Dallas Fed’s Richard Fisher talks TBTF on EconTalk (#OWS)

Yesterday Russ Roberts had Dallas Federal Reserve President Richard Fisher as his guest on his podcast EconTalk to talk about Too-Big-To-Fail (TBTF) banks and the Fed’s monetary policy. It was a fantastic discussion and I’m grateful to Roberts for continuing to discuss this important and nonpartisan issue.

We in Alt Banking have been impressed by Fisher’s stance on TBTF and have thought about trying to get him to come visit us to talk, so this was a great opportunity to get a preview of what he’d likely say if he ever made it over. Given that he’s an active central banker, he’s refreshingly open and honest about stuff, even if every now and then he deliberately makes it seem like everything that happened was a mistake rather than a criminal act.

Fisher and Roberts on TBTF

You should listen to the entire podcast, it’s about an hour long but well worth the time. I will submit a short summary of their conversation here:

- First they discuss the problem of TBTF banks, that instead of failing, large banks were merged into even larger banks during the crisis, and now we have institutions that are too big to manage and are being backed by an implicit government guarantee that the Dodd-Frank regulation isn’t removing.

- Next, the discuss a takeaway in terms of community banks. Is it a problem that it’s not a level playing field for community banks? Or is it primarily a problem that any bank that should fail is being propped up?

- Roberts makes the point that he doesn’t care so much that the system isn’t fair, he cares only that this banking system isn’t effective. If the threat is that France might overtake us in an ineffective field such as finance, then so be it.

- Then Fisher started talking solutions. He has a two-part plan. The first part is to make very explicit which parts of a bank have deposit insurance and access to the Fed window, namely only the commercial bank part that accepts deposits, not any special investment vehicles or insurance subsidiaries etc.

- The second part is to hold a ritual signing of a contract among every bank customer, creditor, investor, and counter-party (but not depositor!) which states that they know their investment is not protected by a government guaranteed. Roberts suggested this might be done in a public ceremony and include a statement that people will refuse government support, so that there will be an added element of public shaming if people go back on this promise. Here’s an example of such a covenant available at the Dallas Fed webpage:

- Next Roberts pushes back: the institutions that got bailed out in 2008 didn’t have insurance, so why will this work?

- To this Fisher acknowledges that it’s all about beliefs and expectations of market participants, but he thinks that the simplicity of this, as well as the signing of the covenant, might be convincing enough. By contrast he mentions that the current system, where we have a Financial Stability Oversight Council that decides which institutions need closing, has a very low probability of working. In particular, Fisher points out that it will take 24 million man hours to simply interpret current law to break down a bank.

- Roberts then asks, what about larger capitalization requirements of banks, or capping the size of the banks? Turns out that Fisher wants to minimize government intervention and maximize “market driven approaches.” He’s a real free market lover. He also says that, in the case of a liquidity run, capital cushions, even big ones, will be insufficient if you’re dependent on short-term funding.

- One last thing. They both mention that TBTF will only be solved when a president wants it to be solved. But they also both agree that no politician wants to lose the money they get from Wall Street lobbyists.

- Next, on to monetary policy. Fisher points out that the dual mandate of the Fed is supposed to focus on long term issues, and that QE’s policy of cornering the market on treasuries and mortgage-backed solutions (MBS) is both unsustainable and doesn’t work well in a long term way.

- Fisher mentions that the Fed has made money on its enormous, $4.2 trillion portfolio, to the tune of $300 billion in the past few years, but on the other hand that’s partly because interest rates are so low. What will happen when that changes?

- He’s worried long-term about inflation, since the Fed is basically printing money, which is being stored by the banks (and hedge funds and private equity) and not lent out, at least for now.

- Finally, and this is where I care the most, this is a policy that benefits rich people and doesn’t do much at all for the rest of Americans. The balance sheets of big US companies look great now because of QE, but they largely don’t hire people because they’ve realized they don’t really need to – they’ve harnessed IT. So actually there’s less need for credit in the system altogether. Conclusion: we should reduce QE sooner rather than later.

A couple of comments

I’m not as much of a fan of “free market solutions” as Fisher and Roberts. In particular I don’t think the influence of the Fed is going to be immediately forgotten, even if we scale it down, and the bailouts will take a while to forget as well. In other words I don’t think it will be realistic to think of our system as a free market any time soon. Plus I believe in good strong rules for the market to work well.

Having said that, I love the idea of implementing these two steps to end TBTF and then seeing how well they work. By all means protect only deposits and let everyone else risk their money. See if we can at least make a dent in the implicit government subsidy.

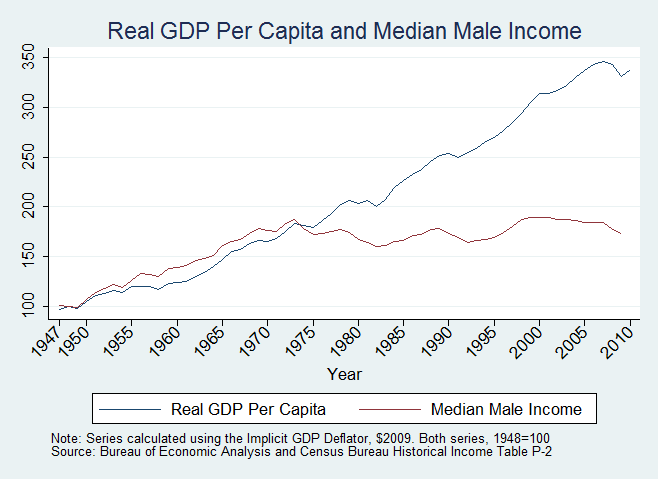

In terms of QE, there’s something to be said for everyone suffering together, and this policy is the opposite of that. Right now we see the GDP decoupled from the fate of the working man, and QE is a primary cause of that decoupling. Even so, we still use GDP as proxy for growth and success for our economy, even though the benefits are almost exclusively going to rich people. Here’s a chart showing what I mean, which I got here:

So in other words I’m basically agreeing with Fisher, except I’m a little more impatient for this craziness to end. If we’re going to spend $85 billion a month to save our economy, how about making state college tuition go down with that money?

I am not sure if I follow his argument. If a big bank has an investment vehicle/fund which starts to go under what would prevent it from making a loan to bail out said vehicle/fund?

LikeLike

I think you have QE backwards. As a citizen of the Eurozone with a central bank that refuses to do anything remotely like QE I dearly wish I was afflicted by a central bank like the Fed that was willing to “harm” me with lots of QE.

LikeLike

i’m ready for guaranteed income. let’s quantitatively ease everyone. you can’t live anywhere on this planet (rare exceptions) with no money, so give everyone some money. every american could carry something equivalent to an ebt card that gets for example $200 a month. it’s better than qe! this is closer to how money should work anyway, as a value exchange not a value store.

LikeLike