Is Hyperinflation Coming?

This is a guest post by Aise O’Neil.

Inflation is growing out of control, or so we are told. Tucker Carlson recently said, “we wound up with frightening levels of inflation,” blaming such levels on the policies of the Biden administration. Glenn Beck published a youtube video entitled “How to Prepare for Hyperinflation in America.”

But it’s not just rightwing cranks who are panicking about inflation. Leading industrialists, like Warren Buffet, are concerned too. For that matter, financiers in the bond market are betting on high inflation. The 5-year breakeven inflation rate, a measure of expected inflation priced into the bond market recently hit a new high for the past decade: 2.72%. At the same time, the cpi index in April 2021, was 4.16% higher than it was in April 2020. That’s another record for a decade. And it’s likely that when this month’s CPI index comes out it will show an even higher percentage change from a year prior.

But even though CPI inflation is hitting records (and so is PCE inflation), there are three reasons to believe the numbers are misleading. Firstly, one has to consider factors which are making usual inflation indicators overstate the actual inflation rate. Second, one should consider better methods of tracking long term inflation trends, like median inflation. Thirdly, economic theory has something to say.

Reason #1: Normal Measures of Inflation Are Giving False Signals

There are two main indices used to track overall inflation that ordinary people might hear about. Both of them use year-on-year measures, which skew readings about a year after something weird happens.

Their names are CPI (“consumer price index”) and the PCE index (“Personal Consumption Expenditures Index”). Each month the government publishes a CPI and a PCE index for last month. We can measure how much prices have changed by looking at the differences in indexes. If the CPI is growing at an approximate rate of 2% a year, we could say CPI inflation is 2%.

When we hear about inflation rates, we normally are hearing about the “annual” inflation which is the % change in an index from a month to the same month next year. So we hear that “inflation was 4.16% in April 2021” we should think that prices are estimated to have risen about 4.16% from April 2020 to April 2021. Essentially, annual inflation is not a data point but a cumulative 12-month sum of data points. When that number is higher than it was last month, that could tell us about what happened recently in terms of the CPI/PCE index, or it could tell us about what happened to the CPI/PCE index last year. For instance, from March to April 2021, the annual CPI inflation went from 2.62% to 4.16%. This is because from March to April 2021 the CPI went up .76%; but from March to April 2020 it fell .7%.

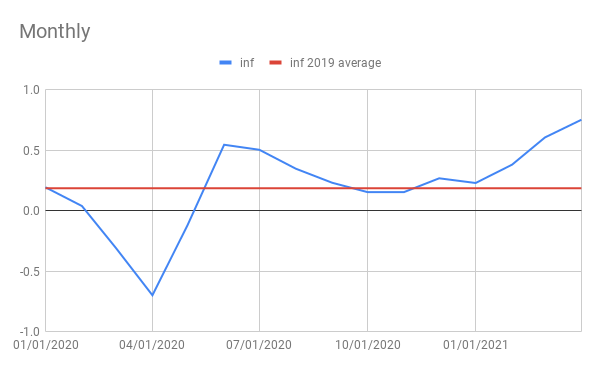

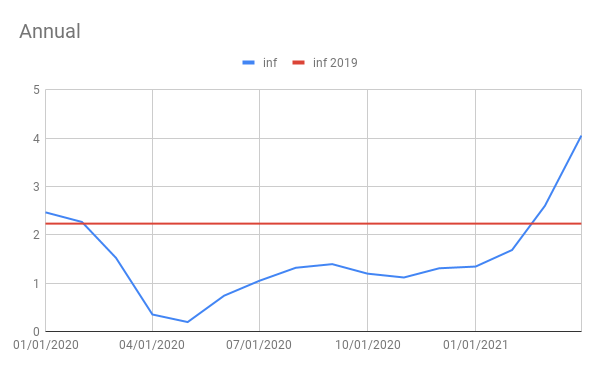

If price changes of plus or minus .7% a month seem kind of volatile, that’s because they are. Volatility is particularly high in both the CPI and PCE index at the moment because of the effects the shutdown, it’s aftershock and reopening have been having on prices. The graph to the bottom left shows monthly changes in the CPI, measured in log-%. The data is seasonally adjusted by the government so seasonal factors have little to do with the behavior of the data. The blue line is the data and the red line is the average monthly inflation rate for December 2018 to December 2019. On the bottom right, one can see data on annual inflation measured in log-% changes to the cpi. The blue line is still the data and the red line is the inflation rate from December of 2018 to December of 2019.

The point of the red line in both graphs is to give a sense of normal levels of inflation. The purpose of a monthly and annual inflation graph side by side is to show that monthly inflation tells some information that annual inflation does not. Both of these graphs are in terms of CPI data, but PCE index data would give similar results.

In terms of monthly inflation, what we saw at the early part of 2020 was extremely low, even negative inflation. This was a temporary phenomenon which occurred as prices for certain goods crashed at the beginning of the shutdown. For instance, when people stopped driving as much oil prices crashed. A few months later and prices slightly rebounded as companies like oil rigs cut back production. Afterwards, monthly inflation seemed to be at normal levels until now where the rollout of the vaccine is allowing for the economy to open up again.

What effect is this having on annual inflation? For about a year after the shutdown, annual inflation gave low readings because the shutdown crash in prices occured over the 1 year time frame to estimate annual inflation. Right now, two things are happening; 1) The volatile and temporary weak monthly inflation readings are falling out of the one year average, and 2) Volatile and temporarily strong inflation readings are coming into the average. This is going to mean an appearance of accelerating inflation.

Additionally, when the current month’s CPI comes out on June 10th, 1 year inflation will cover the rebound in prices shortly after the shutdown along with the spike in prices experienced during the re-opening. While prices did grow strongly from May to August of 2020, that was an aftershock of declining prices from February to May of 2020. The next annual inflation figure will cover the aftershock of the shutdown price decline but not the price decline itself, while at the same time it will include price growth we are experiencing during the re-opening. If prices grow from April to May 2021 as much as they did from March to April, then annual CPI inflation could be as high as 5.05%. This will be scary to some if they don’t understand that it is just temporary shocks.

Reason #2: Better Long-term Inflation Measures

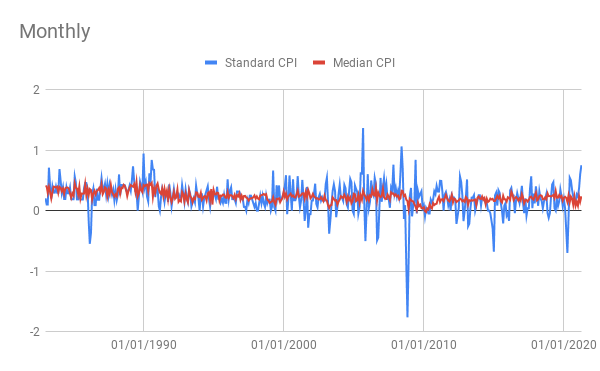

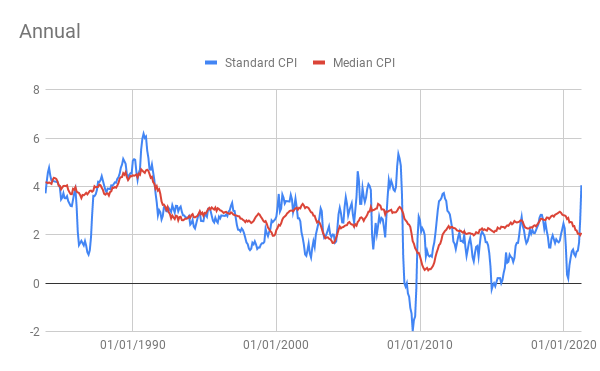

It should be clear now that CPI and PCE index data often has to be scrutinized and can be quite volatile. For that reason many economists attempt to find less volatile measures of inflation. The Cleveland Branch of the Federal Reserve has developed multiple ways to measure underlying trends in inflation. They have developed 2 very good ones: Median CPI and Median PCE inflation. While standard PCE and CPI inflation measure inflation through finding changes to the average levels of prices in an index (it’s slightly more complicated for PCE); median inflation finds the weighted median change of prices in an index. The graphs below compare historical standard and median inflation (in log-% terms) and show how median CPI inflation is more stable and reliable and is not indicating a risk of rising inflation.

Reason #3: Economic Theory

Economic theory tells us that inflation is determined by three things. The first is shocks of the forms I’ve been explaining so far (like the shutdown causing commodity prices to drop). Overall, these impacts will be short-lived and average out to 0 in the long term.

The second relates to how inflation declines during recessions and grows during expansions. If due to a lack of strong spending, a lot of resources like land labor and capital go unused, the prices for those inputs will decline lowering production cost. This can be observed in the graphs above which show a decline in inflation following the early 90s recession, a slight dip following the 2002-2003 recession and a large dip following the great recession of 2008. Recently annual inflation has dipped down again according to median inflation. This is because we have entered another recession.

Thirdly, embedded inflation is a very important long-term determinant of inflation. Oftentimes, economic actors set prices in response to or in anticipation of inflation which then determines inflation. Hence, factors like catch-up inflation and expected inflation are useful in modeling inflation and are thought to give it a good deal of inertia.

In conclusion, what theory tells us is that it is unlikely we will go from inflation persistently undershooting 2% PCE for years to hyperinflation. It is also probably a good idea for economic policymakers to ignore transitory shocks to the best extent possible.

Finally, the most important question to determine where inflation will be headed when the virus is dealt with is: How high will unemployment be? If we cannot ensure a full, rapid recovery to this economic crisis, and likely we can’t, then inflation will probably be heading down, not up.

Conclusion

Overall the conclusion from this is one should not personally be too worried about hyperinflation. Furthermore, one should not pay too much attention to the ideas of Tucker Carlson and Glenn Beck (that’s a more general rule).

Finally, if one wants to make some money, one should realize that betting on rising inflation is a winning bet on wall street right now. It will likely continue to be until June 10th where the next CPI report comes out showing a yearly inflation rate in the vicinity of 4.5% to 5%. However, this high inflation is illusory and eventually wall street will catch on.

Good article – Thank you ________________________________

LikeLiked by 1 person

Aise,

Very nice column and good general rule. FWIW, I agree with your conclusion and salute you for not mentioning monetarism even to refute its claims.

J

LikeLiked by 1 person

You said rightwing cranks who are panicking about inflation………..What about LEFTWING CRANKS ..like Biden and AOC…….what are they saying…….

LikeLiked by 1 person

Biden is not left wing.

Haven’t heard what, if anything, either he or AOC have said about inflation but I’d be surprised if either were raising alarms about it.

LikeLiked by 1 person

Folks need to understand how rare hyperinflation is, and that it tends to be due to an economy’s severally crippled productive capacity (see post WWI Germany, and more recently, Zimbabwe and Venezuela), coupled with unmanageable debt in foreign-denominated currency (see, in particular, post WWI Germany and the more recent Venezuela).

So, absolutely, it’s very, very, very unlikely the U.S. will go from persistent low inflation to hyperinflation.

LikeLiked by 2 people

Very inspired by your work and especially your background!

I currently work in the Financial Services industry. I am starting a social justice themed extension of the financial services industry that I am sure AI will complicate. I’d love to tell you more. As a person who previously worked in the Financial Services industry I am sure that once I inform you of the organization and strategy you will understand how AI will complicate our goal and that you would know how we can overcome it.

Would you be open for a call or Zoom to discuss further?

LikeLiked by 1 person

It seems to me that inflation cannot be properly described as a single number. Typically price of different categories of things change at different rates. In recent years, the government has been supplying the rich with a lot of funny money through artificially depressed interest rates, among other things. As a result, rich people’s asset prices like stocks, real estate, and collectibles have been rising much faster than the kind of goods and services that proles buy. As long as the funny money is sent to the upper realm, there is not a lot of money in the lower realm; so huge amounts of money (or quote-money-unquote) can be produced without causing inflation in the lower realm. There is, however, a dangerous crossover point, and that is real estate, because even the proles think they need a place to live, and have to enter the real estate market to rent or buy. This situation can break down, as it started to in 2005-2009. One could see the debacle coming in that case; it is hard to figure what is going to happen now. Since much of the money which has been printed up for the rich is actually abstract or theoretical, it can disappear very suddenly, so the outcome will not necessarily be an inflation.

LikeLiked by 1 person

Your reasons make sense but I don’t see how your reasons lead to your conclusion. Your reasons are based on retrospective numbers, while your conclusion is forward looking. Not suggesting there will be hyperinflation or even sustained inflation, but I don’t believe the reasons lead to that conclusion.

LikeLiked by 1 person

It seems to me that after the extended débâcle of 2005-2009, part of the ‘recovery’ was to put things back where they had been, for example to reinflate rich people’s assets, I guess in the hope that some of the money would leak out and animate the proles’ economy — not sure about that. The difference between previous inflation and the inflation-if-so-to-be is that old-time inflation was generated by having a lot of permanent money around in various forms, whereas today rich people’s assets can disappear in the twinkling of an eye because people _and_machines_ stop believing in it. So not only may vigorous inflation be the outcome, but alternatively it may be very rapid deflation as usable money vanishes. The further we get from money representing anything like labor, goods, or the prospect of obtaining them, the more unstable the situation.

LikeLiked by 1 person

I always thought hyperinflation was the complete opposite of regular inflation.

My grandfather told me about his experience of inflation being times when lots of people are investing their money. People are looking for a better rate of return over inflation to get more money in their pockets.

He described his personal experience with hyperinflation, as a time when everyone wanted to get rid of money. The less money you had meant the less you were loosing in your pocket.

My grandfather said these experiences he has were the exact opposites of each other in every way imaginable. The only similarity being the suffix of -flation. This conflation of totally opposing phenomena seems to have completely skewed the conclusion of this article.

LikeLiked by 1 person