Bethany McLean’s Shaky Ground: the strange saga of the U.S. mortgage giants

In preparation for an all-housing special on this week’s Slate Money podcast, I just finished Bethany McLean’s new book, Shaky Ground: the strange saga of the U.S. mortgage giants. It’s a quick read and not an expensive book, well worth the money for the amount of information packed into the pages.

Namely, the book tells the story of Fannie Mae and Freddie Mac, and more generally the story of U.S. governmental involvement in the mortgage and housing markets, starting soon after the Great Depression. It’s fascinating stuff, and also completely baffling as well, partly because it’s so deeply entwined with politics, so there’s really not a lot of rational logic attached to it. Here are a few interesting things I learned, or was reminded of, while reading the book:

- When the shit hit the fan in 2008, Fannie and Freddie were put into conservatorships, rather than nationalized (which would have gotten rid of shareholders), but really the only reason (or at least one big reason) they weren’t nationalized was because if they had been, their debts would have been added to the national debt, and the accounting would have looked bad. This is the same reason they were originally made private.

- They were also forced to assume extremely heavy losses, which made their accounting look incredibly bad. That may have been a political move by people who hated them, but it also may have just been pessimistic guesses as to how bad the mortgages they had were.

- In any case, they’ve recently been quite profitable, but all their profit has been siphoned off to the Treasury, in spite of the fact that they are technically still supposed to serve shareholders.

- As a result a bunch of hedge funds, who generally speaking bought shares at very low prices, are suing because they think that profit belongs to them. They have not done well in court as of now.

- Stepping back a bit, the whole reason Fannie and Freddie exist is so that they can insure mortgages, so that more mortgages are given out on better terms, so that every American can “live the American dream” of homeownership. Speaking as a non-homeowner, I think this is crap. Oh, and also, most of the loans in the mid-2000’s were for refinancing and for second homes, so it wasn’t like that was actually happening.

- People still “hate” Fannie and Freddie but nobody seems to have a plan to transition to a system whereby the government isn’t the final backstop for mortgages. It’s like they just want to get rid of these political entities, which did behave extremely badly in the late 1990’s, giving their executives outrageous salaries and wielding ridiculous political sway via favors.

- In any case, the combination of the cheap backstop represented by Fannie and Freddie, in addition to the mortgage tax deduction represents a FUCKTON of government support for homeownership, and also raises the prices of houses by an extreme amount.

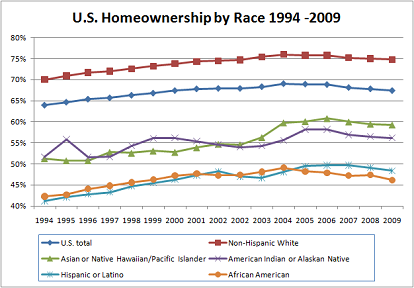

- In spite of this all, homeownership as a percentage of households is way down, although that can be misleading, and is particularly low for minorities:

- There is no current plan to get rid of Fannie and Freddie, or to change their status from conservatorship. Moreover, the current system whereby all their profit goes to Treasury leaves them with no cushion, so should another economic shock happen to them, there’s really no telling what’ll happen.

After reading this book, I can only conclude that it’s time to strengthen renter laws.

{kind=link}

I too recommend her text. It really is a fast read, and as usual, she provides an exceptionally understandable narrative to what most would otherwise consider a dry story matter.

LikeLike

Also, I should add for those interested, as per “Mr Hedge Fund Goes to Washington,” there’s a lot of source material that can be found online in addition to the (relatively) short further reading section. A group of participants have clearly made lottery tickets bets on the backs of Berkowitz, Ackman et al, and so an extent of the research materials have made their way to easy access.

LikeLike

IIRC, there were some reasonable plans put forward to wind-down these two GSEs and allow a new structure to emerge in the mortgage market. I’m not sure why these lost traction, maybe because there have been more exciting political fights in DC that have taken priority?

To point 9, probably the same thing that happened before: US Treasury will step in as before.

Also, another important point about the US mortgage market is that it used to be a key transmission channel for monetary policy (Federal Reserve rates) into the economy. When the Fed target is at 0, it is unclear whether mortgages continue to play this role. Views seem to break along dogmatic lines, but I’ve spent a decent amount of time on this and think the case isn’t convincing or clear on either side.

Finally, don’t forget about the tax incentives for levered home ownership (mortgage interest deduction). I know this has also been discussed before on this blog.

LikeLike