Archive

Nafeez Ahmed to join Alt Banking this Sunday

I am super excited to announce that best-selling British author Nafeez Ahmed will be speaking at the Alt Banking group this Sunday. The title of his talk is Mass Surveillance and the Crisis of Civilization: The inevitable collapse of the old paradigm and the potential for the rise of the new.

Ahmed is an international security scholar and investigative journalist and executive director of the Institute for Policy Research & Development. He writes for The Guardian on the geopolitics of interconnected environmental, energy and economic crises, and is currently on tour in the United States to launch his science fiction novel, Zero Point.

As advance reading for this talk, we recommend browsing through his Guardian articles, including the widely read June 2014 piece, Pentagon preparing for mass civil breakdown. He’s also recently published on occupy.com an article entitled Exposed: Pentagon Funds New Data-Mining Tools To Track and Kill Activists, Part I.

Details: Ahmed will speak from 2-3pm on Sunday, August 24th, in room 409 of the International Affairs Building of Columbia University at W. 118th Street and Amsterdam Ave. After that we will have our regular meeting from 3-5pm in the same room, followed by food and drinks at Amsterdam Tapas. Please join us! And if you can’t this weekend but want to be on our mailing list, please email that request to alt.banking.ows@gmail.com.

Zephyr Teachout to visit Alt Banking this Sunday

I’m excited to announce that Zephyr Teachout, a Fordham Law School professor who is running against Andrew Cuomo for Governor of New York, will be coming to speak to the Alternative Banking group next Sunday, July 13th, from 3pm-5pm in the usual place, Room 409 of the International Affairs Building at 118th and Amsterdam. More about Alt Banking on our website.

Title: Teachout-Wu vs. Cuomo-Hochul in the Democratic Primary in New York!

Description: Come hear candidate Teachout talk about her anti-corruption trust-busting campaign against Governor Cuomo.

Background: Teachout is an antitrust and media expert who served as the Director of Internet organizing for the 2004 Howard Dean Presidential Campaign. She co-founded A New Way Forward, an organization built to break up the power of big banks. Teachout was the first national director of the Sunlight Foundation. More here.

If we have time after talking to Zephyr we will discuss Stiglitz’s article, The Myth Of America’s Golden Age.

Please make time to come hear Zephyr, and please spread the word.

Review: House of Debt by Atif Mian and Amir Sufi

I just finished House of Debt by Atif Mian and Amir Sufi, which I bought as a pdf directly from the publisher.

This is a great book. It’s well written, clear, and it focuses on important issues. I did not check all of the claims made by the data but, assuming they hold up, the book makes two hugely important points which hopefully everyone can understand and debate, even if we don’t all agree on what to do about them.

First, the authors explain the insufficiency of monetary policy to get the country out of recession. Second, they suggest a new way to structure debt.

To explain these points, the authors do something familiar to statisticians: they think about distributions rather than averages. So rather than talking about how much debt there was, or how much the average price of houses fell, they talked about who was in debt, and where they lived, and which houses lost value. And they make each point carefully, with the natural experiments inherent in our cities due to things like available land and income, to try to tease out causation.

Their first main point is this: the financial system works against poor people (“borrowers”) much more than rich people (“lenders”) in times of crisis, and the response to the financial crisis exacerbated this discrepancy.

The crisis fell on poor people much more heavily: they were wiped out by the plummeting housing prices, whereas rich people just lost a bit of their wealth. Then the government stepped in and protected creditors and shareholders but didn’t renegotiate debt, which protected lenders but not borrowers. This is a large reason we are seeing so much increasing inequality and why our economy is stagnant. They make the case that we should have bailed out homeowners not only because it would have been fair but because it would have been helpful economically.

The authors looked into what actually caused the Great Recession, and they come to a startling conclusion: that the banking crisis was an effect, rather than a cause, of enormous household debt and consumer pull-back. Their narrative goes like this: people ran up debt, then started to pull back, and and as a result the banking system collapsed, as it was utterly dependent on ever-increasing debt. Moreover, the financial system did a very poor job of figuring out how to allocate capital and the people who made those loans were not adequately punished, whereas the people who got those loans were more than reasonably punished.

About half of the run-up of household debt was explained by home equity extraction, where people took out money from their home to spend on stuff. This is partly due to the fact that, in the meantime, wages were stagnant and home equity was a big thing and was hugely available.

But the authors also made the case that, even so, the bubble wasn’t directly caused by rising home valuations but rather to securitization and the creation of “financial innovation” which made investors believe they were buying safe products which were in fact toxic. In their words, securities are invented to exploit “neglected risks” (my experience working in a financial risk firm absolutely agrees to this; whenever you hear the phrase “financial innovation,” please interpret it to mean “an instrument whose risk hides somewhere in the creases that investors are not yet aware of”).

They make the case that debt access by itself elevates prices and build bubbles. In other words, it was the sausage factory itself, producing AAA-rated ABS CDO’s that grew the bubble.

Next, they talked about what works and what doesn’t, given this distributional way of looking at the household debt crisis. Specifically, monetary policy is insufficient, since it works through the banks, who are unwilling to lend to the poor who are already underwater, and only rich people benefit from cheap money and inflated markets. Even at its most extreme, the Fed can at most avoid deflation but it not really help create inflation, which is what debtors need.

Fiscal policy, which is to say things like helicopter money drops or added government jobs, paid by taxpayers, is better but it makes the wrong people pay – high income earners vs. high wealth owners – and isn’t as directly useful as debt restructuring, where poor people get a break and it comes directly from rich people who own the debt.

There are obstacles to debt restructuring, which are mostly political. Politicians are impotent in times of crisis, as we’ve seen, so instead of waiting forever for that to happen, we need a new kind of debt contract that automatically gets restructured in times of crisis. Such a new-fangled contract would make the financial system actually spread out risk better. What would that look like?

The authors give two examples, for mortgages and student debt. The student debt example is pretty simple: how quickly you need to pay back your loans depends in part on how many jobs there are when you graduate. The idea is to cushion the borrower somewhat from macro-economic factors beyond their control.

Next, for mortgages, they propose something the called the shared-responsibility mortgage. The idea here is to have, say, a 30-year mortgage as usual, but if houses in your area lost value, your principal and monthly payments would go down in a commensurate way. So if there’s a 30% drop, your payments go down 30%. To compensate the lenders for this loss-share, the borrowers also share the upside: 5% of capital gains are given to the lenders in the case of a refinancing.

In the case of a recession, the creditors take losses but the overall losses are smaller because we avoid the foreclosure feedback loops. It also acts as a form of stimulus to the borrowers, who are more likely to spend money anyway.

If we had had such mortgage contracts in the Great Recession, the authors estimate that it would have been worth a stimulus of $200 billion, which would have in turn meant fewer jobs lost and many fewer foreclosures and a smaller decline of housing prices. They also claim that shared-responsibility mortgages would prevent bubbles from forming in the first place, because of the fear of creditors that they would be sharing in the losses.

A few comments. First, as a modeler, I am absolutely sure that once my monthly mortgage payment is directly dependent on a price index, that index is going to be manipulated. Similarly as a college graduate trying to figure out how quickly I need to pay back my loans. And depending on how well that manipulation works, it could be a disaster.

Second, it is interesting to me that the authors make no mention of the fact that, for many forms of debt, restructuring is already a typical response. Certainly for commercial mortgages, people renegotiate their principal all the time. We can address the issue of how easy it is to negotiate principal directly by talking about standards in contracts.

Having said that I like the idea of having a contract that makes restructuring automatic and doesn’t rely on bypassing the very real organizational and political frictions that we see today.

Let me put it this way. If we saw debt contracts being written like this, where borrowers really did have down-side protection, then the people of our country might start actually feeling like the financial system was working for them rather than against them. I’m not holding my breath for this to actually happen.

Organizing Walmart Workers: Summer for Respect #OWS

This coming Sunday my friend Adam Reich is coming to Alternative Banking to talk about his work as the faculty director of a collaborative project this summer between Columbia’s INCITE and the OUR Walmart campaign.

The plan involves twenty students to scatter across the country, organizing and conducting oral history interviews alongside Walmart workers in five regions.

It is also, not coincidentally, the 50th anniversary of the Freedom Summer of 1964, when a bunch of volunteers including students helped register black Mississippians to vote.

Adam is an activist and a sociologist professor at Columbia. He is also an author of three books including Selling Our Souls: The Commodification of Hospital Care in the United States.

Details are as follows, and I hope you can come:

Where: Room 409 of the International Affairs Building at 118th and Amsterdam.

When: Sunday, June 8th, 2-3pm.

Weekly Slate Money podcast

Aunt Pythia is bowing out today from an exhausting week, and she extends her apologies.

But if you are looking for opinionated advice, please feel free to try out my recent Slate Money podcast with Felix Salmon and Jordan Weissmann. This week I complain about Ben Bernanke, I talk reparations, and complain about white collar crime going unpunished. Last week was also great, because I got to complain about Tim Geithner. And two weeks ago we started the podcast talking Alibaba and the minimum wage.

If you enjoy listening, please subscribe via iTunes and also, please rate the podcast on iTunes so we get more traffic.

How do we prevent the next Tim Geithner?

When you hate on certain people and things as long as I’ve hated on the banking system and Tim Geithner, you start to notice certain things. Patterns.

I read Tim Geithner’s book Stress Test last week, and instead of going through and sharing all the pains of reading it, which were many, I’m going to make one single point.

Namely, Tim was unqualified for his jobs and head of the NY Fed, during the crisis, and then as Obama’s Treasury Secretary. He says so a bunch of times and I believe him. You should too.

He even is forced at some point to admit he had no idea what banks really did, and since he needed someone or something to blame for his deep ignorance, he somehow manages to say that Brooksley Born was right, that derivatives should have been regulated, but that since she was at the CFTC everybody (read: Geithner’s heroes Larry Summers and Robert Rubin) dismissed her out of hand, and that as a result he had no ability to look into the proliferating shadow banking or stuff going on at all the investment banks and hedge funds. So it was kind of her fault that he wasn’t forced to understand stuff, even though she warned people, and when shit got real, all he could do was preserve the system because the alternative would be chaos. And people should fucking thank him. That’s his 600 page book in a nutshell.

Let’s put aside Tim Geithner’s mistakes and his narrow outlook on what could have been done better, and even what Dodd-Frank should accomplish, for a moment. It’s hard to resist complaining about those things, but I’ll do my best.

The truth is, Tim Geithner was a perfect product of the system. He was an effect, not a cause.

When I dwell on the fact that he got the NY Fed job with no in-the-weeds knowledge or experience on how banks operate, there’s no reason, not one single reason, to think it’s not going to happen again.

What’s going to prevent the next NY Fed bank head from being as unqualified as Tim Geithner?

Put it another way: how could we possibly expect the people running the regulators and the Treasury and the Fed to actually understand the system, when they are appointed the way they are? In case you missed it, the process currently is their ability to get along with Larry Summers and Robert Rubin and to look like a banker.

Before you go telling me I’m asking for a Goldman Sachs crony to take over all these positions, I’m not. It’s actually not impossible to understand this system for a curious, smart, skeptical, and patient person who asks good questions and has the power to make meetings with heads of trading floors. And you don’t have to become captured when you do that. You can remember that it’s your job to understand and regulate the system, that it’s actually a perfectly reasonable way to protect the country. From bankers.

Here’s a scary thought, which would be going in the exact wrong direction: we have Hillary Clinton as president and she brings in all the usual suspects to be in charge of this stuff, just like Obama did. Ugh.

I feel like a questionnaire is in order for anyone being considered for one of these jobs. Things like, how does overnight lending work, and what is being used for collateral, and what have other countries done in moments of financial crisis, and how did that work out for them, and what is a collateralized debt obligation and how does one assess the associated risks and who does that and why. Please suggest more.

The US political system serves special interests and the rich

A paper written by Martin Gilens and Benjamin Page and entitled Testing Theories of American Politics: Elites, Interest Groups, and Average Citizens has been recently released and reported on (h/t Michael Crimmins) that studies who has influence on policy in the United States.

Here’s an excerpt from the abstract of the paper:

Multivariate analysis indicates that economic elites and organized groups representing business interests have substantial independent impacts on U.S. government policy, while average citizens and mass-based interest groups have little or no independent influence.

A word about “little or no independent influence”: the above should be interpreted to mean that average citizens and mass-based groups only win when their interests align with economic elites, which happens sometimes, or business interests, which rarely happens. It doesn’t mean that average citizens and mass-based interest groups never ever get what they want.

There’s actually a lot more to the abstract, about abstract concepts of political influence, but I’m ignoring that to get to the data and the model.

The data

The found lots of polls on specific issues that were yes/no and included information about income to determine what poor people (10th percentile) thought about a specific issue, what an average (median income) person thought, and what a wealthy (90th percentile) person thought. They independently corroborated that their definition of wealthy was highly correlated, in terms of opinion, to other stronger (98th percentile) definitions. In fact they make the case that using 90th percentile instead of 98th actually underestimates the influence of wealthy people.

For the sake of interest groups and their opinions on public policy, they had a list of 43 interest groups (consisting of 29 business groups, 11 mass-based groups, and 3 others) that they considered “powerful” and they used domain expertise to estimate how many would oppose or be in favor of a given issue, and more or less took the difference, although they actually did something a bit fancier to reduce the influence of outliers:

Net Interest Group Alignment = ln(# Strongly Favor + [0.5 * # Somewhat Favor] + 1) – ln(#

Strongly Oppose + [0.5 * # Somewhat Oppose] + 1).

Finally, they pored over records to see what policy changes were actually made in the 4 year period after the polls.

Statistics

The different groups had opinions that were sometimes highly correlated:

Note the low correlation between mass public interest groups (like unions, pro-life, NRA, etc) and average citizens’ preferences and the negative correlation between business interests and elites’ preferences.

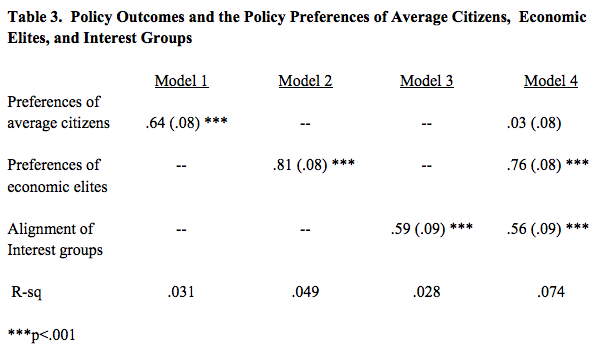

Next they did three bivariate regressions, measuring the influence of each of the groups separately, as well as one including all three, and got the following:

This is where we get our conclusion that average citizens don’t have independent influence, because of this near-zero coefficient in Model 4. But note that if we ignore elites and interest groups, we do have 0.64 in Model 1, which indicates that preferences of the average citizens are correlated with outcomes.

The overall conclusion is that policy changes are determined by the elites and the interest groups.

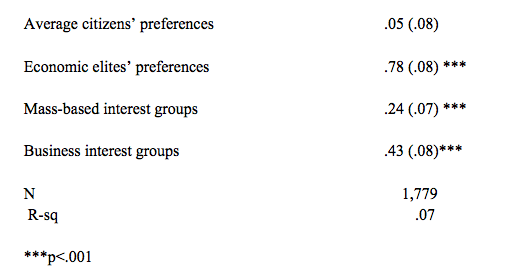

We can divide the interest groups into business versus mass-based and check out how the influence is divided between the four defined groups:

Caveats

This stuff might depend a lot on various choices the modelers made as well as their proxies. It doesn’t pick up on smaller special interest groups. It doesn’t account for all possible sources of influence and so on. I’d love to see it redone with other choices. But I’m impressed anyway with all the work they put into this.

I’ll let the authors have the last word:

What do our findings say about democracy in America? They certainly constitute troubling news for advocates of “populistic” democracy, who want governments to respond primarily or exclusively to the policy preferences of their citizens. In the United States, our findings indicate, the majority does not rule — at least not in the causal sense of actually determining policy outcomes. When a majority of citizens disagrees with economic elites and/or with organized interests, they generally lose. Moreover, because of the strong status quo bias built into the U.S. political system, even when fairly large majorities of Americans favor policy change, they generally do not get it.

How recently have you experienced democracy? #OWS

A few weeks ago Omar Freilla came to talk to my Occupy group. Omar is a founder of the Green Worker Cooperatives and shared his experience as an organizer.

He is a well-spoken guy and talked passionately about forming community cooperatives, where workers “have a direct role in decision-making and a share of all profits, build community wealth and help make a democratic economy real.”

At one point in his presentation, Omar asked us was how recently we’d “experienced democracy.”

On the face of it I didn’t think it was a fair question, especially when he compared it to experiencing anger or happiness. After all, democracy isn’t an emotion and I can’t experience democracy, say, by myself in a room, but of course I can conjure up emotions by myself in a room, especially if I have a laptop, wifi, and Netflix to help me.

But since his visit, I have to admit I have dwelled on that question and it’s become more and more reasonable in my mind, although I made two decisions on how to interpret it.

First of all, I chose to interpret it not as a formal gesture of democracy, like asking how recently have you voted in a formal election. Instead, it’s a local decision-making process question: how recently has your vote mattered in a local decision that affects a group?

Second, it’s not really about me. It’s about looking around and deciding who around me gets to participate in democratic decisions and who doesn’t.

For example, it might be at work. Although I personally get to make a lot of decisions at work, that fact clearly separates me from tons of people who simply get told what to do by some kind of authority. And there is an important distinction between people who have a manager but get to make decisions internal to their projects and people who have every decision laid out for them.

And that latter workplace anti-democratic situation is, I imagine, maximally soul-crushing, and is the audience that Omar is worried about and is reaching out to. And that’s why his question turns out to be a really good question after all.

I also consider democracy inside my own family. Since I’m the mom of the family, I tend to make more decisions that affect my little group than other people, but now I’m more sensitive to sharing that power there when I can. Turns out my kids love making decisions, it makes them gleeful in fact, even if it’s just what to eat for dinner. And they make good decisions too, which I’m consistently proud of.

My final example is Occupy, which is by construction a direct democracy, and I know how good participating and experiencing democracy actually feels there, and it’s a big part of why it works.

What about you? How recently have you experienced democracy?

Envy, greed, and the American Dream #OWS

I was sent this Falkenblog post entitled Why Envy Dominates Greed a while back (hat tip David Murrell). The post suggests an interesting thought experiment which I’d like to discuss this morning.

Namely, it asks us to examine the extent to which our economic assumption that “everyone is working in their own self-interest” can be replaced by the assumption that “everyone is working to improve their relative ranking” and whether you’d get more clarity from economics that way.

I’ve done myself the favor of ignoring everything author Eric Falkenstein actually says about the economic theory, because he’s focusing on investing in the stock market, which honestly only a minority of people ever do even once. Even so I’d like to consider this idea of envy versus greed and try to make sense of it.

First of all, I do think that a certain kind of relativity combined with proximity is deeply important to humans. When members of my Occupy group talk about living on $2 a day while sleeping at homeless shelters in New York City, surrounded by men in suits with chauffeurs, it is very relevant that the privations described are combined with with a deep sense of humiliation of their understanding of their relative position. These are highly intelligent people who know how things look and they feel it keenly.

Similarly, when I think about poor people in other countries, it’s a different level of destitution than we see here, and yet it doesn’t make me want to drop everything and work in India. There’s something about proximity that we all respond to, and which has been well examined by social scientists.

Going back to my New York friend: is that envy being displayed, exactly? I don’t think so. I think it’s something more like dispossession and despair. And it’s honestly something I believe our natures would rather avoid, but sometimes just slaps us in our face, especially in places like New York City.

I’m not throwing envy out altogether. In fact, I do think envy is strongly at work, but only at a local level. I am working at Columbia now, so it’s natural and proper that I am envious of my colleague’s slightly-larger office. I ignore the stuff I don’t see like how the trustees are chosen and treated. A person in a given town is envious of their neighbor’s house or car or job or wife, but they don’t think about what’s happening in a different neighborhood. In fact they might obsess over such things. It happens. But again, it’s local.

Evidence that people only think very locally about wealth and inequality is everywhere; so when people are polled and asked to describe income or wealth inequality, they always think it’s much less skewed than it is. Why? I’ll guess. It’s because they extrapolate from their very local experience, where there the outliers are not so very outlying at all. It’s a safe kind of assumption that doesn’t boil the blood.

So envy is there, it’s powerful, but it biases us enormously. If anything, I’m starting to think envy is something to distract us from something more dangerous, which is that sense of privation and dispossession, which runs deeper and is more anarchic. By contrast, envy seems like a myopic feeling that keeps us acting safely inside the system, where if we follow the rules but we’re a little bit better at them, we will get that bigger office or bigger car.

In the end, I reject envy as a unifying glue that describes our world, at least in times of severe inequality like now. It just doesn’t address the growing hostility that I’m sensing, which is that second kind of feeling, which exists beyond envy.

Moreover, I think the assumption that everyone is feeling something as small as envy, or rather the projection of envy onto the entire population, is damaging.

So, for example, there was an New York Times Op-Ed recently entitled Capitalize Workers! that suggested we get more people involved for saving for their retirement by investing in the stock market with “minimum pensions”.

I think the idea here is that everyone wants a piece of that amazing stock market return. But if you think about where people actually are financially, it’s such a weirdly out-of-touch plan, the idea that everyone is a Wall Street trader or wants to be.

For most people I meet and talk to, at this point retirement is not at all about the thrill of risk-taking, but rather the avoidance of risk altogether. If you asked those people, they’d rather just have their Social Security benefits doubled. They are not trying to take their chances to double their money, but rather trying to eke out a retirement without severe pain.

Why is this happening? Why are the authors of this piece, who both work at the think tank Third Way, making such bizarre assumptions about how poor people want to retire? My first guess was that they are just working with the funds on Wall Street who would reap (even more) profits if more people invested.

But another less suspicious possibility is given by my above observation. Namely, they are projecting their myopic envy, that makes sense in their world, onto the poor and middle class worrying about retirement.

In their neighborhood, the way envy works is about trading and making big gains with extra money, but of course to do that you have to have extra money to start out with. In other words, the distance between the authors and the people they claim to be trying to help is too large for their system of envy to translate meaningfully.

Defining poverty #OWS

I am always amazed by my Occupy group, and yesterday’s meeting was no exception. We decided to look into redefining the poverty line, and although the conversation took a moving and deeply philosophical turn, I’ll probably only have time to talk about the nuts and bolts of formulas this morning.

The poverty line, or technically speaking the “poverty threshold,” is the same as it was in 1964 when it was invented except for being adjusted for inflation via the CPI.

In the early 1960’s, it was noted that poor families spent about a third of their money on food. To build an “objective” measure of poverty, then, they decided to measure the cost of an “economic food budget” for a family of that size and then multiply that cost by 3.

Does that make sense anymore?

Well, no. Food has gotten a lot cheaper since 1964, and other stuff hasn’t. According to the following chart, which I got from The Atlantic, poor families now spend about one sixth of their money on food:

Rich people spend even less on food.

Now if you think about it, the formula should be more like “economic food budget” * 6, which would effectively double all the numbers.

Does this matter? Well, yes. Various programs like Medicare and Medicaid determine eligibility based on poverty. Also, the U.S. census measures poverty in our country using this yardstick. If we double those numbers we will be seeing a huge surge in the official numbers.

Not that we’d be capturing everyone even then. The truth is, in some locations, like New York, rent is so high that the formula would likely be needing even more adjustment. Although food is expensive too, so maybe the base “economic food budget” would simply need adjusting.

As usual the key questions are, what are we accomplishing with such a formula, and who is “we”?

Lobbyists have another reason to dominate public commenting #OWS

Before I begin this morning’s rant, I need to mention that, as I’ve taken on a new job recently and I’m still trying to write a book, I’m expecting to not be able to blog as regularly as I have been. It pains me to say it but my posts will become more intermittent until this book is finished. I’ll miss you more than you’ll miss me!

On to today’s bullshit modeling idea, which was sent to me by both Linda Brown and Michael Crimmins. It’s a new model built in part by the former chief economist for the Commodity Futures Trading Commission (CFTC) Andrei Kirilenko, who is now a finance professor at Sloan. In case you don’t know, the CFTC is the regulator in charge of futures and swaps.

I’ll excerpt this New York Times article which describes the model:

The algorithm, he says, uncovers key word clusters to measure “regulatory sentiment” as pro-regulation, anti-regulation or neutral, on a scale from -1 to +1, with zero being neutral.

If the number assigned to a final rule is different from the proposed one and closer to the number assigned to all the public comments, then it can be inferred that the agency has taken the public’s views into account, he says.

Some comments:

- I know really smart people that use similar sentiment algorithms on word clusters. I have no beef with the underlying NLP algorithm.

- What I do have a problem with is the apparent assumption that the “the number assigned to all the public comments” makes any sense, and in particular whether it takes into account “the public’s view”.

- It sounds like the algorithm dumps all the public comment letters into a pot and mixes it together to get an overall score. The problem with this is that the industry insiders and their lobbyists overwhelm public commenting systems.

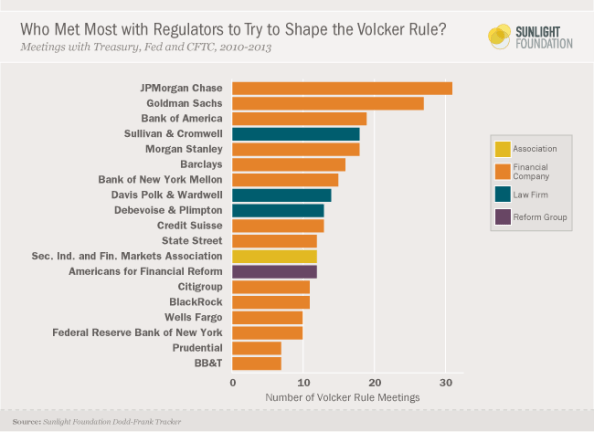

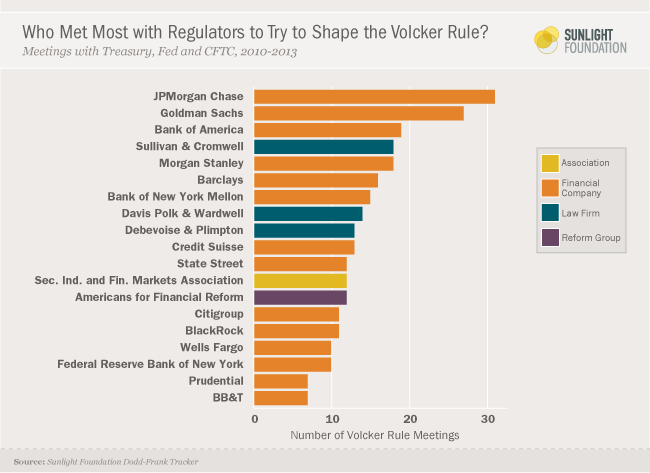

- For example, go take a look at the list of public letters for the Volcker Rule. It’s not unlike this graphic on the meetings of the regulators on the Volcker Rule:

- Besides dominating the sheer number of letters, I’ll bet the length of each letter is also much longer on average for such parties with very fancy lawyers.

- Now think about how the NLP algorithm will deal with this in a big pot: it will be dominated by the language of the pro-industry insiders.

- Moreover, if such a model were to be directly used, say to check that public commenting letters were written in a given case, lobbyists would have even more reason to overwhelm public commenting systems.

The take-away is that this is an amazing example of a so-called objective mathematical model set up to legitimize the watering down of financial regulation by lobbyists.

Update: I’m willing to admit I might have spoken too soon. I look forward to reading the paper on this algorithm and taking a deeper look instead of relying on a newspaper.

Could we use eminent domain to help suffering homeowners? (#OWS)

Here are two things you might have some trouble believing if you read the papers regularly and find yourself convinced we are in a housing recovery. First, there are still huge numbers of homeowners on the brink of, or just starting to enter, foreclosure. Second, many of the banks foreclosing on those properties do not have clear legal ownership over the mortgages in question.

Obama should have addressed the first problem through TARP way back in 2008. In fact mortgage modification was an intention of TARP that was promised Congress when it passed the second half of the money but it never happened. Instead Obama came up with the garbage called HAMP, which has been dreadfully implemented and possibly a net harmful program.

Even without Obama, we should have seen a willingness to renegotiate debt. After all, we can negotiate credit card debt, and businesses routinely renegotiate their mortgages. Why are private home mortgages kept airtight? I guess the banks see it as in their interest not to allow negotiations, and whatever the banks want, the banks seem to get.

The second problem, which is essentially one of botched paperwork (explained here), is probably technically the job of some regulator to deal with, but nobody wants to “blow up the system” so nobody is dealing with it. This is especially ironic considering how often we hear about the so-called sanctity of the contract.

The result of these huge looming problems is that banks got bailed out and the system never got cleared of its actual debt and paperwork problems,.

Enter the concept of using eminent domain to force these two issues. Strike Debt, an offshoot of Occupy Wall Street, is pushing this in a few nationwide court cases, for example in Richmond, California.

More recently, and what inspired this post this morning, is a plan cooked up by Strike Debt using eminent domain to force courts to clear up broken chains of title, written by Hannah Appel and JP Massar.

This idea is on its face unappealing, given the history of that crude tool eminent domain. Everyone I meet has their own stories, but start here for a short list of eminent domain abuses.

And it might not work, either. A district judge might not want to deal with the complexity of the issue and might just let the bad paperwork through.

For that matter, many concerns have been voiced about the practicality of this approach, and one that deeply resonates with me is the idea of using it against current mortgages – i.e. mortgages where the homeowner is up-to-date with payment. Using eminent domain in such a case could set a precedent whereby, even though someone has been taking care of their property, the city uses eminent domain to condemn it based on historical data which implies the owner is likely to neglect their property. That would not be good enough. As far as I know the current plan only uses mortgages where there have been missed payments, though.

The bottomline is this: we’re in a situation where all these homeowners are being crushed with unreasonable monthly payments, and hugely inflated principals, where the legal ownership of the mortgage itself is under question, and nobody seems to want to do squat about it. Maybe it’s time a crude tool is used against a cruel enemy.

Crashing a Wall Street party

I’m just recovering from a killer flu that had me wheezing and miserable for 5 days. I have a whole backlog of rants and vents but no time this morning to even start, so instead let me suggest you read this article (hat tip Chris Wiggins) about a New York Times reporter who crashed the yearly party of Kappa Beta Phi, a Wall Street secret society. Pretty amazing, if true.

Join Alt Banking #OWS

I’m really proud of my Occupy group, Alt Banking. We continue to meet every Sunday at Columbia and we welcome new members. I wanted to throw down a few reasons you might consider coming to our meetings.

If you’re interested, please email alt.banking.ows@gmail.com and ask to be added to the google group. Emails go out Saturday about details on Sunday meetings. And if you’re passing through New York on a Sunday, please consider just joining for one day!

Website

An amazing team of activists have been making the Alt Banking website better and better every week. It’s pretty much up to date and contains real resources for people who can’t come to the meetings, as well as for people who want to continue the conversation between meetings.

Please take a look and give us suggestions to make it even better.

Speakers

We’ve had some amazing speakers come to Alt Banking in the past – including Neil Barofsky, Sheila Bair, Merlyna Lim, Tom Adams, Moe Tkacik, and most recently Stanley Aronowitz – and many more coming up soon. I’d say it’s a great group to know about for the speaker list alone. The speakers come from 2-3pm before the regular 3-5 meeting on Sundays.

Projects

As I’ve mentioned before on mathbabe, we wrote a pretty cool book called Occupy Finance, and we recently got a second printing made since the first printing went so quickly. If you’d like a physical copy, please email alt.banking.ows@gmail.com with your address. A free pdf is available here.

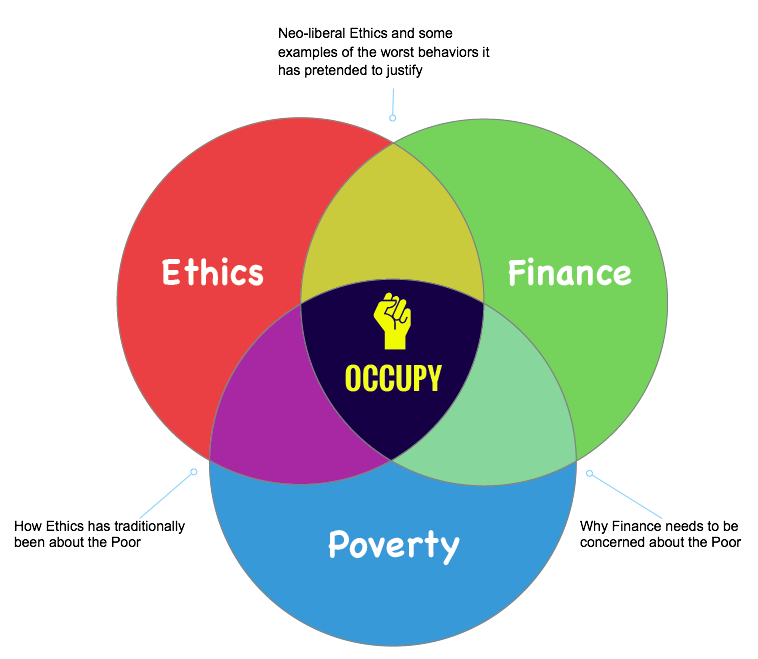

But that’s not all. Last week we decided to start our next big project, which is likely going to be some combination of a book and a movie, or a series of videos, or possibly a series of animated shorts, or something along those lines (still under consideration!). The content of the project is centered around three topics and their intersections, and we already have a cool “first iteration” visual due to Laminated Lychee (note the nerdy use of the Venn Diagram):

We’re also looking to have a cool roll-out for that project, possibly next September, possibly with a day-long conference of activists and lectures and activities. We could really use some help!

Fun

I also wanted to mention that we have a blast every week, and we often go out for dinner and/or a glass of wine or beer after the regular meeting. It’s really a great group of fun people.

Friday protest in Queens against Fast Track TPP #OWS

This coming Friday will be a coordinated day of action against the Trans Pacific Partnership Agreement (TPP). Actions will take place all over the world with the New York version taking place at noon in Queens (details below).

Why anti-TPP? Isn’t “free trade” a good thing? The word “free” is in it!

Language is a tricky thing, and people choose the names of their initiatives to make them sound good. We know that from the “pro life” and “pro choice” debate.

Turns out that, in this case, “free trade” is a weird phrase to describe a campaign that increases the legal power of corporations (ex: tobacco companies) against governments (ex: Namibia).

I’ve written about it here, but if you haven’t seen this Huffington Post video (h/t Matt Stoller) then please take the time. It’s funny and it’s an amazingly clear and beautiful explanation of the dangers of TPP, and especially the so-called “Fast Tracking” of that international agreement.

Details for the Queens anti-TPP rally on Friday

- TUG O’ JOE- a street theater performance where Crowley will be pulled by characters on both sides of the issues – corporate monsters on the one and the defenders of our jobs, health and environment on the other!

- CROWLEY – STOP BEING SPEECHLESS! – another street theater bit, satirizing Crowley’s “Speechless” presentation on the floor of Congress!

- NEW TPP SONGS by the NYC Raging Grannies!

- ROUSING SPEECHES by Mimi Rosenberg (WBAI’S Building Bridges: Your Community and Labor Report), Malú Huacuja del Toro (anti-NAFTA and Zapatista solidarity activist, acclaimed author), Corrine Rosen (Food and Water Watch), Freddy Castiblano (Latin America solidarity activist and small business owner), and others!

- Time: 10am – noon

- Location: Rep. Crowley’s Queens Office, 82-11 37th Ave between 82th and 83rd Streets, Jackson Heights, Queens. Please arrive on time as we may march! If you’re late and can’t find us, call Wendy at (347) 881-5635 or Carlos at (646) 416-3440.

- Directions: Take the 7 train to 82nd Street-Jackson Heights

- Additional Info: Phone: (718) 218-4523 Email: info@tradejustice.net Web: http://tradejustice.net/tpp

Jamie Dimon’s bonus too low – shoulda been $100 million at least

Crossposted on the Alt Banking blog, the below reflects a discussion at Alt Banking from last Sunday’s meeting.

People have been making a big fuss about JP Morgan Chase CEO Jamie Dimon’s recent raise. They seem to think that, what with all the lawsuits that JP Morgan Chase has been involved in this past year, exposing so much fraudulent behavior which directly contributed to so much human suffering, the guy should be somewhat humbled and punished. They even wanna question his right to stock options he shoulda had way back in 2008, when the world was on fire. The nerve!

I mean, maybe by some definition of “earned” he doesn’t deserve those 20 sticks. Maybe they think they have better plans for the bonus money. But from where I sit, the guy should have gotten way more, considering he set the price of fraud by big banks so low and in so many different ways.

I estimate that he should have gotten at least $100 million, using a very basic fact that the regulatory arbitrage which he displayed, and which now exists as a precedent for all bankers for the rest of eternity, benefitted not just him, not just JP Morgan Chase, but all the Too-Big-To-Fail banks. For that reason, every TBTF bank should give him at least $20 million as a reward for their future profitable fraudulent earnings. Since there are at least 5 TBTF banks, I’m just scaling up in a super reasonable way.

I know that might sound weird, for Bank of America and Goldman Sachs, which are generally speaking competitors to JP Morgan, to give Jamie Dimon cash money. And they might want to keep it on the DL for that matter, for the sake of appearances.

But after all, this is the guy who called Attorney General Eric Holder on the phone and negotiated a settlement, for christ’s sake! Who DOES that? That’s really above and beyond the chutzpah of even the most criminal of masterminds. Only the creamiest of the crop, only the most devoted of banker psychopaths can get away with that shit. That is to say, Jamie Dimon, and maybe Lloyd Blankfein (Dear Lloyd: I don’t doubt for a minute that you will have your day too, very soon, and then all the big boys will pitch in for your supersized bonus).

So what are you waiting for, Citigroup? Wells? When are you guys ponying up what we all know Dimon deserves from all of the elite institutions protected from prosecution? I say you guys perform the equivalent of a kowtow in Wall Street terms, which is of course monetized, in the form of a check. Send it on over.

Come to think of it we should also offer extra cash to HSBC’s legal team, and for that matter Eric Holder himself. If it hasn’t already been done.

Four Horsemen showing this Sunday in Alt Banking #OWS

This coming Sunday we’re having a special Alt Banking meeting where, instead of having our usual format, we’re all watching Four Horsemen, a recent documentary film put out by Renegade Economists (on twitter as @RenegadeEcon). We’ll first watch the film and then have a discussion about it.

The entire film is available on youtube here, although I paid 5 bucks to download it from this website in preparation for this coming Sunday’s viewing and discussion. Here’s the trailer, it looks amazing:

Feel free to come to Sunday’s meeting, it starts at 2pm and is uptown at Columbia University. Send an email to alt.banking.ows@gmail.com and ask to be added to the email list for details, or go to the alt banking webpage for details.

Judge Rakoff explains why no banker is in jail #OWS

United States District Judge Jed S. Rakoff is already kind of a hero to me, given that he’s the guy who rejected a “do not admit wrongdoing” settlement between Citigroup and the SEC over mortgage-backed securities fraud because, according to Rakoff, the proposed settlement was “neither fair, nor reasonable, nor adequate, nor in the public interest.”

More recently Rakoff has written a fine essay in the New York Review of Books entitled The Financial Crisis: Why Have No High-Level Executives Been Prosecuted? which I will summarize below but is well worth your time to read.

Rakoff’s essay

First Rakoff made the point that if there was no intentional fraud we should not scapegoat people and put them to jail. But on the other hand, if there was intentional fraud, then it’s a reflection on a dysfunctional justice system that nobody has gone to jail.

Then he examined that first possibility and found it unlikely, given that “… the Financial Crisis Inquiry Commission, in its final report, uses variants of the word “fraud” no fewer than 157 times in describing what led to the crisis…” In fact, fraud permeated at every level.

The Department of Justice (DOJ) has focused on explaining why nobody has gone to jail in spite of the existence of fraud. They have three reasons.

First, the DOJ claims it’s hard to prove intent for high-level management. But Rakoff demurs on this point, explaining that in cases of accounting fraud, “willful blindness” or “conscious disregard” is a well-established basis on which federal prosecutors have asked juries to infer intent.

Second, since many counterparties were “sophisticated,” it’s difficult to prove “reliance“. Again Rakoff demurs, pointing out that “In actuality, in a criminal fraud case the government is never required to prove—ever—that one party to a transaction relied on the word of another.”

Third, because of the “Too Big To Jail” problem, namely that prosecuting fraud would kill the economy. To this, Rakoff points out what that means in terms of class: that poor people can be prosecuted but the rich are protected.

Next, Rakoff says what he thinks is actually happening. First he discounts the revolving door: he thinks lawyers are thoroughly incentivized to make a name for themselves. Then what? He’s got three reasons.

Well, first, people were distracted. The FBI was distracted by terrorists, and the SEC was focused on Ponzi schemes and insider trading. The DOJ was inexperienced and the Southern District US Attorney’s Office was also focused on insider trading. And given the complexity and incentives, it’s hard for a given lawyer to decide to go with an MBS case instead of insider trading.

Second, the government had direct conflict in the fraud, given that the Fed and the regulators had deregulated everything in sight and then kept interest rates low to keep the mortgage machine going. They also meddled a lot during the crisis, deciding which failing bank should be taken over by whom. It made it hard for them to admit shit went wrong.

Finally, it’s because it’s now in vogue to prosecute corporations instead of people, but that really doesn’t work. Here’s Rakoff on this prosecutorial method:

Although it is supposedly justified because it prevents future crimes, I suggest that the future deterrent value of successfully prosecuting individuals far outweighs the prophylactic benefits of imposing internal compliance measures that are often little more than window-dressing. Just going after the company is also both technically and morally suspect. It is technically suspect because, under the law, you should not indict or threaten to indict a company unless you can prove beyond a reasonable doubt that some managerial agent of the company committed the alleged crime; and if you can prove that, why not indict the manager? And from a moral standpoint, punishing a company and its many innocent employees and shareholders for the crimes committed by some unprosecuted individuals seems contrary to elementary notions of moral responsibility.

And then his final conclusion:

So you don’t go after the companies, at least not criminally, because they are too big to jail; and you don’t go after the individuals, because that would involve the kind of years-long investigations that you no longer have the experience or the resources to pursue.

Comments

First, I am super grateful for Judge Rakoff’s essay, because as an experienced lawyer he has way more ammunition than I do to explain this stuff from the perspective of what is actually done in law. The “willful blindness” issue is particularly ridiculous. I’m glad to hear that courts have a way to deal with that problem, even if they aren’t using their tools against Jamie Dimon.

I am also grateful to hear him make the point that widespread fraud, unprosecuted, is not simply a theoretical issue. It exposes the dysfunctionality of our justice system and it exposes basic unfairness in society, where depending on how rich you are and how complicated your crime is, you can avoid going to jail. Personally, in the past few months I’ve gone from being angry at the bankers to being angry at the prosecutors.

Finally, I disagree with Rakoff on one point. Namely, his argument against the negative effect of the revolving door. His argument, I stipulate, only works for lawyers in a US Attorney’s office. I don’t think the average SEC lawyer or economist, or for that matter an employee at any captured regulator, has that much incentive to take on a big MBS case and be hard-assed. I think we would have seen more cases if that were true.

10 Worst things about Wall Street in 2013 (and 5 Silver Linings) #OWS

Written by the Alternative Banking group of Occupy Wall Street.

Compiling a list of the 10 Worst Wall Street Actions of 2013 should be easy–there are so many to choose from! The problem is, it often takes years to see which financial activities and innovations have been the most destructive and destabilizing. Therefore, the following should be considered merely a sample of the ways Wall Street has maneuvered, manipulated, defrauded and deceived us during the past year.

Bottom 10 things we found out about Wall Street in 2013

-

In Washington, It’s a Wash

One of the most obvious examples of Wall Street influence on Congress was HR 992 to roll back some of the derivatives restrictions on banks. The NY Times discovered that Citigroup had drafted most of the language, some of which was accepted almost word-for-word. The House passed it with bipartisan support. Meanwhile, bank lobbyists had excessive influence on the agencies writing and enforcing the Volcker rule. -

Still Too Big to Jail

The financial system in general, and the mammoth banks in particular, are still just too damn big. In 2013, JP Morgan Chase was the poster child for this problem, with its numerous legal problems, for which they set aside on the order of $28 billion dollars just to pay legal fees. The London Whale debacle, which involved Dimon lying to shareholders and Congress, showcased both how banks make their biggest money from pure speculation, and how they are enabled by lawmakers and regulators through their “Too Big To Fail” status. -

Banks Manipulate Commodities, Fed OKs It

Banks like JP Morgan Chase and Goldman Sachs have manipulated access to commodities such as aluminum and electricity in order to increase their profits. The Federal Reserve has permitted the biggest banks to postpone complying with such regulations as still exist to limit banks’ involvement in commodities, or to ignore them altogether. Minimal fines the banks have paid are simply the cost of doing business and are far outweighed by the money they’ve made. -

Zombie Foreclosures

The banks continued to exploit underwater homeowners. One of the worst abuses is called “zombie foreclosures” where the bank pretended to foreclose — evicting the owner — but then didn’t file legal papers. This allowed the banks to continue to rack up interest, fees and penalties because the homeowners, reasonably, stopped making payments because they thought the homes were no longer theirs. To add insult to injury, when the banks sent out checks to homeowners in restitution for past misdeeds, they bounced. -

Pillaging of Detroit

Detroit’s largest creditors, UBS and Bank of America, made it clear just how far they’re willing to go to collect on debts from highly-risky interest rate swap deals they made with Detroit’s leaders before the 2008 financial collapse: they’re coming for the art! Creditors, led by Detroit’s imposed “Emergency Manager” Kevyn Orr, sent Christie’s auction house to the Detroit Institute of Arts to valuate the works, which are all held tightly in public trust by the city. It still remains to be seen whether the approximately $900 million works – we think they’re priceless! – will be sold off to pay off debts or in some hostage deal to pay threatened but constitutionally-protected city worker pensions. -

Killing Credit Unions

According to MSN.com, credit unions offer low rates on loans, higher rates on savings, better credit cards deals, and lower fees. Perhaps because of these competitive benefits, the American Banking Association ran an ad campaign to revoke the tax exempt status for America’s credit unions. -

Court Evasion

There’s a familiar yet still outrageous lack of criminal prosecution for (pick your favorite settlement). But let’s concentrate on an exception that proved the rule, specifically what has been termed the “Bank of America/ Countrywide hustle”. Here Countrywide deliberately and desperately gamed underwriting standards to dump loans on Fannie and Freddie, and got caught. Worst of all, jury found defendants guilty in about 3 hours. If only more cases had been brought to trial: juries are chomping at the bit to find banks guilty. Which is probably why more weren’t. -

Never on Hold

U.S. Attorney General Eric Holder was an egregious case study in how Washington kowtows to Wall Street. When JPMorgan Chase wanted to settle their many legal difficulties, CEO Jamie Dimon had a private meeting with Holder to negotiate; the final settlement involved admission of illegal activity by JPMorgan but no criminal charges — just fines mainly paid by shareholders. Holder also admitted to Congress in March that the megabanks were too big to prosecute. While he later retracted the statement, his actions — never bringing criminal charges despite admitted criminal activities — speak louder than his words. -

Writing the Rules

The banks, among other corporations, pushed for the Trans Pacific Partnership (TPP) treaty that will greatly constrain efforts by the U.S. and other countries to regulate. For instance, it would prevent the imposition of a “Robin Hood Tax” on stock trading, it would roll back some of Dodd-Frank and prevent a return to Glass-Steagall. TPP would also forbid public banks such as the Bank of North Dakota or a return of the Post Office Bank. No wonder we aren’t hearing more details. -

Ongoing cultural confusion

AIG’s President and CEO Robert Benmosche compared criticism of AIG bonuses to lynchings in the Jim Crow South. Mistaking a papercut for a crucifixion is the inevitable delusion of a pampered and under-prosecuted criminal upper class.

5 Silver Linings

-

Occupy the SEC Gains Ground

Occupy the SEC‘s impact on the Volcker Rule (which originally aspired to banning proprietary trading and ownership of hedge funds by banks) could not be more evident. When the Volcker Rule was finalized in December, the hard work Occupy the SEC did writing a 325-page comment letter on paid off. The letter was cited 284 times by the regulators. In some cases, the final rule adopted their recommendations while in others the rule was modified in the direction of Occupy’s suggestions. -

Radical Eminent Domain

Richmond, California Mayor Gayle McLaughlin ignited a fury on Wall St and in Washington by employing an eminent domain threat to force intransigent banks to renegotiate – and reduce principal – for underwater homeowners. The move has sparked everything from lawsuits and threats of mortgage lenders leaving town to copycat actions in other underwater cities as far away as Irvington and Newark, New Jersey. Supporters of the promising tactic are calling it the Reverse Eminent Domain Movement and even Occupy 2.0. -

No Highchair for Larry

Larry Summers did not become the new Fed Chair in 2013. It was a close call but Larry Summers may finally have made too many obvious and ridiculous mistakes – deregulating financial derivatives to pave the way for the financial crisis, for one, and aiding criminal fraud in Russia for another – to be made, once again, one of the most powerful people in the world. -

Journalists Expose the Banks

Several journalists deserve extra praise this year for their coverage of Wall Street’s illegal and undemocratic behavior:: Matt Taibbi, Bill Moyers, Yves Smith, Gretchen Morgenson, the International Consortium of Investigative Journalism, ProPublica and Wikileaks. Taibbi alerted us to the HSBC settlement proving the drug war is a joke, Moyers highlighted how people can provoke change and, with Smith, exposed the dangers of the Trans-Pacific Partnership. Morgenson skewered payday lending and many other unsavory financial practices. The International Consortium of Investigative Journalism and WIkileaks exposed documents that the banks want to keep secret — for good reason — about enormous amounts held off-shore and TPP drafts.. -

Occupy Finance and Strike Debt

-

The OWS Alternative Banking Working group released Occupy Finance, a 100-page book explaining the financial crisis in layman’s terms on the second anniversary of Occupy, and supplies of the book were quickly exhausted (a new printing has been ordered for January 2014).

-

In the past two months alone, Strike Debt’s Rolling Jubilee has collected and abolished $14.7 million in debt, as a means of raising awareness about the personal debt crisis, and a step towards building a debt resistance movement.