Archive

AAPOR Big Data Report

I was recently part of a task force for understanding the practices of “big data” from the perspective of the American Association for Public Opinion Research (AAPOR), which is an organization that promotes good standards for studying public opinion.

So for example, AAPOR has a code of ethics for how to track public opinion, and a set of understood methodologies for correctly using surveys. They involved themselves last year when they criticized the New York Times and CBS for releasing the results of a nationwide poll on Senate races where the opt-in survey method had “little grounding in theory” and for a lack of transparency.

But here’s the thing, the biggest problem facing the world of public opinion research isn’t that online opt-in polls, but rather the temptation to troll twitter to “see what people are thinking.” And that’s exactly what’s happening, in large part because it’s cheaper. Thus the AAPOR Big Data Report that I helped with.

I think we did a decent job of describing some of the intrinsic difficulties with using big data, specifically around quality control issues, and for that reason I recommend this report to anyone entering the field, or even people already in the field who haven’t thought through this stuff. If you don’t have time to read the full report, here are our recommendations:

1. Surveys and Big Data are complementary data sources not competing data sources.

There are differences between the approaches, but this should be seen as an advantage rather than a disadvantage. Research is about answering questions, and one way to answer questions is to start utilizing all information available. The availability of Big Data to support research provides a new way to approach old questions as well as an ability to address some new questions that in the past were out of reach. However, the findings that are generated based on Big Data inevitably generate more questions, and some of those questions tend to be best addressed by traditional survey research methods.

2. AAPOR should develop standards for the use of Big Data in survey research when more knowledge has been accumulated.

Using Big Data in statistically valid ways is a challenge. One common misconception is the belief that volume of data can compensate for any other deficiency in the data. AAPOR should develop standards of disclosure and transparency when using Big Data in survey research. AAPOR’s transparency initiative is a good role model that should be extended to other data sources besides surveys.

3. AAPOR should start working with the private sector and other professional organizations to educate its members on Big Data.

The current pace of the Big Data development in itself is a challenge. It is very difficult to keep up with the research and development in the Big Data area. Research on new technology tends to become outdated very fast. There is currently insufficient capacity in the AAPOR community. AAPOR should tap other professional associations, such as the American Statistical Association and the Association for Computing Machinery, to help understand these issues and provide training for other AAPOR members and non-members.

4. AAPOR should inform the public of the risks and benefits of Big Data.

Most users of digital services are unaware of the fact that data formed out of their digital behavior may be reused for other purposes, for both public and private good. AAPOR should be active in public debates and provide training for journalists to improve data-driven journalism. AAPOR should also update its Code of Professional Ethics and Practice to include the collection of digital data outside of surveys. It should work with Institutional Review Boards to facilitate the research use of such data in an ethical fashion.

5. AAPOR should help remove the barrier associated with different uses of terminology.

Effective use of Big Data usually requires a multidisciplinary team consisting of e.g., a domain expert, a researcher, a computer scientist, and a system administrator. Because of the interdisciplinary nature of Big Data, there are many concepts and terms that are defined differently by people with different backgrounds. AAPOR should help remove this barrier by informing its community about the different uses of terminology. Short courses and webinars are successful instruments that AAPOR can use to accomplish this task.

6. AAPOR should take a leading role in working with federal agencies in developing a necessary infrastructure for the use of Big Data in survey research.

Data ownership is not well defined and there is no clear legal framework for the collection and subsequent use of Big Data. There is a need for public-private partnerships to ensure data access and reproducibility. The Office of Management and Budget (OMB) is very much involved in federal surveys since they develop guidelines for those and research funded by government should follow these guidelines. It is important that AAPOR work together with federal statistical agencies on Big Data issues and build capacity in this field. AAPOR’s involvement could include the creation or propagation of shared cloud computing resources

When non-mathematicians judge the math major

I was going to blog about some serious stuff this morning but then someone (specifically, my cousin Anne Hall) sent me this socialist and feminist redo of 50 Shades, which made me forget everything else. Favorite line:

“You need to go away and sit and think about commodity fetishism and the compensation of emotional labour. Also your obvious issues with women. By the way, how did you get this number?”

Oh wait, I guess I still have 18 minutes to say something.

So yesterday my Facebook page lit up with mathematicians discussing this USA Today list of top 10 colleges for math majors:

- HARVEY MUDD COLLEGE: CLAREMONT, CALIF.

- COLORADO SCHOOL OF MINES: GOLDEN, COLO.

- MASSACHUSETTS INSTITUTE OF TECHNOLOGY: CAMBRIDGE, MASS.

- UNIVERSITY OF CALIFORNIA – LOS ANGELES

- CARNEGIE MELLON UNIVERSITY: PITTSBURGH, PA.

- UNIVERSITY OF CHICAGO: CHICAGO

- CORNELL UNIVERSITY: ITHACA, N.Y.

- WASHINGTON UNIVERSITY IN ST. LOUIS: SAINT LOUIS, MO.

- UNIVERSITY OF PENNSYLVANIA: PHILADELPHIA

- CALIFORNIA INSTITUTE OF TECHNOLOGY: PASADENA, CALIF.

These are some fine schools, but not at all the typical list one would consider. That makes you wonder, how does one decide where the best place is for a math major? Scanning this list, I have no idea, and it certainly doesn’t correspond to the places that produce the most research mathematicians. But maybe that’s not what USA Today cares about.

In fact, it isn’t. The methodology is outlined here, and the “full methodology,” which doesn’t actually explain much, is here. But as for figuring out what is actually valued, we get some glimpse:

| Factor | Weighting | Description |

| Graduate Earnings | ||

| Early-Career Salary | High | Average salary of bachelors degree graduates from the college in that major with 0-5 years of experience. |

| Mid-Career Salary | Med | Average salary of bachelors degree graduates from the college in that major with 10+ years of experience. |

| Major Focus | ||

| Major Focus % | Med | Percentage of students at the college studying that major. |

| Bachelors Degree Market Share | Med | Percentage of all U.S. bachelors degree graduates in that major represented at that college. |

| Masters Degree Market Share | Low | Percentage of all U.S. masters degree graduates in that major represented at that college. |

| Doctoral Degree Market Share | Low | Percentage of all U.S. doctoral degree graduates in that major represented at that college. |

| Related Major Concentration | ||

| Related Major Focus (mPower Index) | Med | Measure of how much all the other majors at the college are related to the major. |

| Related Major Breadth | Low | Number of closely related majors offered at the college. |

| Accreditation | ||

| Relevant Program Specific Accreditation | Med | Whether or not the major is accredited by a relevant accrediting body (ie. ABET for engineering). If no obvious accrediting body for a major, this factor is ignored for that major’s rankings. |

| Overall College Quality | ||

| Best Colleges Ranking | High | The College Factual Best Colleges ranking, a measure of overall college quality. |

So here’s the thing. We mathematicians think that money doesn’t buy happiness, and we don’t care so much about early career salaries. That’s the first thing that sticks out.

But also, and I’d say just as importantly, we do care about the extent to which the average undergraduate math major is exposed to research mathematics, which is why we care much more deeply about the “doctoral degree market share” than this ranking does. I mean, I guess to the non-expert, it makes sense to care way more about the undergraduate focus of a college for judging the quality of an undergrad math major, but it all depends on what you want to have happen next.

I’m enjoying how different this list is from the typical inside baseball list. I don’t even know who it’s for, if anyone, but as a thought experiment it’s interesting to imagine what would happen if suddenly all the math departments everywhere suddenly tried to game this particular system, like colleges do with the US News ranking.

So, for example, we’d throw out pure math majors altogether in order to focus our attention on applied math majors that will make loads of money out of college. We’d also compete for students against other majors, something very few math departments actually do. It would be interesting, but I’m not holding my breath.

Things I’m reading

Really into writing right now but I’d still like to share my reading list with y’all.

- The review of 50 Shades I wish I’d written (hat tip Chris Wiggins). I still can’t decide whether the net effect of the film is bad, because the characters are so terribly stereotypical and stalkerish, or good, because it at least forces people to ask the question, what do I desire and how is that different from other people’s desires.

- Alexis Goldstein’s newest piece in Medium.com about the newest pawn in the financial lobbyist’s chess set, community banks.

- Remember SketchFactor? Well now there’s PlaceToLive (hat tip Jordan Ellenberg).

- I’m researching the toxic industry that is for-profit colleges. On the other hand, the Washington Post seems to be shilling for that same industry: here, here, and here (hat tip Auros Harman).

- If you’re a listener, try this interview with Edward Baptist, author of The Half Has Never Been Told: Slavery and the Making of American Capitalism. I’ve heard great things about this interview and its explanation of the earlier versions of “financial innovations” that directly involved slaves. This piece and many many more can be found on the Alt Banking website.

Aunt Pythia’s advice: 50 Shades edition

Readers! Dearest readers! Welcome! And a very warm welcome as well to anyone coming from the Slate Money podcast “Exotic Fantasies” edition, where Aunt Pythia was delighted to be featured this week.

Aunt Pythia is so very happy to welcome you (and your Inner Goddesses) onto the bus today. Please enter single file, find an empty seat, or sit on someone’s lap, or lie across a series of laps, and then apply the “restraints” (otherwise known as seat belts) to yourself and others. I’ll wait. Oh, and before Aunt Pythia forgets, please sign this consent form before we begin. Yes, that’s what I said. It’s an unusual column today, people.

Because, dear readers, although Aunt Pythia does not believe in Valentine’s Day in general, she is making an exception this year for the opening weekend of 50 Shades of Grey, simply because it has created an extraordinary opportunity to talk about sex nonstop for a week:

The movie is entirely sold out all day today, so I’m going first thing tomorrow morning, kind of like church.

After you read the column, but before you go to the movie, please:

ask Aunt Pythia a question at the bottom of the page!

By the way, if you don’t know what the hell Aunt Pythia is talking about, go here for past advice columns and here for an explanation of the name Pythia.

——

Dear Aunt Pythia,

Now that you’ve been out of the ivory tower for a few years, do you have any particular advice for smart math phd’s who want to leave academia?

I’m asking because one of my students is more interested in having a permanent job after her Ph.D. than doing a research post doc and moving several times. She’s a decent programmer, but with little formal training beyond a few classes and a lot of experience with Magma.

Best,

Cutie-Patootie

——

Dear Cutie-Patootie,

Sounds like your students is not psyched for the nomadic, monastic, and frugal lifestyle of the mathematician. I get that.

And here’s the thing, I wrote Doing Data Science for people like her. She should take a look and see if that is her style. And if yes, she should learn python and do a few data projects and exhibit them online.

If not, she should take the following quiz:

- Are you boring?

- Are you evil?

If she said “yes” to #1, she might consider actuarial math. If she said “yes” to #2, she should think finance. If she said “no” to both, she should consider moving to Canada.

Good luck!

Aunt Pythia

——

Dear Aunt Pythia,

Couldn’t tolerate the thought of that picture getting posted again next week, so. . .

What are your suggestions for getting better at sex? I’m sure open communication, mutual exploration and play will be at the top of your standard list. Problem is that my partner doesn’t want to do any of that. I think the reasons are a mix of shame and an idealized romantic notion that this should be effortlessly perfect.

No More Bouncy Castle Genitalia Pics

Dear NMBCGP,

Do you mean this picture?

I could post this every week and die a happy woman

As to your question, here’s what I’ve noticed. A lot of people complain about their sex life and when I ask them whether they’ve tried various things, they tell me their partner “doesn’t want that.” But when I ask whether they’ve asked their partner, explicitly, about that, they admit they haven’t. It makes me wonder if their partner also goes around saying exactly the same thing.

The thing about open communication is that having it clears up these kinds of mutual misunderstandings. It’s worth double checking sometimes, in other words.

And if you do double check, and she agrees she doesn’t like open communication, mutual exploration, and play, then I’d say find a new girlfriend.

Good luck!

Aunt Pythia

——

Hello Aunt Pythia,

So this is a tricky question to phrase, or to ask at all, but I will give it a try.

I met my girlfriend online and for the first two years, all of our interactions were carried out that way. All of them. There was something I could do that she liked, and it IS kinda fun, once in a while. I didn’t know it was rare, but she assured me it is, and that it excited her enormously.

Now we are together, and of course she wants me to do it ‘in the flesh’. I worried that it wouldn’t be nearly such a turn-on for her as it was online … but she absolutely loved it. Now she wants me to do it every time, and even while I’m inside her. As I’ve said … I enjoy it sometimes … but not every time, plus I am a bit worried about the hygiene element of the whole ‘inside’ aspect of it.

I don’t want this to be something that dents our relationship, but nor do I want it to happen every time. I know it’s stupid, but occasionally I even think this might have been what brought her to me, and in those moments, I can’t countenance NOT doing it for her, in case I lose her. Most of the time I know that last sentence isn’t true, but that 1% of the time when I don’t rather carves me up.

Dear Aunt Pythia – can you help me retain my lovely girlfriend, and also help us both to get the maximum enjoyment from sex?

Hopefully yours,

Finding Our Unusual Net Techniques Aren’t Intimate Nirvanas

Dear FOUNTAIN,

First of all, amazing sign-off. Possibly the best one ever.

Next, it’s not clear if you’ve ever expressed to your girlfriend that you’d like to try sex without this. For all she knows, you might like this as much as she does. So the first thing to do is to talk to her about how it would be nice to have sex without this element once in a while. She might be fine with that!

Third, it’s not ok for someone to insist on something, anything, to happen every time, unless both people want it. It borders on abusive, in fact. So keep in mind it’s totally OK to tell her what you need. Or another thing you might do is discover a kink of your own and agree to alternate between your two kinks, thus naturally creating balance.

Finally, here’s what I’d actually do if I were you. I would just “forget how to” do that thing that you do once or twice and see what happens and see what conversations emerge, if any.

After all, penises are mysterious things that women don’t have direct experience with and thus don’t understand. They don’t always do what you want them to do (we all know that from our experiences in 7th grade!), with all those myriad valves and fittings. It’s perfectly reasonable to believe that this specific thing sometimes just doesn’t work. Not that I want you to be consistently devious, but try it out and see whether the sex can be good for both of you.

Love,

Aunt Pythia

——

Aunt Pythia,

You seem to have a great and helpful perspective on sex. I’d love to ask a sex question or three. And you seem desperate for sex questions. But I’m afraid that the closest I can come right now is more of a disappointingly meta sex question.

In particular, how can people safely ask their sex questions? Aren’t they thinking ahead and afraid that their letter will be immortalized online and someone, someday, will read it and figure out who wrote it? Do people play tricks like reversing the genders? Would that really be convincing, like “I can’t get my wife to help with the dishes. Can you help?” Most of the time gender issues are raised that would not allow this.

I think part of what makes your answers great is that you don’t always insist on the idea that one must necessarily share with one’s partner anything one might think, fantasize about, etc. Thus the worry.

Perhaps this has brought me closer to a sex question: what is your general guidance about when one should and should not share thoughts and fantasies about sex with a partner? That seems safe enough for starters.

ME Think Ahead

Dear META,

First of all, I’d advice you to stop worrying so much. Everyone thinks about sex all the time, so by the pigeon hole principle most people think for at least a few minutes a day about any one question, and might find themselves asking any old sex advice columnist that question. So you are well camouflaged here on earth.

Plus, if you are worried you could always just change your handwriting a little bit like students do on end-of-semester evaluation forms, which totally doesn’t work.

As to your eventual question, I’ve got three rules. First, share when it will make your partner hornier. Second, keep it to yourself if it will make your partner angry or jealous or less horny. And third, change it ever so slightly to bring it from the second category to the first. Become an erotic story teller!

Good luck,

Aunt Pythia

——

Well, you’ve wasted yet another Saturday morning with Aunt Pythia! I hope you’re satisfied! If you could, please ask me a question. And don’t forget to make an amazing sign-off, they make me very very happy.

Click here for a form or just do it now:

Rebellious Lawyering Conference

In a bit more than a week I’ll be on a panel at Yale’s Rebellious Lawyering Conference 2015, otherwise known as RebLaw. If you’re wondering what that is, here’s a description:

RebLaw is the nation’s largest student-run public interest conference. Every year the conference brings together practitioners, law students, and community activists from around the country to discuss innovative, progressive approaches to law and social change. The conference, grounded in the spirit of Gerald Lopez‘s Rebellious Lawyering, seeks to build a community of law students, practitioners, and activists seeking to work in the service of social change movements and to challenge hierarchies of race, wealth, gender, and expertise within legal practice and education.

The panel I’m on is entitled Using Law To Occupy Wall Street, and I’ll be on the panel On Saturday the 21st at 10am with my friend Akshat Tewary, of Occupy the SEC, as well as Rebecca Wilkins, who I’m excited to meet. The panel is organized and moderated by Zorka Milin, who is both a kick-ass lawyer and a math nerd. The other panels look amazing as well.

Guest post: a survey of mathematical podcasts

This is a guest post by Samuel Hansen, a podcast producer and the director of the ACMEScience podcast network. He spends his spare time listening to podcasts that he did not produce, playing soccer, and hoping more people would pitch him podcast ideas. He isn’t kidding, if you have ideas for a podcast he wants to hear them.

My name is Samuel Hansen and I love podcasts. This might not seem like that crazy of a confession, but I would like you to keep in mind that I am currently subscribed to 97 shows and am caught up on all but 10.

I started listening to them around the time I started my undergraduate studies, so 2005 or so. It might seem odd, but a huge amount of the good things that have happened to me in the past 10 years are because of podcasts. Most of my closest friends I have met because we are all fans of a certain podcasting network, the best working collaboration I have ever had came out of an interview that I did, and I have had the opportunity to travel around the world producing a show.

My journey down the mathematical podcast rabbit hole started when I started to apply to graduate schools. Being a huge fan of podcasts I went looking for a podcast that would help me better understand the world that I was about to enter into, the world of the mathematical graduate student. While there were a couple of shows, none of them were exactly what I was looking for so when I started graduate school I knew it would be up to me to make the show for the next person that went looking.

I will admit that first show was silly, very very silly, and quite vulgar, but I had to start somewhere. Since then I have produced shows featuring interviews with mathematicians, round ups of the week’s mathematical news, and multi-voice stories from the mathematical domain.

I am not the only mathematical podcaster though, there is a whole community of producers out there making great content for us to consume. I have collected all of the mathematical podcasts that I know of here. Not all of them are still running, and some formats will appeal to you more than others, but they are all wonderfully mathematical.

Regularly Released Podcasts

- One of my current favorites is Taking Maths Further from Peter Rowlett and Katie Steckles. Produced for the Further Maths Support Program the show takes a different field from mathematics every episode and features an interview with a mathematician working in that field.

- Wrong, But Useful is the brain child of Colin Beveridge and Dave Gale. New episodes come out around monthly and feature mathematical stories that they came across in the previous month with a bit of focus on the UK and UK mathematical education. Each episode also features a problem of the month.

- Conversational interviews with people who live mathematical lives, at least that is what I always envisioned Strongly Connected Components as being. The second podcast that I created, Strongly Connected Components is only recently relaunched and I am so happy to be producing new episodes and talking to yet more wonderful people from the world of mathematics.

- Math Mutation is a series of quick hit podcasts about the fun and interesting mathematics that is not usually talked about in school.

- Tim Harford, the Financial Time’s Undercover Economist, helms the BBC’s More Or Less , a radio show that does everything it can to examine and interpret numbers and statistics that appear in the news and everyday world. The podcast feed features both the full length Radio Four episodes as well as the shorter BBC World Service episodes which are produced even when the show is between series.

Irregularly Released Podcasts

- I am more proud of this podcast than anything else I have ever done. Relatively Prime is a podcast that features 8 episode series of stories from the mathematical domain. The first series had episodes about Chinook the AI that defeated checkers, my favorite mathematical building La Sagrada Familia, mathematicians favorite numbers, and first hand accounts of working with Paul Erdos. I am in the middle of producing the second Kickstarter funded series and believe me, it is going to be good. You can expect it late spring or early summer of this year.

- Inspired By Math is a podcast by Sol Lederman featuring long form interviews with mathematicians, educators, authors, and other people that are inspired by mathematics.

- Plus Magazine tries to bring the beauty and applications of mathematics to all who read it. Their podcast features interviews with mathematicians talking about their work and their lives.

- Both the AMS and the MAA have podcasts that feature interviews with mathematicians talking about their work.

- From the math blog The Aperiodical, The Aperiodcast features editors Peter Rowlett, Katie Speckles, and Christian Perfect discussing stories they had recently featured on the blog and was as aperiodical as its name would suggest.

- Math/Maths was a show that I co-hosted with Peter Rowlett where we discussed the past week’s news from the world of mathematics. It was very topical and could be odd to go back and listen to now, but there were some non-topical episodes mixed in. The show is sadly no more, but I have heard from a good source, myself, that the people behind it are working to bring it back in a slightly tweaked format.

The following mathematical shows are sadly no longer being produced. That should not stop you from going back and checking them out though, with the exception of my first show, Combinations and Permutations, which I give you free reign to skip.

- There were two podcasts about the history of mathematics and oddly enough both were produced in England. Bite Sized History of Mathematics was produced by Noel-Ann Bradshaw, Tony Mann, and Mark McCartney and was part of a project that was funded by HE Academy MSOR Network. It featured episode, and accompanying pdfs, about important theorems, important numbers, and important mathematicians. The other podcast, Brief History of Mathematics, was a BBC production presented by Marcus du Sautoy and focused on the biggest mathematicians from the past few centuries.

- If you like swearing, bad jokes, pop culture references, and a host that heavily relies on wikipedia during a show then Combinations and Permutations is the math podcast for you. This was the first podcast that I ever produced and featured my fellow graduate students at UNLV and I sitting around trying to be funny about mathematics while sneaking in some real content from time to time. I will readily admit it is not the best show, but it was tons of fun to do and from the feedback I did receive tons of fun to listen to if you are the right person.

- Tom Henderson and Nick Horton hosted the Math for Primates podcast for 14 episodes. It was an entertaining and irreverent look at topics in mathematics that relied heavily on the idiosyncratic viewpoints of the hosts. I looked forward to every episode and was very sad when they stopped coming, because(as the hosts themselves say on their website) talking about math is more fun that throwing poo.

- The Math Factor started in 2004 as a segment on Kyle Kellam’s Sunday Ozark’s at Large radio show on KUAF featuring mathematician Chaim Goodman-Strauss. Featuring a lot of puzzles and problems and other very Gardner-esque content the episodes were short, sweet, and well worth a listen.

- Peter Rowlett’s first podcast, Travels in a Mathematical World was a podcast of interviews with mathematicians talking about their work and episodes about math history and news. Done with the support of the Institute of Mathematics and its Applications the podcast really focuses on the cool jobs and interesting work in which mathematics allows people to take part.

There are also more general science shows that often talk about mathematics. What follows is by no means an exhaustive list, but it does feature some personal favorites of mine.

- I will clearly expose my biases on this one, Radiolab is my favorite thing. I am actually wearing a Radiolab t-shirt as I type this. I will readily tell anyone who will listen about my favorite episodes and it is Radiolab’s producer and genius, literally the MacArthur Foundation decreed him as such, that is the reason that I even thought making mathematics podcasts might be possible. The show is mostly about big ideas and science, but some episodes do feature very mathematical stories.

- Presented by Melvyn Bragg In Our Time is a long running discussion program from the BBC. Every episode features a topic and a panel of experts, usually academics, to discuss the topic. While not a math show a quick google search shows that they often cover the subject.

- The BBC also has an irreverent panel show presented by physicist Brian Cox and comedian Robin Ince called The Infinite Monkey Cage. They have had episodes about Randomness, Six Degrees of Separation, and Symmetry amongst many other sciency topics.

- Keith Devlin has been NPR’s Math Guy for many years and has contributed many different stories to the show Weekend Edition. Thankfully Keith has gathered all the episode for us.

- Science Friday has been a US public radio stand by for more than two decades. While primarily covering other scientific topics, they also feature mathematics at times.

- My podcast about fights from the history of science, Science Sparring Society, has featured stories about Newton Vs. Leibniz and Cantor Vs. Kronecker

Finally, I interviewed Mathbabe the other day and put it up on my podcast here:

Women and work and housekeeping

I’ve been enjoying Sheryl Sandberg’s columns with Adam Grant in the “Women at Work” columns of the New York Times. See for example this one on discrimination at work.

The most recent one, third in a series of four, talks about how women at work do lots of extra “housekeeping” tasks like training, giving advice, and so on, which is often unrewarded. In fact they point out a double standard in expectations for this stuff:

In a study led by the New York University psychologist Madeline Heilman, participants evaluated the performance of a male or female employee who did or did not stay late to help colleagues prepare for an important meeting. For staying late and helping, a man was rated 14 percent more favorably than a woman. When both declined, a woman was rated 12 percent lower than a man.

So, part of this is absolutely just sexism, which doesn’t surprise me. But I think another part of it is mismanagement.

Let me explain. First of all, this stuff generally resonates with me – I’m absolutely one of those people who tries to make the workplace “more of a community.” So, for example, things like figuring out stuff and building and updating a wiki, which then everyone can use as a resource and saves a bunch of time for everyone. That stuff is not directly rewarded even though it’s actually useful. Because of that weirdness, men (in general) don’t try and don’t care as much about it, so given a men-only group, it simply wouldn’t get done.

But here’s the thing, what should we conclude from such group behaviors like this? Should women stop doing those extra things, or should men start? Should we continue to ignore how much stuff like that actually helps, or should we begin to keep track? You might be able to guess what I think.

Sanderberg and Grant’s column is a rare example of a column which doesn’t fall into the standard trap of telling women to simply conform to the current system of rewards. They explain that this kind of “Having people help both behind the scenes and in public is essential to organizational success. Research shows that teams with greater helping behavior attain greater profits,sales, quality, effectiveness, revenue and customer satisfaction.” and then they go on to state the obvious:

But doing the heavy lifting can take a psychological toll.

The question is, why? Is it because people ignore your efforts? I think it is, at least partly, and the other part is the sexism.

Now, Sandberg and Grant did suggest that we begin to “track acts of helping,” but then they go on to focus on how women should care for themselves before others, and give a load of advice about how to be more efficient when being helpful.

I’m already really efficient, though, so I’d like more advice on that first part, keeping track of acts of helping, and in particular how to build an incentive system that both men and women respond to which rewards stuff that’s actually good for the company. Because obviously just keeping track of stuff won’t help if you don’t actually care about the numbers. Or, even worse, if you just pity the poor fool who helped the most.

So the question is, how do you do that? Getting rid of assholes is already hard, and this is more nuanced than that.

Why not bored and brilliant kids?

If you’re like me you’ve been listening on public radio for the last couple of weeks to a “New Tech City” challenge called Bored and Brilliant, focused on getting people to stop checking their phones for email, twitter, and games. The idea is that “your most creative moments happen when you’re bored,” so try to let yourself be bored. The challenge ended yesterday.

I liked the challenge, since I’ve been on record that I’d like to be bored for the last couple of decades (very unsuccessfully!). It’s a constant goal of mine, and I thought it was obvious that boredom creates moments of creativity.

That’s not to say I don’t get addicted to games on my phone – curse you Candy Crush! – but I do delete them with regularity. And I always cherish the couple of days when I’ve lost my phone but before I get my new one. Sweet freedom!

Anyhoo, two points. First, the challenge didn’t have an enormous effect on actual phone usage for the people who signed up for it (other data is here and looks similar):

That doesn’t surprise me, but even changing people’s mind about whether it’s good to be bored is a worthy secondary goal.

Which brings me to my second point, namely, why don’t we let our kids get bored if we think it’s so great? I mean, I deliberately keep my kids virtually unscheduled outside of their school and homework. To be fair I mean the older kids, who are 12 and 14. The 6-year-old still goes to after school most days, although he comes home with his 12-year-old brother on Thursdays to do absolutely nothing. But that doesn’t seem to be the general practice of most other parents nowadays, including, I’d bet, quite a few of the participants in the “Bored and Brilliant” project. What gives?

After all, kids aren’t addicted to phones (yet), and they don’t have as many family responsibilities, and they do have plenty of reasons and avenues to be incredibly creative. My best moments of childhood – playing music, forming lifelong friendships, reading Dostoyevsky, and yes, experimenting with things – only happened because I was utterly without other grown-up plans.

Where does all that settlement money go?

In the Alternative Banking meeting yesterday we kicked things off with a great visit from Katya Cohen, author of a new book called The American Spellbound, where she describes the fictional account of a women working in a large bank and learning to fit in with the mindset of greed combined with a superhero complex. Good stuff, and it explains at least a little bit to me about what the heck was going on in the one outrageous Robin Hood Foundation awards night dinner I went to at Cipriani way back when.

After that we talked for a bit about the recent S&P settlement with the Justice Department, which was one of those nobody-goes-to-jail deals that cost $1.5 billion.

Now, that’s a lot of money to you and me, but it’s not that much to huge financial institutions; in the case of S&P it’s about two years of profit, depending of course on which two years you’re talking about:

That’s not what we focused on yesterday, though, because it’s really old news. All these massive settlements are relatively manageable for the financial companies that end up paying them. In fact that is implicitly part of the deal, and it’s part of why the system is so contemptible. In the end, the settlements don’t substantially threaten business as usual. Instead, as Gerald mentioned, you should take the word literally: the settlements do nothing but “settle” things back to the way they were.

That brings us to the question we focused on yesterday: where does all this money go? It’s big money after all, and if it goes into state coffers, to be used as Cuomo or whomever sees fit, then the concern is that, as corrupt as this system is, there will be powerful forces at work to keep it just like this. If a given state (New York State, I’m looking at you) gets addicted to this cash flow, there will be no reason to change tactics and, instead of massive fines, simply jail wrong doers and break up or dissolve corrupt institutions.

In fact, if you think about it, there will even be reasons for places like New York State to allow wrongdoing in order to cash in for the settlement a few years later. The more you think about it, the more this “big fines but no jail time” settlement practice we now have in place seems like a way to legalize and tax crime.

Anyhoo, we might be getting ahead of ourselves (although, equally, we might be late to this game) and so we’d like to follow the money. Where does the settlement money go? Do the funds earmarked for “victims” actually go to victims? Is this information available beyond vague statements like “S&P parent McGraw Hill Financial Inc, said it will pay $687.5 million to the U.S. Department of Justice, and $687.5 million to 19 states and the District of Columbia, which had filed similar lawsuits over the ratings“? Can we build an infographic to see who might be compromised in terms of demanding and enacting a more functional white-collar crime system?

Aunt Pythia’s advice

Holy shit, guys, it’s already fucking February, and Aunt Pythia isn’t ready for Spring at all. Spring is when things get frighteningly beautiful and distracting and the cycle of nature breaks our hearts and blah blah blah and a certain something is due, and Aunt Pythia would rather it stay mid-January for a while yet, do you dig?

Speaking of being distracted (or not!), someone sent me this link (hat tip name withheld for privacy protection) that’s supposed to be “porn for women”:

All the pictures are like this.

The book’s description:

Prepare to enter a fantasy world. A world where clothes get folded just so, delicious dinners await, and flatulence is just not that funny. Give the fairer sex what they really want beautiful PG photos of hunky men cooking, listening, asking for directions, accompanied by steamy captions: “I love a clean house!” or “As long as I have two legs to walk on, you’ll never take out the trash.” Now this is porn that will leave women begging for more!

Talk about perverted! You’d have to be a real fetish freak to be turned on by stuff like that. Personally, and Aunt Pythia doesn’t know about you, but Aunt Pythia prefers the kind of book that involves penises and vaginas.

And, good news on that front: when scouring the web with the phrase “porn for women,” it turned up this book list entitled 10 Sexy Books That’ll Make You Forget ’50 Shades Of Grey’ (Warning: Don’t read bad erotica. It’s bad for your vagina.).

Let’s start there, shall we? And if we ever find ourselves really falling off the deep end we can try out the above smut with vacuum cleaners, but Aunt Pythia highly doubts it will ever come to that. Plus, let’s face it, flatulence is always funny.

Which reminds me, I’m supposed to be farting out some advice to you wonderful and patient people. Let’s start this immediately, with the understand that, at the end of the column, you might just be willing to:

ask Aunt Pythia a question at the bottom of the page!

By the way, if you don’t know what the hell Aunt Pythia is talking about, go here for past advice columns and here for an explanation of the name Pythia.

——

Dear Aunt Pythia,

I’m a guy and a grad student and I was talking to a fellow grad student, Z, about gender issues in academia. Specifically, I was arguing that gender plays a role in fellowship/scholarship selection and college admissions, and she claimed that no, an applicant’s sex does not have any detectable influence on such decisions. We started talking about affirmative action and before we had time to even discuss the implications of affirmative action, she had to go to class and I thought that was the end of it.

A week or two later, one of my friends, Y, lets me know that Z had told her and several people that I had made some sexist comments. I was shocked and decided to confront her about it the next day. I said, “I heard from a friend that you’ve been telling people I made sexist comments.” When I asked her whether she had told anyone I made sexist comments she said no. I then asked her what she thought about our talk about gender issues several weeks ago, and she said essentially that some people think gender plays a larger role in fellowship selection than it really does. I told her that I agreed with her, some people exaggerate who big a role it plays and that people who obtained these fellowships obviously deserved them, but that gender does play a minor role. I asked her a few more times whether she had said anything to anyone even as an offhand remark (and in the least aggressive way as I could), to which she replied no each time.

I have little doubt that she did tell people about our talk and report to them without context what I had said, but I don’t understand why she wouldn’t just admit it and talk more about it. Of course any statements, even factual ones, in support of the thesis: being female sometimes helps in getting scholarships and in college admissions, is terribly easy to twist into a sexist remark, and I think that’s probably what happened in this case. I don’t think intrinsically this is a sexist stance—it is a statement about the nature of the system, not one about the abilities of women. Am I crazy?

This whole experience has been extremely frustrating for me. Discussion about sensitive issues shouldn’t result in someone being labeled a sexist. How can we understand it if we can’t even talk without people getting defensive? Now I don’t know whether other people in the department who have heard the gossip and don’t know me think I’m a sexist. What should I do?

Gossiped About And Hurt Humongously

Dear GAAHH,

Life lesson learned! Or, otherwise put, you play with fire you gonna get burned.

Here’s the mistake you made. You talked to a person you didn’t really know, when you didn’t have enough time to have a proper conversation, about how “people like them” have it less tough than “people like you.” And even though it is not what you meant to say, that’s how it came across, and you’re going to have to live with that. Have you tried to imagine how that came across to her? Not great.

Also, it sounds like you decided to spend your time trying to prevent people from thinking you’re an asshole, but that will only make matters worse, because you haven’t acknowledged any mistake, real or perceived.

In other words, if you want to make things right with the woman you originally talked to, here’s what you don’t do: accuse her of telling lies about you, since that would make her defensive, and moreover, she wasn’t telling lies. She was telling people how she felt after your conversation. In her shoes I probably would have done the same thing, in fact, and if you came up to me afterwards and said, “hey, did you tell people I’m sexist?” I would deny it too, since after all it’s not my problem, it’s yours.

Here’s what you could do that may or may not work, depending on how deep the hole is that you dug already: write a letter to her showing you know how much sexism is in the field of mathematics, with reference to various double blind experiments that show how people assume women don’t understand stuff, how they write weaker letters of recommendation, and so on, and conclude with an acknowledgement that the system has to make up for that in order to be fair. And that, moreover, the result of that system is still probably not sufficient, given how few women there are, but that in any case the women that are in the grad program, on average, are clearly just as strong, and quite possibly stronger, than the men. Finish the letter by apologizing if it came out wrong the first time but now you’ve learned you lesson.

Good luck!

Aunt Pythia

p.s. I’d be happy to publish your apology letter once it’s complete. That way other confused men (and women!) can use it too.

p.p.s. I notice you signed off “gossiped about and hurt humongously.” Hopefully you can understand that you were likely gossiped about because you hurt someone else humongously, and that this is just as much about them than about you. Which is not to say you haven’t been hurt, but if we spend all our time licking our own wounds rather than understanding what went wrong, then no progress will be made. I do actually think this turn out well, but it will require you to think about what you did, and to make amends for that first, before trying to address yourself.

——

Dear Aunt Pythia,

I take my six-year old daughter to school on subway every day. Recently, ads appeared on our line, which sometimes happen to be right in front of us, for the Museum of Sex, or “MoSex” (incidentally, located around the corner from MoMath). They include the quote “Like a Willy Wonka sex dream!”

My daughter hasn’t asked anything yet, and probably hasn’t paid any attention. I still think it’s inappropriate. Sex may be great fun and entertainment to some, but shouldn’t be advertised as such to children. Am I a prude?

Anyway, I was bothered enough to write a complaint on the MTA website. I got a response:

“As you may know, the MTA’s Board had enacted an advertising guideline that prohibited ads that are demeaning to people on account of their race, sex, religion or national origin, but that guideline was recently struck down by a federal court as inconsistent with the First Amendment. As a result, the MTA is prohibited from applying that standard to restrict ads and must post the ad in question. As we have sought to make clear by requiring prominent disclaimers, the MTA does not endorse or support this or any other paid advertisement that appears in the MTA system. The MTA displays advertisements in the system to generate much-needed revenue to support the MTA’s vital transportation function.”

The response makes me angrier.

Is there anything else I can do? Or should do? Or should I relax and be grateful there is no outright pornography in the subway? Or should I be sad about it? It could also generate much-needed revenue…

Not a fan of MoSex

Dear Not a fan,

It’s New York. And your kid hasn’t actually complained. Personally I find the constant barrage of sexualized advertisements with perfect plastic people more demeaning than straight up sex museum advertising, but I don’t know who to complain to about that.

Luckily, you do have lots of power in this situation, since it’s your kid. Namely, you can talk to her about how ads manipulate people and make her aware of stuff before they reach puberty but after she start actually reading the ads.

Those are some of the best parent-to-kid conversations I’ve ever had, and they basically sparked an ongoing game, whereby my two teenagers compete to explain what the “underlying message” of any advertisement or TV show is (but my 6-year-old doesn’t understand what we’re talking about and that’s fine). It’s fun! It’s life!

Good luck,

Aunt Pythia

——

Dear Aunt Pythia,

I am a man, not exactly young (I have grand-daughters in high school and college now, and I retired one year ago). My quandary is the following: I have been diagnosed with prostatic cancer and the prognosis if I don’t have surgery is bleak: between one and two years. But the prognosis if I have surgery is bleak as well: even if the hospital I go to has very good reputation, the risk of relapse combined to the pain of post-op, the damage to urinary and most importantly for me to sexual function would probably make me miserable for say five or ten years I would possibly gain with this procedure. I feel very much like choosing to spend the next two years having all the great sex we want with my lovely wife, put my scientific papers in order and damn the cancer anyway.

What is your opinion?

Shadow Or/And Prey

Dear SOAP,

It’s your life! And if you have the option to have more sex with your hot wife, I say go for it. People overemphasize length of life over quality of life.

Aunt P

——

Hi Aunt Pythia,

I have a higher libido then my boyfriend, who I love very much. How can I satisfy both our needs? I find it would be awkward to “help” myself if he is there, we live together. I think I would be up for doing it everyday, for about 2/3 of the month, he, far less so… On a related note, is there good erotica you would recommend?

On a completely unrelated note, what was your advisor student relationship dynamic like back in your math phd years? I have had both a young advisor and a relatively old one (current) and find that the two operate very differently. With the younger one, we talked a lot, whereas with my current one, I am left with a question and it’s harder to talk to him about intuitions for the problem…etc. We also meet weekly, but I feel like it is harder to speak about a problem with him. How can I improve this to a working relationship that is more similar to the one I had before (in case you are wondering why the previous one is over, it was for an undergraduate research project).

Love,

NYMPHO

Dear NYMPHO,

Masturbate! Masturbate until you’re raw, if that works! If your fingers get tired, consider getting an electric vibrator, they are easily available.

And if you find masturbating awkward, keep in mind that the alternatives are often way more so. And hopefully the above-mentioned erotica will help. Please send me reviews of each and every book on that motherfucking list.

As for the advisee situation, experiment on more structure in your meetings with him, until you find a format that leads to better and more fluent conversations. For example, tell him to come each week prepared with three specific questions. And think about it from his perspective, he’s so lost he probably doesn’t even know how to describe how lost he is, and giving him a task to complete, even if it’s just “write a list of three questions for me,” might help him a lot.

UPDATE: some eagle-eyed readers noticed I likely misinterpreted your question. I thought you were the advisor, not the student. Now that I’ve been set straight, though, I wouldn’t change my advise too much. Set yourself the goal of asking three specific questions, and see how that goes. Tell your advisor you’d like to improve the fluency of your conversations and you’re trying different things towards that end. Tell your advisor it’s important to you to have an easy conversational relationship with them.

Good luck!

Aunt Pythia

——

Well, you’ve wasted yet another Saturday morning with Aunt Pythia! I hope you’re satisfied! If you could, please ask me a question. And don’t forget to make an amazing sign-off, they make me very very happy.

Click here for a form or just do it now:

I Love you Mathbabe, but 529 Plans are Awesome.

This is a guest post by FogOfWar, who disagrees with me about 529 plans and my plan to make paying for college harder.

I’m catching up on the 529 kerfuffle. First observation: this made a massively outsized splash in public perception compared to what one would expect from a technical tax provision, which (more on this later) has a budgetary impact within a 5% confidence interval of $0.

Second observation: my good friend Cathy, who has kids mind you, is arguing against the 529 plan. Huh? When did we enter the Twilight Zone? Beating up on 529 plans is like stealing oatmeal from orphans—they’re too small to defend themselves, you don’t really get much if you win and everyone loves the soot- smudged little munchkins.

So here is what may be patient zero: this GAO Report released in 2012. The headlines read right into the talking points people are quoting. If you’re going to read it, try an interesting thought experiment: mentally substitute “401(k)” for “529” and “saving for retirement” for “saving for college” everywhere you see it. That’s not a completely fair analogy, but neither is it completely unfair…

Also, right at the beginning of the report, there’s an interesting omission. It’s in the “who did we talk with to figure out what was going on here?” section. Not that the report did a bad job, but why didn’t they talk to the AICPA (the national organization of CPAs)? These are the people who are most commonly on the ground talking to clients (rich and poor alike) about whether a 529 plan makes sense for them. I think you’d get a slightly different focus in the report with this on the ground perspective.

529 Plans Work Really Well for Everyone but the Very Rich and the Actually Poor

You can define ‘rich and poor’ in a hundred different ways, so let’s pick 4 examples in a semi-arbitrary manner. All couples are two parents and 1 kid who is 3, and all live in NYC. Couple 1 (“poor”) earned $20,000 last year; Couple 2 (“middle class”) earned $75,000 last year; Couple 3 (“mass affluent”, or “the bottom 1% of the top 1%”) earned $250,000 last year and Couple 4 (“rich”) earned $3-5m last year. Each couple has $100.00 of extra funds and is deciding what to do with it.

Important note: that’s not “$100x” as code for $100,000.00, that’s really $100.00.

Everything we’re talking about here is downwardly scalable and transaction costs are minimal (the cost of a stamp or time to set up direct deposit/withdrawal). All the couples have student loans, which are charging them 5%. Assume a stable long term low-risk portfolio also returns 5% (this is a side debate, but for those wanting to make it higher, I’d say you should consider your returns on a risk-adjusted basis).

Each couple has 3 rough choices, A: contribute the $100.00 to a 529 for kids, B: invest the $100.00 outside the 529 plan for kids, C: pay down $100.00 of student loans.

Poor Couple: Well, these guys get no state tax advantage from making the initial 529 contribution, and given their tax rate, the compounding on the 529 earnings has a negligible tax impact. Plus they’re giving up liquidity, which has more value in their hands than it does in the higher income cohort. Not only that, but I believe (chime in if you know this for sure) that moving the $100.00 from parent’s account to 529 account moves the asset from “parent asset” to “child’s asset” on many (but not all) needs-based financial aid forms. In short, the 529 plan is a terrible idea for this couple.

The real question is whether they should pay down the student loans or invest the $100.00 outside. That question is more subtle, but the availability of the student-loan interest deduction (lower after-tax return on debt paydown) and liquidity considerations makes $100.00 outside investment the likely best option.

Basically the tax code (this portion) combined with student aid gives no incentive for this couple to save and maybe a disincentive (or maybe an incentive to buy physical silver and not declare it on fin aid forms).

Middle Class Couple: At $75,000 the couple is still getting the tax shield for their student loans. So, at a combined Federal/State rate approaching 25% (NYC is a very high-tax place to live), their ROI (Return On Investment) from paying down student loan debt will be only 3.75%, compounding. So cash in pocket of $3.75 in year 1, $3.89 in year 2, etc. Their return on outside investment is sorta the same, with a big caveat. It’s all in the taxes. If middle class couple is invested in mutual funds or bonds, then yes, it’s $3.75 in year 1, $3.89 in year 2, etc. If Middle Class Couple is tax smart, they’ll invest only in low-dividend/high-growth stocks that will compound over the next 15 years before being cashed out to pay for kid’s college. In this case, the taxes are much, much lower—not zero, but much closer.

Doing some quick math: if the $5 in appreciation is going to be taxed at 20% capital gains 15 years from today, that makes the current tax cost = ($5.00*20%)/(1+0.05)^15 or $0.48. So year 1 the stock investment gains $4.52 compared to $3.75 from paying down student loans.

That’s not the full analysis, however, as (i) that difference compounds over the next 15 years, and (ii) the compounding is on $5.00, not $3.75, so it’s even more powerful. Run a quick spreadsheet and the student loan deduction compounds to $173.70 over 15 years and the stock investment runs to $186.31 after cash-out capial gains. Note that I’m assuming that student debt “savings” are reinvested in additional paydowns of student debt (somewhat for simplicity).

There’s a more subtle point as well: income is dynamic, not static, and thus tax brackets and availability of tax benefits is not locked in. If their income increases over time (as is very likely to happen statistically), they may knock themselves out of the deductibility of the student loan interest, which would cut back to paying down debt. OTOH, liquidity concerns (which are hard to reduce to a single dollar value but are extremely important) push towards the stock investment. Complicated analysis and everything above should be the starting point not the ending point if you’re looking at this choice in real life.

Now let’s add 529 Plans to the mix. Because the couple is NYC resident, they get an immediate tax advantage of $10 cash-in pocket state tax advantage (this assumes no itemizing, which is just over the cusp of reasonable given the numbers). The compounding is 100% tax free, either now or on distribution, so right away the earnings are $5.00 in year 1, compared to $4.52 and $3.75 for the other two options.

But that’s not all: the $10 in pocket is also invested—let’s assume in 5% stock investments, as above, so there’s an additional $0.45 return on that, making the 529 earnings in year one a Patriots four-time superbowl championship winner at $5.45. Not only that, but the benefit compounds over time, so the 15-year return is $226.52, all in. 30% higher than paying off student debt on an after-tax basis.

Liquidity is still a concern, although 529 plans have more liquidity than paying off student debt (b/c of ‘wrong way risk’ but that’s another discussion)—you can at least get at the money, but you have to pay a 10% penalty. Also, all of these numbers get much more dramatic if you assume investment in the stock market at a 10% rate of return over time, rather than the more conservative 5% rate of return I’ve worked with. Also, if you factor in dynamic tax rates the 529 becomes even more attractive, as the tax cut from investment income gets higher in the out years.

Takeaway? The 529 plan is an extremely powerful tool for the true working class.

Second Takeaway: running some quick numbers, about 46% of the benefit over the ‘buy and hold stocks’ strategy here is from the state tax advantage and 70% is from the federal compounding and exemption on distribution of profits. If this couple has the misfortune to move to a state that doesn’t seem to care about the middle class saving for college, like, let’s say…Massachusetts or California (neither of which give a state tax advantage for 529 contributions), the 15 year return drops down from $226.52 to $207.89. Still not bad, but the state incentives are a huge part of the practical analysis. Note also, that anyone living in a state without an income tax (Texas, Florida) gets no state income tax advantage because there ain’t any state income tax to take the deduction against!

Mass Affluent Couple: Whew, that was a lot of ink on the middle class couple, and if you’re in the Mass Affluent income cohort and reading this for practical advice, go back and read the numerical analysis of the middle class closely, because with a few modifications it’s going to apply to you as well.

Before that, though, let me say that there’s been a lot of progressive spite (not sure what adjective to use here) thrown at this couple. Cries of “they really don’t need any help—we should take this away” are there either explicitly or just below the surface. Some of my best friends are mass affluent couples in NYC, and I will tell you that the cost of college is something that gives them grey hairs. It’s enough money to be able to pay for college, yes, but not as easily as it might look from the outside.

Plus, and maybe most importantly, earnings now are not a guarantee of earnings for the next 15 years. You’re free to say “cry me a river”, but these are people, and all they want is the best for their children and to villainise them for such doesn’t sit well with me. Also, as we said before, the state tax benefit is close to ½ of the total 529 benefit, and that benefit is capped out in NY at $5,000 per parent per year, so this isn’t reducing anyone’s state tax bill to $0.

OK, here are the numbers: paying off student debt is actually more attractive for this couple because they earn too much money to get the income tax deduction, which, by the way, now stands at 43% combined state & federal (I’m assuming, not unreasonably, that this couple are AMT taxpayers). So $100.00 paying down student debt compounds at the full $5.00 ending up at a full $207.89 at the end of year 15. Not too bad, and liquidity is sacrificed, which is still important, but probably less important for this couple than the others.

Investing on the side, even if done in a tax efficient manner yields only $186.31 after 15 years (I upped the capital gains rate to 25% to reflect higher taxes—this gets a little more messy in real life but it’s a decent approximation). Hmmm…

Takeaway: Mass Affluent couple is better off paying away their student debts than investing in the stock market, given our mathematical assumptions (and, critically, on a risk-adjusted basis).

What about 529 plans? Well, the 529 plan still yields $226.52. Definitely better than paying off student debt (and that investment opportunity doesn’t even exist after all debt is paid off).

Interestingly 100% of the benefit in that comparison is now state level. Let me say that again: for well off taxpayers who still have student loans, the federal tax advantage is in some ways $0 and the advantage is all at the state level.

Interesting observation, given that many of the cries were for Obama to remove this great federal incentive in 529 plans (neither Obama nor the US Congress has any input on what states decide to do with 529 tax treatment).

Takeaway: The well-off/upper middle class/mass affluent/merely wealthy/whatever you want to label them get some advantage from 529 plans, but mostly from the state level & that really has nothing to do with Obama one way or another.

The Rich Couple: Nothing we’ve talked about matters at all. For reasons I won’t get into, anyone earning this level of income who is contributing to 529 plans should chew out their tax planner and/or financial advisor. There are a few situations where they make sense, but usually 529s are an unbelievably sub-optimal use of your annual gift tax exclusion.

Takeaway: 529 plans aren’t relevant to the rich at all. They’re glad you’re spending your time thinking about 529 taxation rather than something that matters, like carried interest or the step up in basis at death…

OK, that’s great, but what about Cathy’s point?

Oh, right. Well, yes—when you subsidize an asset the price generally increases to at least some degree (there’s all sorts of complicated analysis on relative elasticity here), and in theory that impact of the 529 is hosing the poor at the expense of the middle class and upper middle class (and the rich, sortof/maybe). Still, I feel like there are a lot of much bigger moving pieces in the overall calculus of costs of college that 529 plan tax advantages aren’t really the primary driver moving the needle.

So, for example, the total budgetary impact from 529 plans & prepaid plans is scored at around $1bn/year (page 39 here). If you’ve never worked with OMB numbers that sounds like a lot, but there’s a special phrase for a number like $1bn/year in the beltway: it’s called “a rounding error”. This is less than peanuts in the overall scope of the budget.

Which leads me full circle to an interesting question: what’s really going on here? I mean, the Obama administration is, depending upon the color of your pin, either Reed Richards or Lex Luthor—you may hear that he’s evil or a Marxist, but not usually that he’s a moron. Yet, this was an unbelievably dumb thing to propose, and honestly, it was entirely predictable that it would be not only a hideous failure, but a very public hideous failure. Again, any on-the-ground CPA could have told anyone in the administration willing to listen that these plans are one of the only reeds the government gives to parents grasping at straws to find the money to cover college and pulling it away would be…well, like stealing porridge from an orphan.

Unless there really is a brilliant “I’m thinking 3 moves ahead of you” long-game/long-con (again, depending on the color of your pin) strategy. If so, could it be this:

The left wants to win the next election. Statisticians working hard have studied the impact of the Tea Party on electoral results for the right and have determined that the optimal game-theory path is to alienate and marginalize the Elizabeth Warren/Bernie Sanders progressive wing. To do so, Obama created a straw man (the proposal to cut back 529 Plans) that pretty much most of America would hate but die-hard progressives would love. This lays the foundation for important discussions of party planks between centrists and progressives, for the centrists to say “look at what your wingnut policies cost us on that 529 debacle”, thus isolating progressives from the central discussion in formulating policy and, you know, trying to make radical change or something crazy like that…

Paranoid? Or not paranoid enough….

FoW

Cathy’s short response: nobody except the affluent middle class (and the rich) has $100 extra to begin with.

S&P and the Puffery Defense

Yesterday the ratings agency S&P settled a lawsuit with the Department of Justice for awarding ridiculously high ratings for mortgage-backed securities way back when. For their massive contribution to the world-wide financial crisis, they got fined $1.5 billion, nobody went to jail, and they didn’t even have to admit what they’d done is wrong.

But here’s something they did admit: their use of the word “objective” when describing their models was mere “marketing puffery,” not to be taken seriously. This is called the “puffery defense” by Bloomberg.

To be fair, this wasn’t just about the usage of the word objective. From Bloomberg’s piece:

S&P said in its request to dismiss the case that the government can’t base its fraud claims on S&P’s assertions that its ratings were independent, objective and free of conflicts of interest because U.S. courts have found that such vague and generalized statements are the kind of “puffery” that a reasonable investor wouldn’t rely on.

Now, as some of you know, I’m writing a book about destructive mathematical models. And pretty much all of the models make claims of being objective. It’s part of the marketing for those models, a requirement to lure people into using complex, mathematical black boxes instead of their own brains, and crucially, in place of their own sense of fairness and accountability.

Example: Value-added models for teachers are showered with claims of objectivity (see page 4 of this marketing brochure for example), even though those claims are questionable at best.

So, it makes me wonder, is the Puffery Defense going to be widespread? Is it a technical and legalistic approach? Are we going to have a redefinition of that word so that companies are officially allowed to claim objectivity while actually meaning nothing like objectivity?

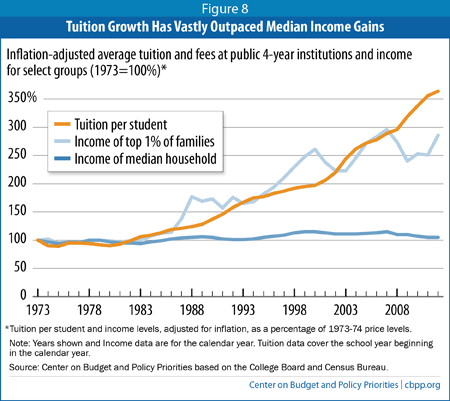

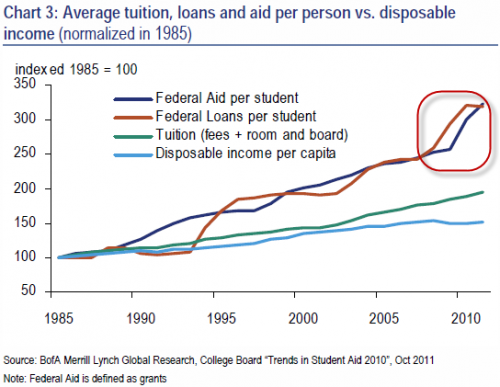

Let’s make paying for college harder

I was disappointed with Obama’s retraction of the tax benefit for college savings, referred to as the “529 plan.”

And, although some would claim that the 529 tax shelter was used by more than rich or very well-off people, it’s still a very lopsided regressive tax, because the majority of Americans can barely scrape by on their income, never mind saving for their kids’ college funds. But that’s not exactly the point I’m trying to make, although it’s a very important point.

The larger point is this: whenever we make college more affordable by helping people pay for college, it just makes college more expensive. Tuition rises to meet our new-found ability to pay. And although I can’t prove causality for every tuition hike, the data kind of speaks for itself:

versus here’s the federal aid growth:

The result of our federal loan programs, which were started with good intentions, is that whereas before college was out of reach for lots of people, now it’s still out of reach, they go anyway, and then emerge loaded with debt. It’s not actually a huge improvement for the vast majority of the middle class, but it’s become a requirement to get a reasonable job so people are forced to go through it, kind of like a hazing ritual.

There’s another related reason why college tuition goes up, namely because we have stopped funding state schools, so their tuition is higher, and the other colleges also rise to meet them. But part of the reasoning behind that is because we have all these federal loans available, so why would we need to fund the state schools.

We need to put into place ways for tuition to go down. First, we make paying for college harder, and that includes for upper middle class folks. The reasoning is this: if you’re the only person having trouble paying for something, that’s bad. But if everyone has trouble paying for something, the price goes down.

Second, we make state schools much cheaper, or even free, by funding them.

Slate Money Talks Sports

Lots of traveling in the last couple of days, and not enough sleep, has prevented me from posting as often as I’d like. Aunt Pythia sends her regrets.

But if you’re interested, please take a few minutes to listen to this week’s Slate Money podcast, which I particularly enjoyed being part of, and meeting this week’s esteemed guest Mina Kimes of ESPN the Magazine. We talked about money issues around sports, namely whether college athletes should be paid, the economics of stadiums in cities, and the NFL Commissioner Roger Goodell.

If you’re interested, go here or look up “Slate Money podcast” on iTunes.

When Errorbars Hit Mainstream News

It’s interesting to me how science has come into conflict with the news in the past week. First we had the deflategate, where footballs mysteriously deflated during a playoff game, and then we had an over hyped blizzard.

The NFL recently hired physicists at Columbia to help make the case for science with the football fiasco, but I think that’s unnecessary: a few good experiments with temperature and friction and lots of measurements by lots of different pressure gauges will empirically demonstrate how much of a range we might expect from such things. In other words, understanding errorbars.

As for the blizzard, this article nicely articulates the science of weather forecasting and what went wrong. But what is interesting is that, in general, models have gotten much better, and in particular are good at predicting how powerful a storm is going to get. In this case the model got that right, but then the error came in figuring out exactly where the storm would travel and when.

Again, it’s a case of errorbars, and the public seems not to understand it. Or maybe they just don’t want to.

In fact, I heard quite a few people call in to ESPN radio over the past week trying to explain to the sports radio hosts what might be going on scientifically, only to be hung up on. The truth is, it’s not as interesting a story to think about it just happening outside our control. It messes with our sense of omnipotence and control.

This is bad news for society, as more and more things become “datafied” and as we assume that will translate into perfect information.

Dartmouth Math Colloquium & All Souls Panel on Mega-Foundations

This Thursday I’m heading up to the Dartmouth Math department to give a colloquium on the subject of data science. They made the following poster for my talk:

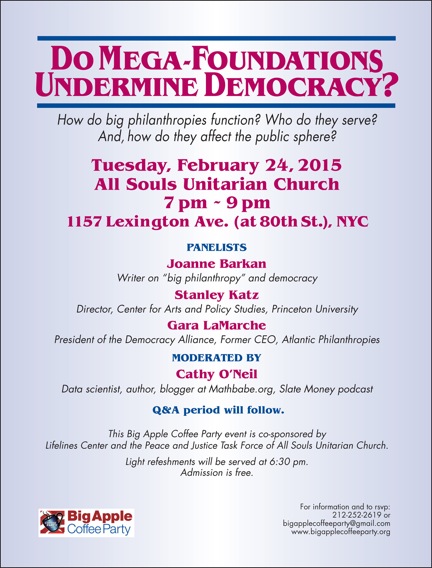

Also, next month I’m excited to be the moderator of a panel at the All Souls Unitarian Church on the east side of Manhattan, with some amazing panelists. There’s also a poster for that event:

I hope I see you there!

Grexit

The exciting news today (besides tonight’s blizzard!) is the Greek elections. Yesterday an anti-austeristy party called Syriza won the plurality of the votes, and is on the very verge of winning a majority as well.

This is huge because the leader of the party, Alexis Tsipras, has basically promised the Greek people that, if elected, he would refuse to pay off any more of Greece’s debt.

How did this happen? Well, From the perspective of the Greek people, the negotiations around their economic problems have been taken on by their last two governments since 2008 with a bunch of European technocrats behind closed doors and in an intensely undemocratic process. Well, this is when democracy fought back.

Possible ramifications: If Greece indeed defaults, and it might leave or get booted out of the Eurozone (this is called “Grexit”), which may or may not be a good thing for Greece long term, but in any case is very interesting. Short term, the black market in Greece is said to be highly developed, so the average person isn’t entirely dependent on functioning banks anyway.

Also, I’m sure Greece has been looking at Argentina recently to see how their (accidental) default has been going, namely not as bad as everyone predicted. The world will be watching Greece to see what happens and to see how smaller countries can and will deal with stifling debt in the future.

Aunt Pythia’s advice

Time passes quickly, my friends. It seems like only yesterday that Aunt Pythia was answering really long questions, and today her questions seem to be extra short. Last week it was cold outside – freezing! – but this week it is warm and snowy (but not for long!). Last week she was knitting a cowl, this week a colorful scarf. Crazy changes, in other words.

Indeed the only thing that hasn’t changed is an absolute willingness, on the part of Aunt Pythia, to offer up irrelevant and terrible advice to you earnest people. Many apologies, you definitely deserve better, but this is just something Aunt Pythia was born with, there’s nothing for it.

My suggestion for you is to just turn away and stop reading. I mean, how many obscene images must one be subjected to??

This is a liqueur filled sperm-shaped bottle. I know it really exists because I bought one at a liquor store in San Antonio a couple of weeks ago, no shit. No, I haven’t opened it yet.

Wait, you’re still here? Really? Well, in that case, come on in, enjoy the warmth, get under a hand-knitted blanket, and don’t forget to:

ask Aunt Pythia a question at the bottom of the page!

By the way, if you don’t know what the hell Aunt Pythia is talking about, go here for past advice columns and here for an explanation of the name Pythia.

——

Dear AP,

is it worth saving, or should we just burn it all down and start again?

Sick of Bull Systems

Dear Sick,

I’m going to assume you’re talking about the financial system. I’m tempted to say “burn it” but there would actually be severe short-term problems caused by there being no financial system. Moreover, it isn’t clear that a new one would be built better than the existing one. I know that sounds disappointingly unrevolutionary, but there it is.

If you are feeling desperate, may I suggest ignoring it and starting a new one. If I had time I would be more active in the public bank movement in this country, which seems like a better alternative to ours and can exist in parallel.

Aunt Pythia

——

Dear Aunt Pythia,

Have you seen the Celtic Oracle designs? I made a deck but would like additional divination material.

Oracular Designs

Dear Oracular,

Nice! And flattering to oracles such as myself! Can I make a wee request? More naked people, especially men? Thanks.

Aunt Pythia

——

Dear Aunt Pythia,

I would like to start watching Dr. Who but I’m intimidated by 50+ years of shows. How do you get started?

Dr. Who Ignoramus

Dear DWI,

Common problem, I sympathize. The truth is, it doesn’t matter much. Let me give you a cheat sheet which should be more than adequate:

- Dr. Who is always a man who talks fast and is incredible smug, although usually in a lovable way.

- He sometimes has a dog named K-9 with him. If he does, you’re watching an earlier show.