lying” phenomenon, let me add one more important thing.

Namely, if we replace okay models with more complicated models, as many people are suggesting we do, without first addressing the lying problem, it will only allow people to lie even more. This is because the complexity of a model itself is an obstacle to understanding its results, and more complex models allow more manipulation.

Example 1: Municipal Debt Models

Many municipalities are in shit tons of problems with their muni debt. This is in part because of the big banks taking advantage of them, but it’s also in part because they often lie with models.

Specifically, they know what their obligations for pensions and school systems will be in the next few years, and in order to pay for all that, they use a model which estimates how well their savings will pay off in the market, or however they’ve invested their money. But they use vastly over-exaggerated numbers in these models, because that way they can minimize the amount of money to put into the pool each year. The result is that pension pools are being systematically and vastly under-funded.

Example 2: Wealth Management

I used to work at Riskmetrics, where I saw first-hand how people lie with risk models. But that’s not the only thing I worked on. I also helped out building an analytical wealth management product. This software was sold to banks, and was used by professional “wealth managers” to help people (usually rich people, but not mega-rich people) plan for retirement.

We had a bunch of bells and whistles in the software to impress the clients – Monte Carlo simulations, fancy optimization tools, and more. But in the end, the banks and their wealth managers put in their own market assumptions when they used it. Specifically, they put in the forecast market growth for stocks, bonds, alternative investing, etc., as well as the assumed volatility of those categories and indeed the entire covariance matrix representing how correlated the market constituents are to each other.

The result is this: no matter how honest I would try to be with my modeling, I had no way of preventing the model from being misused and misleading to the clients. And it was indeed misused: wealth managers put in absolutely ridiculous assumptions of fantastic returns with vanishingly small risk.

Example 3: JP Morgan’s Whale Trade

I saved the best for last. JP Morgan’s actions around their $6.2 billion trading loss, the so-called “Whale Loss” was investigated recently by a Senate Subcommittee. This is an excerpt (page 14) from the resulting report, which is well worth reading in full:

While the bank claimed that the whale trade losses were due, in part, to a failure to have the right risk limits in place, the Subcommittee investigation showed that the five risk limits already in effect were all breached for sustained periods of time during the first quarter of 2012. Bank managers knew about the breaches, but allowed them to continue, lifted the limits, or altered the risk measures after being told that the risk results were “too conservative,” not “sensible,” or “garbage.” Previously undisclosed evidence also showed that CIO personnel deliberately tried to lower the CIO’s risk results and, as a result, lower its capital requirements, not by reducing its risky assets, but by manipulating the mathematical models used to calculate its VaR, CRM, and RWA results. Equally disturbing is evidence that the OCC was regularly informed of the risk limit breaches and was notified in advance of the CIO VaR model change projected to drop the CIO’s VaR results by 44%, yet raised no concerns at the time.

I don’t think there could be a better argument explaining why new risk limits and better VaR models won’t help JPM or any other large bank. The manipulation of existing models is what’s really going on.

Just to be clear on the models and modelers as scapegoats, even in the face of the above report, please take a look at minute 1:35:00 of the C-SPAN coverage of former CIO head Ina Drew’s testimony when she’s being grilled by Senator Carl Levin (hat tip Alan Lawhon, who also wrote about this issue here).

Ina Drew firmly shoves the quants under the bus, pretending to be surprised by the failures of the models even though, considering she’d been at JP Morgan for 30 years, she might know just a thing or two about how VaR can be manipulated. Why hasn’t Sarbanes-Oxley been used to put that woman in jail? She’s not even at JP Morgan anymore.

Stick around for a few minutes in the testimony after Levin’s done with Drew, because he’s on a roll and it’s awesome to watch.

Guest Post SuperReview Part III of VI: The Occupy Handbook Part I and a little Part II: Where We Are Now

Whattup.

Moving on from Lewis’ cute Bloomberg column reprint, we come to the next essay in the series:

The Widening Gyre: Inequality, Polarization, and the Crisis by Paul Krugman and Robin Wells

Indefatigable pair Paul Krugman and Robin Wells (KW hereafter) contribute one of the several original essays in the book, but the content ought to be familiar if you read the New York Times, know something about economics or practice finance. Paul Krugman is prolific, and it isn’t hard to be prolific when you have to rewrite essentially the same column every week; question, are there other columnists who have been so consistently right yet have failed to propose anything that the polity would adopt? Political failure notwithstanding, Krugman leaves gems in every paragraph for the reader new to all this. The title “The Widening Gyre” comes from an apocalyptic William Yeats Butler poem. In this case, Krugman and Wells tackle the problem of why the government responded so poorly to the crisis. In their words:

By 2007, America was about as unequal as it had been on the eve of the Great Depression – and sure enough, just after hitting this milestone, we lunged into the worst slump since the Depression. This probably wasn’t a coincidence, although economists are still working on trying to understand the linkages between inequality and vulnerability to economic crisis.

Here, however, we want to focus on a different question: why has the response to crisis been so inadequate? Before financial crisis struck, we think it’s fair to say that most economists imagined that even if such a crisis were to happen, there would be a quick and effective policy response [editor’s note: see Kautsky et al 2016 for a partial explanation]. In 2003 Robert Lucas, the Nobel laureate and then president of the American Economic Association, urged the profession to turn its attention away from recessions to issues of longer-term growth. Why? Because he declared, the “central problem of depression-prevention has been solved, for all practical purposes, and has in fact been solved for many decades.”

Famous last words from Professor Lucas. Nevertheless, the curious failure to apply what was once the conventional wisdom on a useful scale intrigues me for two reasons. First, most political scientists suggest that democracy, versus authoritarian system X, leads to better outcomes for two reasons.

1. Distributional – you get a nicer distribution of wealth (possibly more productivity for complicated macro reasons); economics suggests that since people are mostly envious and poor people have rapidly increasing utility in wealth, democracy’s tendency to share the wealth better maximizes some stupid social welfare criterion (typically, Kaldor-Hicks efficiency).

2. Information – democracy is a better information aggregation system than dictatorship and an expanded polity makes better decisions beyond allocation of produced resources. The polity must be capable of learning and intelligent OR vote randomly if uninformed for this to work. While this is the original rigorous justification for democracy (first formalized in the 1800s by French rationalists), almost no one who studies these issues today believes one-person one-vote democracy better aggregates information than all other systems at a national level. “Well Leon,” some knave comments, “we don’t live in a democracy, we live in a Republic with a president…so shouldn’t a small group of representatives better be able to make social-welfare maximizing decisions?” Short answer: strong no, and US Constitutionalism has some particularly nasty features when it comes to political decision-making.

Second, KW suggest that the presence of extreme wealth inequalities act like a democracy disabling virus at the national level. According to KW extreme wealth inequalities perpetuate themselves in a way that undermines both “nice” features of a democracy when it comes to making regulatory and budget decisions.* Thus, to get better economic decision-making from our elected officials, a good intermediate step would be to make our tax system more progressive or expand Medicare or Social Security or…Well, we have a lot of good options here. Of course, for mathematically minded thinkers, this begs the following question: if we could enact so-called progressive economic policies to cure our political crisis, why haven’t we done so already? What can/must change for us to do so in the future? While I believe that the answer to this question is provided by another essay in the book, let’s take a closer look at KW’s explanation at how wealth inequality throws sand into the gears of our polity. They propose four and the following number scheme is mine:

1. The most likely explanation of the relationship between inequality and polarization is that the increased income and wealth of a small minority has, in effect bought the allegiance of a major political party…Needless to say, this is not an environment conducive to political action.

2. It seems likely that this persistence [of financial deregulation] despite repeated disasters had a lot do with rising inequality, with the causation running in both directions. On the one side the explosive growth of the financial sector was a major source of soaring incomes at the very top of the income distribution. On the other side, the fact that the very rich were the prime beneficiaries of deregulation meant that as this group gained power- simply because of its rising wealth- the push for deregulation intensified. These impacts of inequality on ideology did not in 2008…[they] left us incapacitated in the face of crisis.

3. Conservatives have always seen seen [Keynesian economics] as the thin edge of the wedge: concede that the government can play a useful role in fighting slumps, and the next thing you know we’ll be living under socialism.

4. [Krugman paraphrasing Kalecki] Every widening of state activity is looked upon by business with suspicion, but the creation of employment by government spending has a special aspect which makes the opposition particularly intense. Under a laissez-faire system the level of employment to a great extend on the so-called state of confidence….This gives capitalists a powerful indirect control over government policy: everything which may shake the state of confidence must be avoided because it would cause an economic crisis.

All of these are true to an extent. Two are related to the features of a particular policy position that conservatives don’t like (countercyclical spending) and their cost will dissipate if the economy improves. Isn’t it the case that most proponents and beneficiaries of financial liberalization are Democrats? (Wall Street mostly supported Obama in 08 and barely supported Romney in 12 despite Romney giving the house away). In any case, while KW aren’t big on solutions they certainly have a strong grasp of the problem.

Take a Stand: Sit In by Phillip Dray

As the railroad strike of 1877 had led eventually to expanded workers’ rights, so the Greensboro sit-in of February 1, 1960, helped pave the way for passage of the Civil Rights Act of 1964 and the Voting Rights Act of 1965. Both movements remind us that not all successful protests are explicit in their message and purpose; they rely instead on the participants’ intuitive sense of justice. [28]

I’m not the only author to have taken note of this passage as particularly important, but I am the only author who found the passage significant and did not start ranting about so-called “natural law.” Chronicling the (hitherto unknown-to-me) history of the Great Upheaval, Dray does a great job relating some important moments in left protest history to the OWS history. This is actually an extremely important essay and I haven’t given it the time it deserves. If you read three essays in this book, include this in your list.

Inequality and Intemperate Policy by Raghuram Rajan (no URL, you’ll have to buy the book)

Rajan’s basic ideas are the following: inequality has gotten out of control:

Deepening income inequality has been brought to the forefront of discussion in the United States. The discussion tends to center on the Croesus-like income of John Paulson, the hedge fund manager who made a killing in 2008 betting on a financial collapse and netted over $3 billion, about seventy-five-thousand times the average household income. Yet a more worrying, everyday phenomenon that confronts most Americans is the disparity in income growth rates between a manager at the local supermarket and the factory worker or office assistant. Since the 1970s, the wages of the former, typically workers at the ninetieth percentile of the wage distribution in the United States, have grown much faster than the wages of the latter, the typical median worker.

But American political ideologies typically rule out the most direct responses to inequality (i.e. redistribution). The result is a series of stop-gap measures that do long-run damage to the economy (as defined by sustainable and rising income levels and full employment), but temporarily boost the consumption level of lower classes:

It is not surprising then, that a policy response to rising inequality in the United States in the 1990s and 200s – whether carefully planned or chosen as the path of least resistance – was to encourage lending to households, especially but not exclusively low-income ones, with the government push given to housing credit just the most egregious example. The benefit – higher consumption – was immediate, whereas paying the inevitable bill could be postponed into the future. Indeed, consumption inequality did not grow nearly as much as income inequality before the crisis. The difference was bridged by debt. Cynical as it may seem, easy credit has been used as a palliative success administrations that been unable to address the deeper anxieties of the middle class directly. As I argue in my book Fault Lines, “Let them eat credit” could well summarize the mantra of the political establishment in the go-go years before the crisis.

Why should you believe Raghuram Rajan? Because he’s one of the few guys who called the first crisis and tried to warn the Fed.

A solid essay providing a more direct link between income inequality and bad policy than KW do.

The 5 Percent by Michael Hiltzik

The 5 percent’s [consisting of the seven million Americans who, in 1934, were sixty-five and older] protests coalesced as the Townsend movement, launched by a sinewy midwestern farmer’s son and farm laborer turned California physician. Francis Townsend was a World War I veteran who had served in the Army Medical Corps. He had an ambitious, and impractical plan for a federal pension program. Although during its heyday in the 1930s the movement failed to win enactment of its [editor’s note: insane] program, it did play a critical role in contemporary politics. Before Townsend, America understood the destitution of its older generations only in abstract terms; Townsend’s movement made it tangible. “It is no small achievment to have opened the eyes of even a few million Americans to these facts,” Bruce Bliven, editor of the New Republic observed. “If the Townsend Plan were to die tomorrow and be completely forgotten as miniature golf, mah-jongg, or flinch [editor’s note: everything old is new again], it would still have left some sedimented flood marks on the national consciousness.” Indeed, the Townsend movement became the catalyst for the New Deal’s signal achievement, the old-age program of Social Security. The history of its rise offers a lesson for the Occupy movement in how to convert grassroots enthusiasm into a potent political force – and a warning about the limitations of even a nationwide movement.

Does the author live up to the promises of this paragraph? Is the whole essay worth reading? Does FDR give in to the people’s demands and pass Social Security?!

Yes to all. Read it.

Hidden in Plain Sight by Gillian Tett (no URL, you’ll have to buy the book)

This is a great essay. I’m going to outsource the review and analysis to:

http://beyoubesure.com/2012/10/13/generation-lost-lazy-afraid/

because it basically sums up my thoughts. You all, go read it.

What Good is Wall Street? by John Cassidy

If you know nothing about Wall Street, then the essay is worth reading, otherwise skip it. There are two common ways to write a bad article in financial journalism. First, you can try to explain tiny index price movements via news articles from that day/week/month. “Shares in the S&P moved up on good news in Taiwan today,” that kind of nonsense. While the news and price movements might be worth knowing for their own sake, these articles are usually worthless because no journalist really knows who traded and why (theorists might point out even if the journalists did know who traded to generate the movement and why, it’s not clear these articles would add value – theorists are correct).

The other way, the Cassidy! way is to ask some subgroup of American finance what they think about other subgroups in finance. High frequency traders think iBankers are dumb and overpaid, but HFT on the other hand, provides an extremely valuable service – keeping ETFs cheap, providing liquidity and keeping shares the right level. iBankers think prop-traders add no value, but that without iBanking M&A services, American manufacturing/farmers/whatever would cease functioning. Low speed prop-traders think that HFT just extracts cash from dumb money, but prop-traders are reddest blooded American capitalists, taking the right risks and bringing knowledge into the markets. Insurance hates hedge funds, hedge funds hate the bulge bracket, the bulge bracket hates the ratings agencies, who hate insurance and on and on.

You can spit out dozens of articles about these catty and tedious rivalries (invariably claiming that financial sector X, rivals for institutional cash with Y, “adds no value”) and learn nothing about finance. Cassidy writes the article taking the iBankers side and surprises no one (this was originally published as an article in The New Yorker).

Your House as an ATM by Bethany McLean

Ms. McLean holds immense talent. It was always pretty obvious that the bottom twenty-percent, i.e. the vast majority of subprime loan recipients, who are generally poor at planning, were using mortgages to get quick cash rather than buy houses. Regulators and high finance, after resisting for a good twenty years, gave in for reasons explained in Rajan’s essay.

Against Political Capture by Daron Acemoglu and James A. Robinson (sorry I couldn’t find a URL, for this original essay you’ll have to buy the book).

A legit essay by a future Nobelist in Econ. Read it.

A Nation of Business Junkies by Arjun Appadurai

Anthro-hack Appadurai writes:

I first came to this country in 1967. I have been either a crypto-anthropologist or professional anthropologist for most of the intervening years. Still, because I came here with an interest in India and took the path of least resistance in choosing to retain India as my principal ethnographic referent, I have always been reluctant to offer opinions about life in these United States.

His instincts were correct. The essay reads like an old man complaining about how bad the weather is these days. Skip it.

Causes of Financial Crises Past and Present: The Role of This-Time-Is-Different Syndrome by Carmen M. Reinhart and Kenneth S. Rogoff

Editor Byrne has amazing powers of persuasion or, a lot of authors have had some essays in the desk-drawer they were waiting for an opportunity to publish. In any case, Rogoff and Reinhart (RR hereafter) have summed up a couple hundred studies and two of their books in a single executive summary and given it to whoever buys The Occupy Handbook. Value. RR are Republicans and the essay appears to be written in good faith (unlike some people *cough* Tyler Cowen and Veronique de Rugy *cough*). RR do a great job discovering and presenting stylized facts about financial crises past and present. What to expect next? A couple national defaults and maybe a hyperinflation or two.

Government As Tough Love by Robert Shiller as interviewed by Brandon Adams (buy the book)!

Shiller has always been ahead of the curve. In 1981, he wrote a cornerstone paper in behavioral finance at a time when the field was in its embryonic stages. In the early 1990s, he noticed insufficient attention was paid to real estate values, despite their overwhelming importance to personal wealth levels; this led him to create, along with Karl E. Case, the Case-Shiller index – now the Case-Shiller Home Prices Indices. In March 2000**, Shiller published Irrational Exuberance, arguing that U.S. stocks were substantially overvalued and due for a tumble. [Editor’s note: what Brandon Adams fails to mention, but what’s surely relevant is that Shiller also called the subprime bubble and re-released Irrational Exuberance in 2005 to sound the alarms a full three years before The Subprime Solution]. In 2008, he published The Subprime Solution, which detailed the origins of the housing crisis and suggested innovative policy responses for dealing with the fallout. These days, one of his primary interests is neuroeconomics, a field that relates economic decision-making to brain function as measured by fMRIs.

Shiller is basically a champ and you should listen to him.

Shiller was disappointed but not surprised when governments bailed out banks in extreme fashion while leaving the contracts between banks and homeowners unchanged. He said, of Hank Paulson, “As Treasury secretary, he presented himself in a very sober and collected way…he did some bailouts that benefited Goldman Sachs, among others. And I can imagine that they were well-meaning, but I don’t know that they were totally well-meaning, because the sense of self-interest is hard to clean out of your mind.”

Shiller understates everything.

Verdict: Read it.

And so, we close our discussion of part I. Moving on to part II:

In Ms. Byrne’s own words:

Part 2, “Where We Are Now,” which covers the present, both in the United States and abroad, opens with a piece by the anthropologist David Graeber. The world of Madison Avenue is far from the beliefs of Graeber, an anarchist, but it’s Graeber who arguably (he says he didn’t do it alone) came up with the phrase “We Are the 99 percent.” As Bloomberg Businessweek pointed out in October 2011, during month two of the Occupy encampments that Graeber helped initiate and three moths after the publication of his Debt: The First 5,000 Years, “David Graeber likes to say that he had three goals for the year: promote his book, learn to drive, and launch a worldwide revolution. The first is going well, the second has proven challenging and the third is looking up.” Graeber’s counterpart in Chile can loosely be said to be Camila Vallejo, the college undergraduate, pictured on page 219, who, at twenty-three, brought the country to a standstill. The novelist and playwright Ariel Dorfman writes about her and about his own self-imposed exile from Chile, and his piece is followed by an entirely different, more quantitative treatment of the subject. This part of the book also covers the indignados in Spain, who before Occupy began, “occupied” the public squares of Madrid and other cities – using, as the basis for their claim on the parks could be legally be slept in, a thirteenth-century right granted to shepherds who moved, and still move, their flocks annually.

In other words, we’re in occupy is the hero we deserve, but not the hero we need territory here.

*Addendum 1: Some have suggested that it’s not the wealth inequality that ought to be reduced, but the democratic elements of our system. California’s terrible decision–making resulting from its experiments with direct democracy notwithstanding, I would like to stay in the realm of the sane.

**Addendum 2: Yes, Shiller managed to get the book published the week before the crash. Talk about market timing.

Guest Post SuperReview Part II of VI: The Occupy Handbook Part I: How We Got Here

Whatsup.

This is a review of Part I of The Occupy Handbook. Part I consists of twelve pieces ranging in quality from excellent to awful. But enough from me, in Janet Byrne’s own words:

Part 1, “How We Got Here,” takes a look at events that may be considered precursors of OWS: the stories of a brakeman in 1877 who went up against the railroads; of the four men from an all-black college in North Carolina who staged the first lunch counter sit-in of the 1960s; of the out-of-work doctor whose nationwide, bizarrely personal Townsend Club movement led to the passage of Social Security. We go back to the 1930s and the New Deal and, in Carmen M. Reinhart and Kenneth S. Rogoff‘s “nutshell” version of their book This Time Is Different: Eight Centuries of Financial Folly, even further.

Ms. Byrne did a bang-up job getting one Nobel Prize Winner in economics (Paul Krugman), two future Economics Nobel Prize winners (Robert Shiller, Daron Acemoglu) and two maybes (sorry Raghuram Rajan and Kenneth Rogoff) to contribute excellent essays to this section alone. Powerhouse financial journalists Gillian Tett, Michael Hilztik, John Cassidy, Bethany McLean and the prolific Michael Lewis all drop important and poignant pieces into this section. Arrogant yet angry anthropologist Arjun Appadurai writes one of the worst essays I’ve ever had the misfortune of reading and the ubiquitous Brandon Adams make his first of many mediocre appearances interviewing Robert Shiller. Clocking in at 135 pages, this is the shortest section of the book yet varies the most in quality. You can skip Professor Appadurai and Cassidy’s essays, but the rest are worth reading.

Advice from the 1 Percent: Lever Up, Drop Out by Michael Lewis

Framed as a strategy memo circulated among one-percenters, Lewis’ satirical piece written after the clearing of Zucotti Park begins with a bang.

The rabble has been driven from the public parks. Our adversaries, now defined by the freaks and criminals among them, have demonstrated only that they have no idea what they are doing. They have failed to identify a single achievable goal.

Indeed, the absurd fixation on holding Zuccotti Park and refusal to issue demands because doing so “would validate the system” crippled Occupy Wall Street (OWS). So far OWS has had a single, but massive success: it shifted the conversation back to the United States’ out of control wealth inequality managed to do so in time for the election, sealing the deal on Romney. In this manner, OWS functioned as a holding action by the 99% in the interests of the 99%.

We have identified two looming threats: the first is the shifting relationship between ambitious young people and money. There’s a reason the Lower 99 currently lack leadership: anyone with the ability to organize large numbers of unsuccessful people has been diverted into Wall Street jobs, mainly in the analyst programs at Morgan Stanley and Goldman Sachs. Those jobs no longer exist, at least not in the quantities sufficient to distract an entire generation from examining the meaning of their lives. Our Wall Street friends, wounded and weakened, can no longer pick up the tab for sucking the idealism out of America’s youth.We on the committee are resigned to all elite universities becoming breeding grounds for insurrection, with the possible exception of Princeton.

Michael Lewis speaks from experience; he is a Princeton alum and a 1 percenter himself. More than that however, he is also a Wall Street alum from Salomon Brothers during the 1980s snafu and wrote about it in the original guide to Wall Street, Liar’s Poker. Perhaps because of his atypicality (and dash of solipsism), he does not have a strong handle on human(s) nature(s). By the time of his next column in Bloomberg, protests had broken out at Princeton.

Ultimately ineffectual, but still better than…

Lewis was right in the end, but more than anyone sympathetic to the movement might like. OccupyPrinceton now consists of only two bloggers, one of which has graduated and deleted all his work from an already quiet site and another who is a senior this year. OccupyHarvard contains a single poorly written essay on the front page. Although OccupyNewHaven outlasted the original Occupation, Occupy Yale no longer exists. Occupy Dartmouth hasn’t been active for over a year, although it has a rather pathetic Twitter feed here. Occupy Cornell, Brown, Caltech, MIT and Columbia don’t exist, but some have active facebook pages. Occupy Michigan State, Rutgers and NYU appear to have had active branches as recently as eight months ago, but have gone silent since. Functionally, Occupy Berkeley and its equivalents at UCBerkeley predate the Occupy movement and continue but Occupy Stanford hasn’t been active for over a year. Anecdotally, I recall my friends expressing some skepticism that any cells of the Occupy movement still existed.

As for Lewis’ other points, I’m extremely skeptical about “examined lives” being undermined by Wall Street. As someone who started in math and slowly worked his way into finance, I can safely say that I’ve been excited by many of the computing, economic, and theoretical problems quants face in their day-to-day work and I’m typical. I, and everyone who has lived long-enough, knows a handful of geniuses who have thought long and hard about the kinds of lives they want to lead and realized that A. there is no point to life unless you make one and B. making money is as good a point as any. I know one individual, after working as a professional chemist prior to college,who decided to in his words, “fuck it and be an iBanker.” He’s an associate at DB. At elite schools, my friend’s decision is the rule rather than the exception, roughly half of Harvard will take jobs in finance and consulting (for finance) this year. Another friend, an exception, quit a promising career in operations research to travel the world as a pick-up artist. Could one really say that either the operations researcher or the chemist failed to examine their lives or that with further examinations they would have come up with something more “meaningful”?

One of the social hacks to give lie to Lewis-style idealism-emerging-from-an attempt-to-examine-ones-life is to ask freshpeople at Ivy League schools what they’d like to do when they graduate and observe their choices four years later. The optimal solution for a sociopath just admitted to a top school might be to claim they’d like to do something in the peace corp, science or volunteering for the social status. Then go on to work in academia, finance, law or tech or marriage and household formation with someone who works in the former. This path is functionally similar to what many “average” elite college students will do, sociopathic or not. Lewis appears to be sincere in his misunderstanding of human(s) nature(s). In another book he reveals that he was surprised at the reaction to Liar’s Poker – most students who had read the book “treated it as a how-to manual” and cynically asked him for tips on how to land analyst jobs in the bulge bracket. It’s true that there might be some things money can’t buy, but an immensely pleasurable, meaningful life do not seem to be one of them. Today for the vast majority of humans in the Western world, expectations of sufficient levels of cold hard cash are necessary conditions for happiness.

In short and contra Lewis, little has changed. As of this moment, Occupy has proven so harmless to existing institutions that during her opening address Princeton University’s president Shirley Tilghman called on the freshmen in the class of 2016 to “Occupy” Princeton. No freshpeople have taken up her injunction. (Most?) parts of Occupy’s failure to make a lasting impact on college campuses appear to be structural; Occupy might not have succeeded even with better strategy. As the Ivy League became more and more meritocratic and better at discovering talent, many of the brilliant minds that would have fallen into the 99% and become its most effective advocates have been extracted and reached their so-called career potential, typically defined by income or status level. More meritocratic systems undermine instability by making the most talented individuals part of the class-to-be-overthrown, rather than the over throwers of that system. In an even somewhat meritocratic system, minor injustices can be tolerated: Asians and poor rural whites are classes where there is obvious evidence of discrimination relative to “merit and the decision to apply” in elite gatekeeper college admissions (and thus, life outcomes generally) and neither group expresses revolutionary sentiment on a system-threatening scale, even as the latter group’s life expectancy has begun to decline from its already low levels. In the contemporary United States it appears that even as people’s expectations of material security evaporate, the mere possibility of wealth bolsters and helps to secure inequities in existing institutions.

Lewis continues:

Hence our committee’s conclusion: we must be able to quit American society altogether, and they must know it.The modern Greeks offer the example in the world today that is, the committee has determined, best in class. Ordinary Greeks seldom harass their rich, for the simple reason that they have no idea where to find them. To a member of the Greek Lower 99 a Greek Upper One is as good as invisible.

He pays no taxes, lives no place and bears no relationship to his fellow citizens. As the public expects nothing of him, he always meets, and sometimes even exceeds, their expectations. As a result, the chief concern of the ordinary Greek about the rich Greek is that he will cease to pay the occasional visit.

Michael Lewis is a wise man.

I can recall a conversation with one of my Professors; an expert on Democratic Kampuchea (American: Khmer Rouge), she explained that for a long time the identity of the oligarchy ruling the country was kept secret from its citizens. She identified this obvious subversion of republican principles (how can you have control over your future when you don’t even know who runs your region?) as a weakness of the regime. Au contraire, I suggested, once you realize your masters are not gods, but merely humans with human characteristics, that they: eat, sleep, think, dream, have sex, recreate, poop and die – all their mystique, their claims to superior knowledge divine or earthly are instantly undermined. De facto segregation has made upper classes in the nation more secure by allowing them to hide their day-to-day opulence from people who have lost their homes, job and medical care because of that opulence. Neuroscience will eventually reveal that being mysterious makes you appear more sexy, socially dominant, and powerful, thus making your claims to power and dominance more secure (Kautsky et. al. 2018).*

If the majority of Americans manage to recognize that our two tiered legal system has created a class whose actual claim to the US immense wealth stems from, for the most part, a toxic combination of Congressional pork, regulatory and enforcement agency capture and inheritance rather than merit, there will be hell to pay. Meanwhile, resentment continues to grow. Even on the extreme right one can now regularly read things like:

Now, I think I’d be downright happy to vote for the first politician to run on a policy of sending killer drones after every single banker who has received a post-2007 bonus from a bank that received bailout money. And I’m a freaking libertarian; imagine how those who support bombing Iraqi children because they hate us for our freedoms are going to react once they finally begin to grasp how badly they’ve been screwed over by the bankers. The irony is that a banker-assassination policy would be entirely constitutional according to the current administration; it is very easy to prove that the bankers are much more serious enemies of the state than al Qaeda. They’ve certainly done considerably more damage.

Wise financiers know when it’s time to cash in their chips and disappear. Rarely, they can even pull it off with class.

The rest of part I reviewed tomorrow. Hang in there people.

Addendum 1: If your comment amounts to something like “the Nobel Prize in Economics is actually called the The Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel” and thus “not a real Nobel Prize” you are correct, yet I will still delete your comment and ban your IP.

*Addendum 2: More on this will come when we talk about the Saez-Delong discussion in part III.

Guest Post SuperReview Part I of VI: The Occupy Handbook

Whassup.

It has become a truism that as the amount of news and information generated per moment continues to grow, so too does the value of aggregation, curation and editing. A point less commonly made is that these aggregators are often limited by time in the sense, whatever the topic, the value of news for the median reader decays extremely rapidly. Some extremists even claim that it’s useless to read the newspaper, so rapidly do things change. The forty eight hours news cycle, in addition to destroying context, has made it impossible for both reporters and viewers to learn from history. See “Is News Memoryless?” (Kautsky et. al. 2014).

A more promising approach to news aggregation (for those who read the news with purpose) is to organize pieces by subject and publish those articles in a book. Paul Krugman did this for himself in The Great Unraveling, bundling selected columns from 1999 to 2003 into a single book, with chapters organized by subject and proceeding chronologically. While the rise and rise of Krumgan’s real-time blogging virtually guarantees he’ll never make such an effort again, a more recent try came from uber-journalist Michael Lewis in Panic!: The Story of Modern Financial Insanity. Financial journalists’ myopic perspective at any given point in time make financial column compilations of years past particularly fun(ny) to read.

Nothing is staler than yesterday’s Wall Street journal (financial news spoils quickly) and reading WSJ or Barron’s pieces from 10 to 20 years ago is just painful.

The title PANIC: The story of modern financial insanity led me to believe the book was about the current crises. The book does say, in very, very fine print “Edited by” Michael Lewis.

-Fritz Krieger, Amazon Reviewer and chief scientist at ISIS

Unfortunately, some philistines became angry in 2008 when they insta-purchased a book called Panic! by Michael Lewis and to their horror, discovered that it contained information about prior financial crises, the nerve of the author to bring us historical perspective, even worse…some of that perspective relating to nations other than the ole’ US of A.

As the more alert readers have noted, almost nothing in the book concerns the 2008 Credit Meltdown, but instead this is merely a collection of news clippings and old magazine articles about past financial crises. You might as well visit a chiropodist’s office and offer them a couple of bucks for their old magazines.

Granted, the articles are by some of today’s finest and most celebrated journalists (although some of the news clippings are unsigned), but do you really want to read more about the 1987 crash or the 1997 collapse of the Thai Baht?

Perhaps you do, but whoever threw this book together wasn’t very particular about the articles chosen. Page 193 reprints an article from “Barron’s” of March, 2000 in which Jack Willoughby presents a long list of Internet companies that he considered likely to run out of cash by 2001. “Some can raise more funds through stock and bond offerings,” he warns. “Others will be forced to go out of business. It’s Darwinian capitalism at work.” True, many of the companies he listed did go belly-up, but on his list of the doomed are

[..]Amazon.com– Someone named Keith Otis Edwards

Perhaps because I was abroad for both the initial disaster and the entire Occupation of Zucotti Park, both events have held my attention. So it is with a mixture of hope and apprehension that I picked up Princeton alum Janet Byrne’s The Occupy Handbook from the public library. The Occupy Handbook is a collection of essays written from 2010 to 2011 by an assortment of first and second-rate authors that attempt to: show what Wall Street does and what it did that led to the most recent crash, explain why our policy apparatus was paralyzed in response to the crash, describe how OWS arose and how it compared with concurrent international movements and prior social movements in the US, and perhaps most importantly, provide policy solutions for the 99% in finance and economics. Janet Byrne begins with a heartfelt introduction:

One fall morning I stood outside the Princeton Club, on West 43rd Street in Manhattan. Occupy Wall Street, which I had visited several times as a sympathetic outsider, has passed its one month anniversary, and I thought the movement might be usefully analyzed by economists and financial writers whose pieces I would commission and assemble into a book that was analytical and- this was what really interested me – prescriptive. I’d been invited to breakfast to talk about the idea with a Princeton Club member and had arrived early out of nervousness.

It seemed a strange place to be discussing the book. I tried the idea out on a young bellhop…

And so it continues. The book is divided into three parts. Part I, broadly speaking, tries to give some economic background on the crash and the ensuing political instability that the crash engendered, up to the first occupation of Zuccotti Park. Part II, broadly speaking, describes the events in Zuccotti Park and around the world as they were in those critical months of fall 2011. Part III, broadly speaking, prescribes solutions to current depression. I say broadly speaking because, as you will see, several essays appear to be in the wrong part and in the worst cases, in the wrong book.

Nasty reader comments and blogging

I’m pretty sure you guys know this already, but I love my regular readers and commenters. It’s a large part of why I blog – I feel like I’m having a super interesting cocktail party every morning in my underwear. I’m investing in the quality of the rest of my day, stealing a moment before my family wakes up so I can articulate one single idea. The payoff is, most of the time, dependably good conversation that lasts all day, or even more than a day, as your comments and emails come in.

Of course, there are sometimes nasty people and comments in addition to thoughtful ones. Not everyone interprets me as trying to figure stuff out, they think I’m being intentionally asinine or manipulative. Or sometimes they just don’t agree with me, and instead of explaining their reasoning they just yell. Or sometimes they are just jerks, getting out their aggression on a stranger.

My first rule is to allow comments that disagree with me, as long as the reasons are articulated and as long as the comment isn’t abusive. Rude is ok, “you are stupid” is not ok.

My second rule is to have a thick skin. I can completely ignore the sentiment of an abusive commenter calling me names, because first of all I’ve heard it all before and second I’m pretty sure it’s not about me.

I’m not saying it doesn’t bother me at all, because obviously it’s a pain to have to go through my email and make sure people are being civil.

For example, whenever I get onto the top 10 of Hacker News, which has been a few times now, I’ve noticed a huge wave of nasty comments. Of course this could be a direct result of how many people I get (thousands per hour), but I don’t think so – the ratio of interesting to abusive comments coming from Hacker News traffic is tiny. It creates nasty work for me, which I feel compelled to do because letting nasty comments stay on my blog makes me feel violated and intentionally misunderstood.

This morning I found this article via Naked Capitalism regarding reader comments, and how nasty ones make subsequent readers evaluate the message differently, and in particular, more negatively. In other words, my intuition was right – it’s super important to curate comments.

My experience with Hacker News has also given me sympathy for Izabella Laba‘s position that she doesn’t accept comments on her blog (read this post for example). She puts herself out there, with strong opinions, and many of her posts are important and thought-provoking. And by the same token people can get pretty threatened by what she has to say. I can well imagine what her experience has been. What if every day was a Hacker News day? What if a majority of comments contained ridiculous and personal attacks? Yuck.

Makes me even more grateful to have you guys.

Prices in the junk bond market

There are various ways of deciding how valuable something is. People spend some amount of time talking about “the current value of future earnings til the end of time” as a rule-of-thumb measurement. That sometimes works (i.e. jives with what the selling price is), but it’s certainly not robust – in a given case, plenty of people think there’s a good reason a stock should be worth more than that, if their personal growth projections are rosy (you could argue that they are still valuing future earnings, but they’ve got a different projection than, say, the current dividends continued as is. Another possibility is that they’re simply valuing future values coming from other people). Similarly, some stocks are underpriced with respect to this baseline. Could it be that they’re cooking their books? If they don’t last til the end of time then they could hardly be making earnings til then (Groupon).

Of course when you go down that road, nothing lasts til the end of time. Never mind companies, the industry in which the company sits will be dead before too long unless it’s food or cosmetics.

Anyway, throw out the future earnings price for a moment, and replace it by something else entirely: there’s a certain amount of money invested in the (international) market at a given moment, and it has to go somewhere. I think of it as a big pot that sloshes around and achieves equilibrium depending on various things like relative interest rates in different countries, and to a lesser extent, regulation in different countries and access to markets. Like, the carry trade is kind of a big deal, and depends almost entirely on the Japanese interest rate being tiny.

Of course it’s not really that simple, since people can and do remove money from the market at certain times – it’s not a closed system. But not as much money is removed as you might think, because if you think about it, lots of people have set up their livelihoods to be investing large pots of money, so they need to appear busy.

Articles like this one from Bloomberg make me think about the “where should we put our money that we need to invest somewhere?” effect is particularly strong right now. We see people “chasing yield” in the junk bond market, buying junk bonds that have positive yields because their options are limited while the Fed keeps the rates really low (this is not a side-effect of the Fed’s keeping the rates low, it’s their goal. They want people to invest in financing businesses, which is what buying junk bonds is).

But they (the investors) all want the same stuff, so the prices are too low high, which is another way of saying the yields are a lot lower than they’d otherwise be if there were other things to buy. This might be a good example of where the price of junk debt is not particularly good at exposing the actual risk of default. Well, it might be an ok indicator of the very short-term default rate, but that’s just because money is so cheap right now, businesses in trouble can just borrow more. It’s kind of a set-up for a bubble.

The article makes the point that once the Fed raises rates, people will flee this market, since they will actually be able to make money again with less risky bonds. The slower actors will be left with much-reduced-in-value junk debt. The big pot of money which is the market will have an entirely new equilibrium point, and there will be lots of death and destruction in the transition. It’s become even more crucial than usual to time the Fed’s moves, but keep in mind money managers are going to stay in there as long as they possibly can because they don’t want to miss yield while their bonuses depend on it (“opportunity costs”). It’s a game of chicken.

Staying with the meta-analysis, can someone do a back-of-the-envelope estimate of how much built-in interest rate risk we’ve taken on by the issuance of so much junk debt in the overall international portfolio? Is it sizeable?

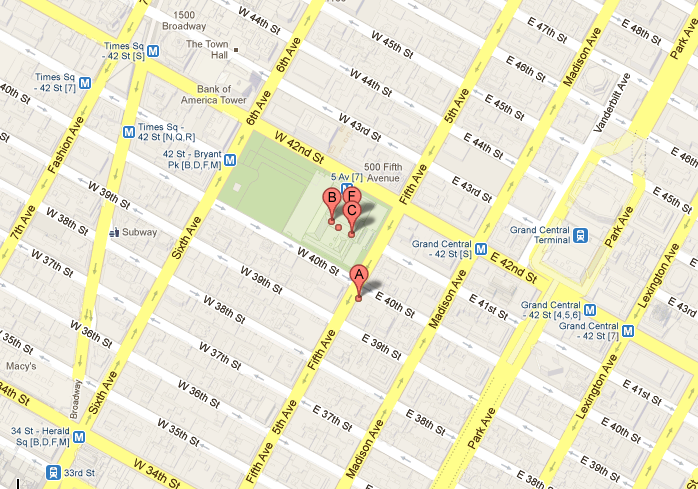

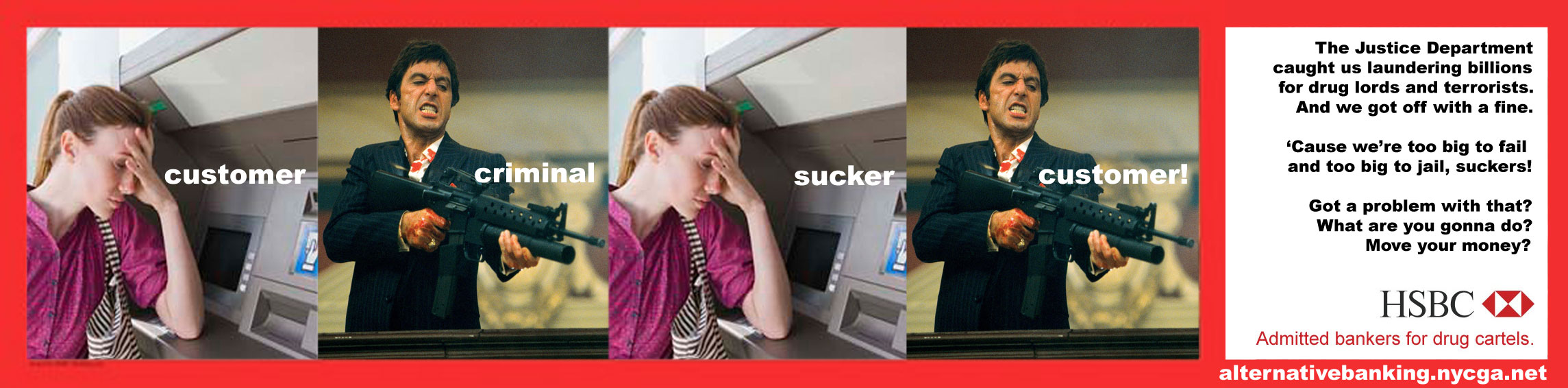

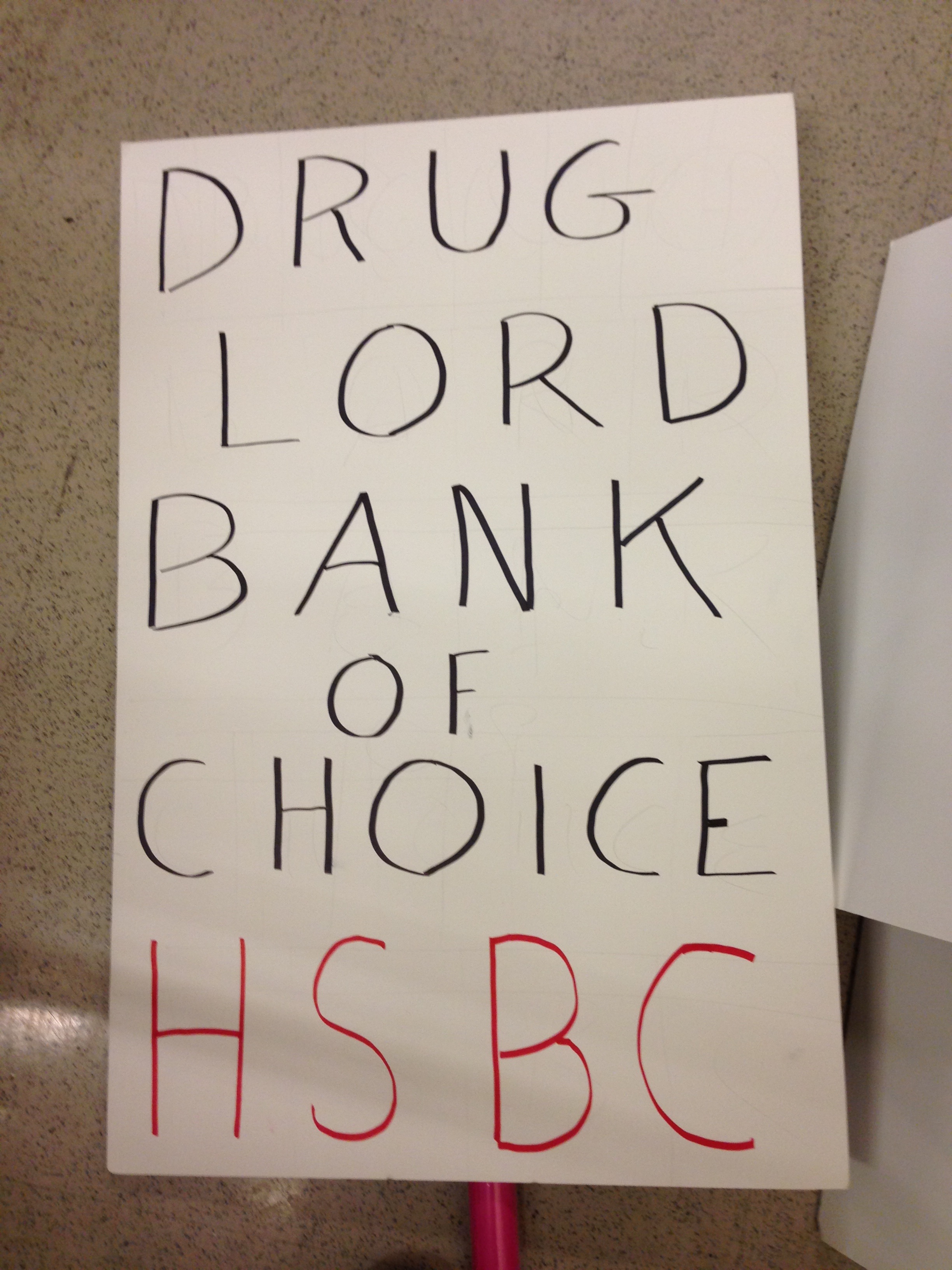

Occupy HSBC: Valentine’s Day protest at noon #OWS

Protest with #OWS Alternative Banking Group

I’m writing to invite you to a protest against mega-bank HSBC at noon on Valentine’s Day (Thursday) starting on the steps of the New York Public Library at 42nd and 5th. Details are here but it’s the big green box on the map on the Fifth Avenue side:

Why are we protesting?

Like you, I’m sure, I’d like nothing more than to stop worrying about shit that goes on in our country’s banks.

We have better things to do with out time than to get annoyed over enormous bonuses being given to idiots for their repeated failures. We’re frankly exhausted from the outrage.

I mean, the average person doesn’t have a job where they get an $11 million bonus instead of a $22 million dollar bonus when they royally screw up. Outside the surreal realm of international banking, the normal response to screw-ups on that level is to get fired.

You might expect a company that has been caught criminally screwing minorities out of fair contracts might be at risk of being closed down, but in this day and age you’d know that big banks, or TIBACO (too interconnected, big, and complex to oversee) institutions, as we in Alt Banking like to call them, are immune to such action.

There’s a clear evolving standard of treatment in the banking sector when it comes to criminal activity:

- the powers that be (SEC, DOJ, etc.) make a huge production over the severity of the fine,

- which is large in dollar amounts but

- usually represents about 10% of the overall profit the given banks made during their exploit.